Key Trends in Fixed-Mobile Convergence (“FMC”)

-

May 07, 2026

-

Fixed-Mobile Convergence (“FMC”) — where U.S. households subscribe to the same provider for their home internet and wireless services – is increasingly a key competitive lever structurally shaping the U.S. telecommunications market. FMC is core to the strategy of several large players in the industry; in their full-year 2025 earnings calls, AT&T, Verizon, Comcast and Charter mentioned the word “convergence” 21, 10, 10, and 7 times respectively.1

To better understand this trend, FTI Consulting surveyed a representative sample of U.S. households at the end of 2025. We found that an increasing share of households are converged and, more importantly, that a significant share of home internet customers of convergence-enabled providers is considering convergence adoption. The opportunity is larger for the largest CableCos (Xfinity and Spectrum) that have relatively lower convergence rates, but it is also very sizeable for AT&T and Verizon, which already have comparatively higher convergence rates.

Key broadband providers differ in their approach to convergence. For T-Mobile, a convergence play is limited to its fixed wireless access (“FWA”) customers, among whom convergence adoption is already high, and its fiber footprint is significantly smaller in terms of homes passed than the large CableCos, AT&T and Verizon.2 T-Mobile’s convergence opportunity is therefore limited to its existing and future fiber footprint plus its growing FWA customer base, making its convergence opportunity smaller today than that of its mobile network operator (“MNO”) competitors (AT&T and Verizon) and CableCos.

AT&T and Verizon have a larger existing fiber base and are thus more technologically equipped to drive convergence adoption using technologies other than FWA. The cable providers also each have a large footprint of service across the country but require further go-to-market initiatives and investment to convince customers that they are a compelling mobile provider. Simultaneously, CableCos need to strategically deploy capital so that their cable technology remains competitive despite new fiber entrants competing in their existing footprint.

The United States telecommunications industry is unique. High-speed fixed infrastructure, cable and fiber, is highly fragmented so no one provider covers the entire country. This leads to elevated competition both between providers and technologies, as mobile network operators increase their reach into homes by acquiring fiber providers and using their existing 4G LTE and 5G reach to offer fixed wireless access (“FWA”) to an increasing number of consumers.

Cable providers, with the highest historic share of internet broadband subscribers, have been defending against this encroachment into their core market by offering converged bundles of their own, leveraging mobile virtual network operator (“MVNO”) agreements with mobile network operators to make up for their lack of owned wireless infrastructure. Not all providers are convergence-enabled, however, as most of the smaller fiber and cable companies lack a mobile offering.

To better understand how much and when to invest in marketing convergence, communications providers need a thorough understanding of consumer needs. Winning the convergence race requires leveraging network and consumer analytics to define successful go-to-market strategies and understanding purchasing behaviors that fit the competitive footprint. It also requires an awareness of when to use convergence as a new customer acquisition tool and how to expose a provider’s existing customer base to the cross-sell opportunities from converging.

