-

November 06, 2019

-

Emerging markets offer new opportunities as low- to negative interest rates spread across the developed world.

Last summer, a large German conglomerate made an unusual move when it issued €1.5 billion in two-year and five-year bonds. It wasn’t the bonds themselves that were so eye-catching, however. Rather, it was the rates of return offered (negative 0.315% for the two-year bonds and negative 0.207% for the five-year bonds). Roughly translated, the below-zero yields meant that investors who purchased the bonds were paying to lend money to the conglomerate.1

Offering negative-yielding bonds (at nominal interest rates; i.e., rates before inflation) would seem to defy financial logic. In fact, it is a historic rarity. But since 2015, the trend has been spreading, reaching Japan and various European nations.2 If the negative rates extend into other major global economies, investors may want to turn toward emerging markets in the pursuit of positive returns.

Why Are Countries So “Negative” About Their Rates?

In 2008, central banks around the globe slashed policy interest rates to lower levels to encourage growth in consumer spending and corporate investment.3 Lower policy interest rates typically result in a reduction of nominal interest rates.4 Low policy interest rates also help improve a trade balance with weaker currencies. Despite these measures, the results have come up short as we currently still have an underperforming global economy.

To stimulate their respective economies, several central banks are lowering their policy interest rates even further — in some instances to negative rates. By doing this, the central banks hope to encourage local banks to lend cash out instead of depositing it back in central banks. Additionally, central banks believe that lowering rates to negative levels will encourage corporations to invest in projects that will stimulate employment and demand instead of hoarding cash.

Central banks are unlikely to raise policy interest rates in the near future because of their policy objectives and macroeconomic trends. Those include:

- Existing large fiscal deficits – This leaves little room for fiscal stimulus and places more pressure on monetary policy.

- Rapidly aging global population – Older populations are more risk-adverse and thus demand more fixed-income instruments.

- Fear of a recession – This increases the likelihood of further rate cuts which, in turn, increases the demand for fixed-income instruments.

- Technological developments – This reduces expectations for inflation in the future.

For some advanced economies, long-term government bonds and some corporate debt are trading at negative yields. Germany’s entire yield curve is below zero, meaning that an investor buying a 30-year government bond who holds it until maturity stands to lose money on the investment.

On the other hand, there is an advantage in buying long-term bonds that remunerate negative rates if one expects rates to drop further.

Negative Rates on the Horizon for the United States?

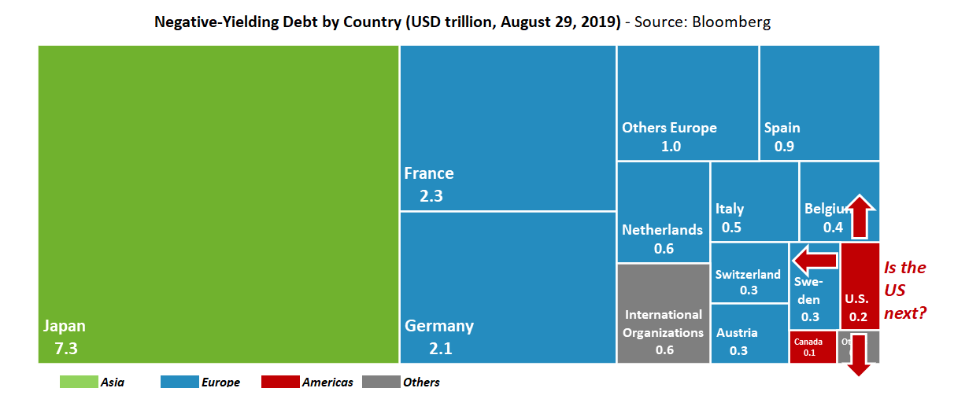

Globally, debt in excess of USD$17 trillion is currently traded at negative yields, and 30% of all investment-grade securities are traded with subzero yields to maturity, according to Bloomberg. Japanese and European economies account for 94% of the total negative yielding debt, as shown in the chart that follows.5

While the U.S. currently represents a fraction of global negative-yielding debt, this could change in the short term. According to Deutsche Bank, the hunt for positive returns has pushed European and Japanese investors toward debt issued by the U.S. Treasury and corporations, boosting the gains for holders of long-term bonds. Consequently, as U.S. Treasury yields have significantly declined, the U.S. dollar has appreciated against the average of all currencies.

What’s in It for Investors?

Investors seeking higher yields will continue to focus on the U.S. market. These investors are expected to explore emerging markets that have positive real interest rates and attractive economic prospects. An uptick in demand for emerging-markets bonds should reduce the overall cost of capital in these emerging economies and make investments in projects once considered unviable more attractive.

While the global impact from negative rates is still unclear, emerging markets are expected to see an inflow of investments from private equity, family offices and investors in general as the global hunt for yield intensifies.

Footnotes:

1: This is true for an investor buying these bonds and holding them to maturity, as interim investors can still make money if interest rates become more negative (which can happen if the yield curve is upward sloping).

2: Although Japan has had zero rates for almost 20 years, it was only recently that the rates went into negative territory.

3: The policy interest rate refers to the overnight interest rate that a central bank charges on deposits and loans from commercial banks. In the U.S., this rate is called federal funds rate. In Brazil, the rate is called SELIC rate.

4: A lowering of policy interest rates does not always result in an equivalent lowering of nominal interest rates because demand and supply factors also play an important role in setting of nominal interest rates observed in the market place.

5: https://www.bloomberg.com/graphics/negative-yield-bonds/ adapted by FTI.

© Copyright 2019. The views expressed herein are those of the authors and do not necessarily represent the views of FTI Consulting, Inc. or its other professionals.

About The Journal

The FTI Journal publication offers deep and engaging insights to contextualize the issues that matter, and explores topics that will impact the risks your business faces and its reputation.

Related Insights

Published

November 06, 2019

Key Contacts

Key Contacts

Senior Managing Director, Leader of FTI Consulting in Brazil

Senior Managing Director

Senior Managing Director