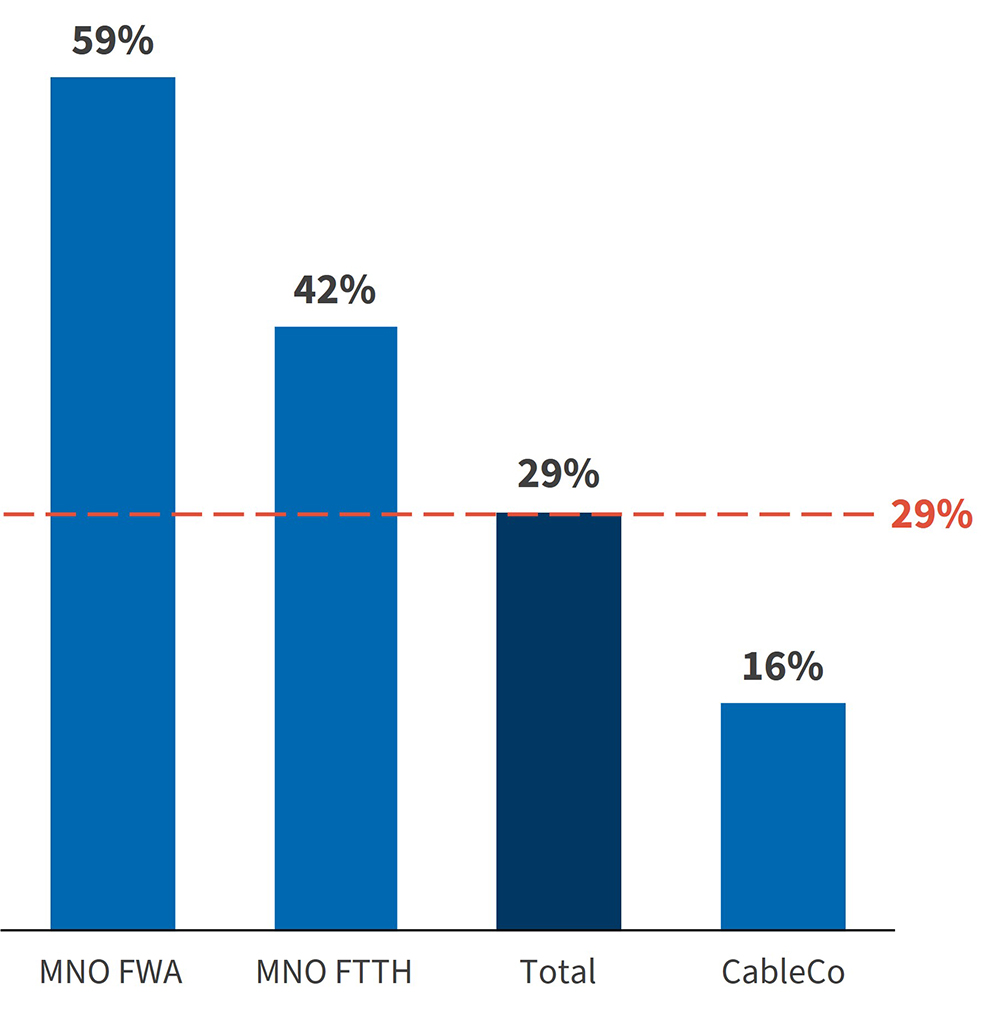

At the end of 2025, as shown in Figure 1, U.S. convergence rates as reported by individual players are 29%. FTI Consulting’s survey found that this convergence rate has increased by 15% year-on-year from 2024. We believe this pace will accelerate as more customers specifically seek out converged offerings and as convergence-enabled providers find ways to improve their cross-selling effectiveness.

Figure 1 – Convergence Rate by Service Provider

(% of home internet subscribers with same provider for mobile)

Source: Data from FTI Consulting Consumer survey and anchored against publicly available information from home internet providers

Recent success in driving convergence adoption has not been evenly distributed across three player segments:

MNO FWA providers (T-Mobile, AT&T and Verizon) have the highest convergence rates (59%) with wireless being their anchor service on top of which they add home internet through FWA technology.

MNO fiber to the home (“FTTH”) players (i.e., AT&T and Verizon) have the second highest convergence adoption. They mostly cross-sell FTTH broadband to their wireless customers as they expand their fiber passings.

Lastly, cable providers, with their MVNO-based mobile offerings, have been successful in driving convergence adoption by cross-selling wireless to their established broadband customer base. However, their convergence rates are the lowest among peers, sitting at 16%.

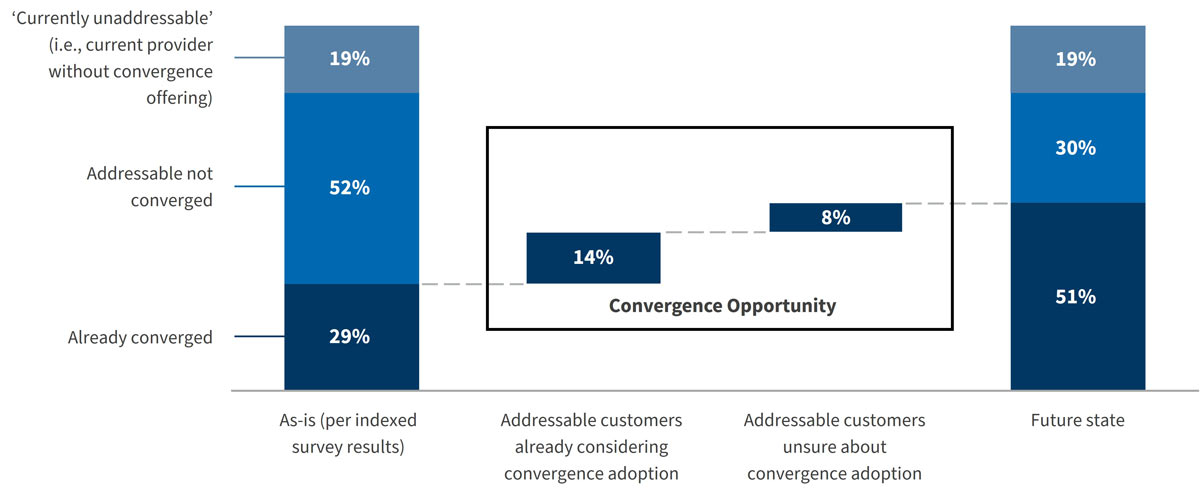

Providers of all types will need to develop clear strategies for accelerating convergence based on the markets where they can actively sell converged offerings according to their available infrastructure. This acceleration has no signs of slowing down: we estimate the convergence opportunity size to be 22 percentage points larger than the current converged customer share of 29%, with 14 percentage points of it addressable in the short-term, driven by the customers already considering convergence today.

Figure 2 – Convergence Adoption Opportunity Sizing

(% of home internet subscribers)

Source: Data from FTI Consulting Consumer survey and anchored against publicly available information from home internet providers

Beyond sizing the market opportunity, FTI Consulting’s survey revealed several novel and important observations about how and why consumers converge, and the implications of this trend to both convergence-enabled and non-convergence enabled providers. We’ve highlighted a selection of those findings below.

Key Findings

- Converged customers report higher net promoter scores (“NPS”) and satisfaction rates than their non-converged peers.

- The churn mitigation effect of convergence could be temporary as converged customers report a higher desire to change providers than customers who are not converged.

- Beyond price, non-converged consumers favor better network performance and incremental benefits as key convergence drivers.

- Convergence can act as a key lever for new customer acquisition.

- Consumers subscribing to higher broadband speeds report higher loyalty to home internet providers.

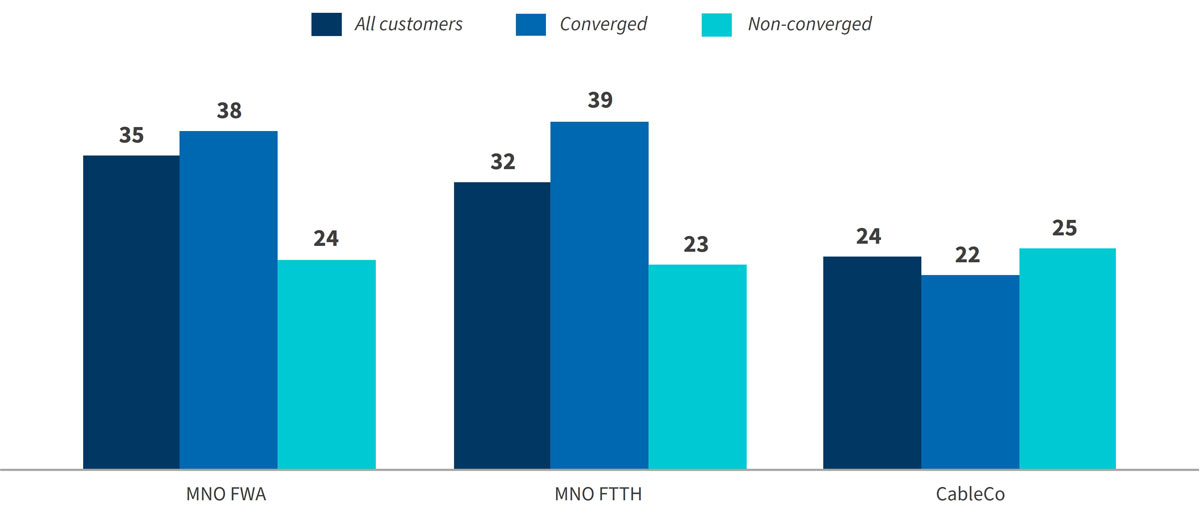

Converged Customers Report Higher Net Promoter Scores (“NPS”) and Satisfaction Rates Than Their Non-Converged Peers

Our findings indicate that converged customers are significantly more likely to be net promoters of their home internet service provider, with a ~19% relative increase in NPS over the non-converged baseline. This effect is true across providers and technologies, with the greatest effect for FWA providers.

A notable exception is cable providers, who report a relative decrease in NPS of ~12% over the non-converged baseline. These customers mostly adopted home internet first, which generally shows less satisfaction than mobile. This further decline due to convergence could be due to any number of reasons, but a few recurring responses in our survey include:

- Customer service and support – The increased complexity of converged offerings comes with incremental customer service challenges that convergence-enabled players must deal with effectively. Subscribers point to an inability to reach human support in many cases, a dissatisfaction with the customer service received when they do reach an agent and perceived slow responsiveness in resolution.

- Speed and performance of fixed broadband – Several customers report slower than expected download and upload speeds, or complain about buffering, throttling and peak-hour slowdowns; complaints particularly arise when customers perceive slower speeds than contracted.

- Service reliability and uptime – References to “spotty” connections and “cuts out a lot” are recurring issues with broadband. Specifically in fixed broadband, customers generally point to better storm and weather resilience and faster outage repair as potential areas for improvement.

These observations are common to several home internet providers but are worsened by convergence among users of cable providers and mitigated by convergence among users of home internet provided by mobile network operators.

Figure 3 – Home Internet Service Providers’ Net Promoter Scores (“NPS”)

Source: Data from FTI Consulting Consumer survey

The Churn Mitigation Effect of Convergence Could Be Temporary As Converged Customers Report a Higher Desire To Change Providers

Our market analysis suggests converged customers are less likely to switch broadband providers than non-converged customers across technologies. Our survey revealed an important nuance, however: converged customers are more, not less, likely to report a desire to switch than their non-converged peers. This is especially true for customers subscribed to broadband offerings by cable providers.

Remarkably, this desire to switch is concentrated on customers reporting that they want to switch both home and mobile broadband providers. We therefore find that converged customers, once introduced to thinking of their home internet and mobile subscriptions as a bundle, are more likely to stay converged in the future.

One potential effect of this higher desire is that the churn mitigation effect of convergence may be a mirage. Higher switching costs keep converged customers subscribed for longer, but their higher switching intent will catch up to those switching costs, and churn will rise for that category of consumers over time.

A possible explanation of this finding is CableCos’ low satisfaction — they are the only provider category to report a lower NPS for converged customers versus non-converged — make them distinct for churn mitigation purposes. The major mobile network operators of AT&T, Verizon and T-Mobile have negligibly increased switching intent among converged customers.

Figure 4 – Perceived Desire To Switch in Next 12 Months (% of Respondents)

Source: Data from FTI Consulting Consumer survey

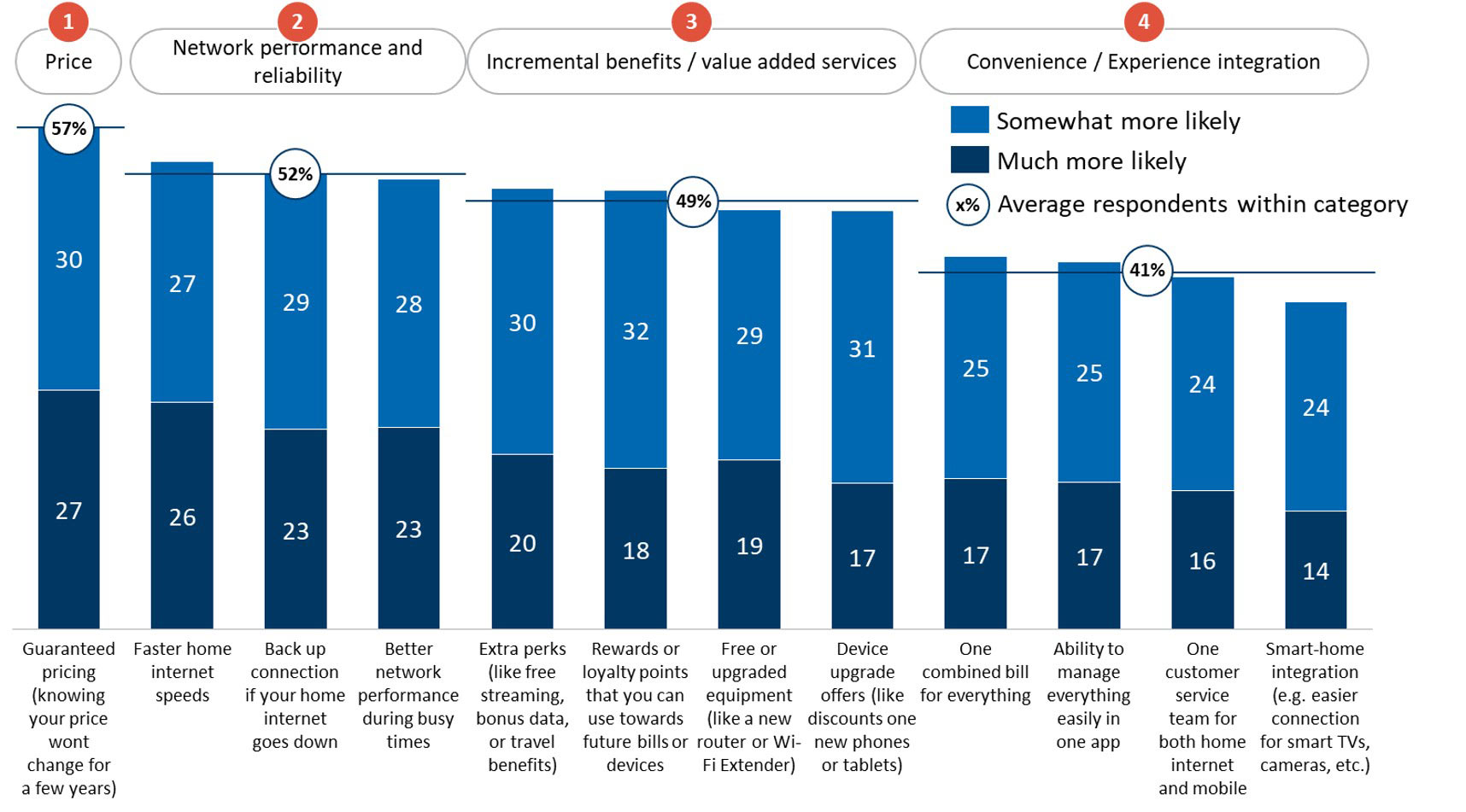

Beyond Price, Non-Converged Consumers Favor Better Network Performance and Incremental Benefits as Key Convergence Drivers

Non-converged consumers consider themselves more likely to converge if the switch brings with it either improved network performance and reliability or incremental benefits and value-added services. This differs from currently converged customers, who report being drawn in large part by convenience.

Based on the intent to switch drivers depicted in Figure 5, there are several go-to-market initiatives that U.S. providers could leverage to drive convergence based on these findings:

- Technology rollout and upgrades – As faster speeds become available through fiber-to-the-home and cable upgrades to DOCSIS 3.5 and DOCSIS 4.0, converged providers can use those better technologies to target the ~53% of customers for whom faster home internet speeds are either somewhat or much more likely to make them switch.

- Resiliency through FWA back-up – For subscribers on more expensive plans or as a potential up-sell, converged mobile network operators are uniquely positioned to offer functionally 100% uptime by using FWA back-ups when reliability issues arise. Converged providers could also investigate unlimited (or higher capacity) mobile hotspot data to serve as back-up during fixed broadband downtime.

- Consumer Premises Equipment (“CPE”) upgrades – Modern equipment with new technologies (e.g., WiFi 7, mesh routers) can be a relatively low-cost way of markedly improving perceived performance, further driving overall adoption and convergence benefits.

- Convenience improvements – If providers can modernize their billing and CRM systems, they may be able to drive significant adoption advantages. 42% of respondents indicated they would be more likely to switch if the new provider offered a unified bill or app, which would be a significant adoption driver with little marginal cost.

Figure 5 – Perceived Likeliness of Switching by Bundle Feature (% of Respondents)

Source: Data from FTI Consulting Consumer survey

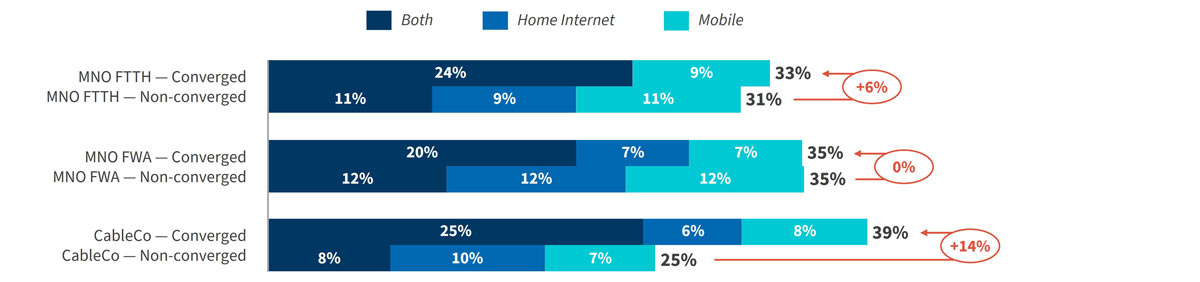

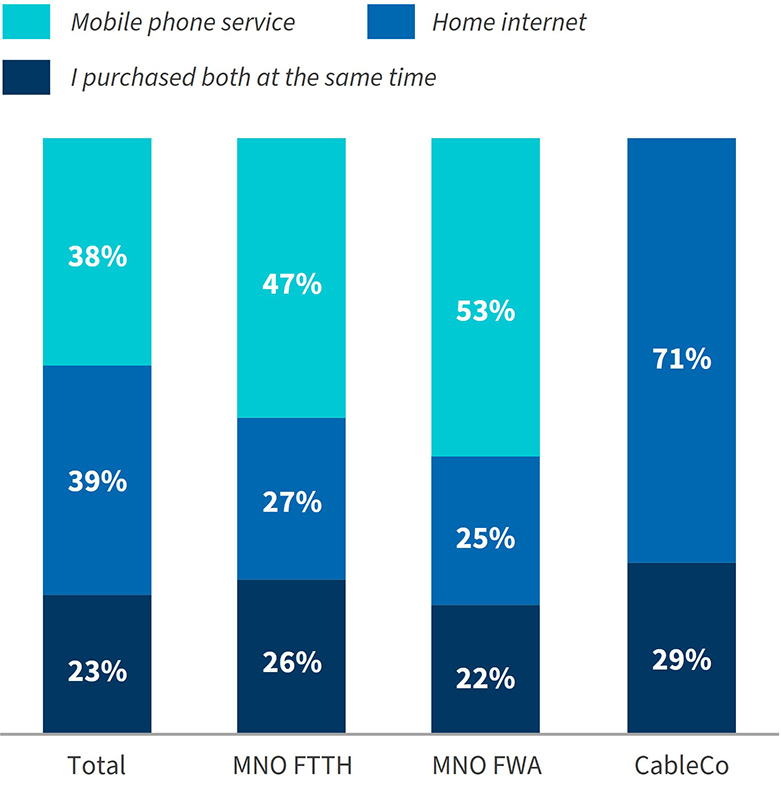

Convergence Can Act as a Key Lever for New Customer Acquisition

To date, most providers see convergence as a cross-selling opportunity rather than as a driver of new customer acquisition. Our survey indicates this view is myopic, as convergence provides a competitive advantage to acquire new customers.

Figure 6 – Anchor Services of Converged Subscribers

(% of respondents)

Source: Data from FTI Consulting Consumer survey

Our findings indicate that roughly a quarter of converged subscribers adopted both services simultaneously. That share is likely to rise over time as, once converged, customers tend to view home and mobile services together from a total cost of ownership and convenience perspective, and are thus more likely to stay converged in the future.

Some providers have been more attuned to this fact than others. The cable providers are particularly effective in advertising convergence benefits clearly in their acquisition flow for new customers, with Xfinity and Spectrum both offering one free unlimited line for one year to new home internet subscribers. This decision may be part of the reason that cable providers report a higher rate of simultaneous adoption than mobile network operators.

While mobile network operators drive a greater fixed-mobile convergence adoption rate overall, it is driven primarily by cross-selling. The sizeable opportunity for new customer acquisition through convergence benefits is thus underutilized by these providers. In their online sales flows, none of the three major US carriers show the benefits of convergence as part of their home internet package as clearly as Xfinity and Spectrum.

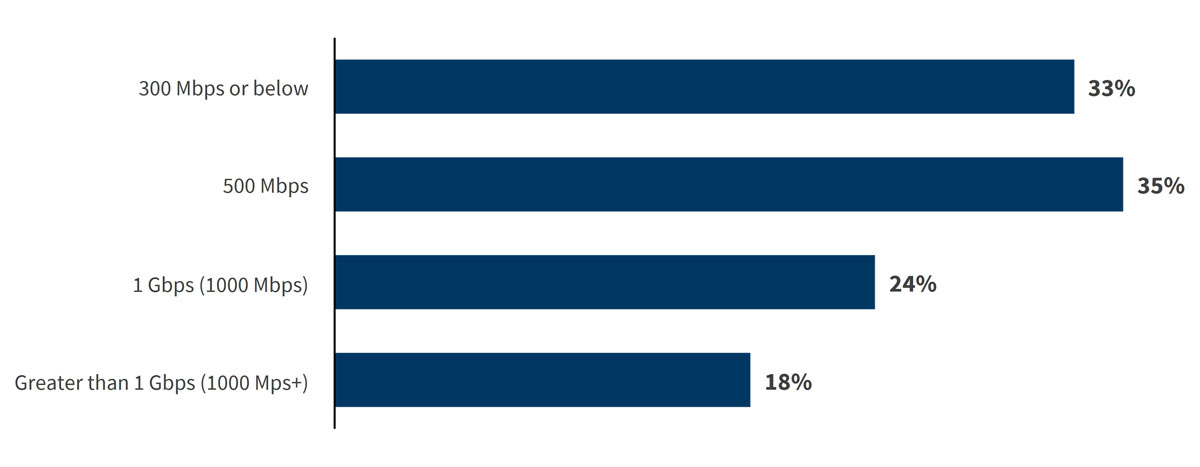

Consumers Subscribing to Higher Broadband Speeds Report Higher Loyalty to Home Internet Providers

Switching intent is concentrated among consumers of lower internet speeds, with roughly one-third of subscribers to speeds below 500 Mbps saying they want to switch. This contrasts with the roughly one-fifth of consumers subscribers to speed of 1 Gbps and up reporting the same.

The implication is that the benefits of up-selling consumers into higher home internet speeds are even more significant than previously thought. Intuitively, higher speeds bring a higher price tag and thus higher average revenue per user (“ARPU”). But benefits to providers extend beyond that: despite paying more, those same customers are more loyal to their home internet providers and face less desire to switch.

To capture those benefits, mobile network providers will need to invest significantly in further fiber rollout as FWA is not capable of 1 Gbps+ speeds. The cable providers, to match, can use a mix of technologies to make faster speeds and greater reliability available to their subscribers. This includes fiber-to-the-home (“FTTH”), and/or cable upgrades to DOCSIS 3.5 and 4.0. Lower churn makes the return on those investments potentially higher than previously thought.

Figure 7 – Desire To Switch Home Internet Provider by Speed

(% of respondents, excluding “Unsure”)

Source: Data from FTI Consulting Consumer survey

Conclusion

FTI Consulting surveyed a representative sample of the U.S. population and uncovered new insights about fixed-mobile convergence, its drivers, and its effects. As the number of converged consumers stands to increase significantly in the medium term (potentially by about 76%), providers of all types should investigate what the potential upsides and risks for their business are.

Implications for Mobile Network Operators: Expand Existing Converged Customers and Drive New Customer Acquisition

AT&T and Verizon are among the best-positioned players to take advantage of the increasing trend toward convergence. Their addressable market is far higher than their existing converged customer base, and expansion opportunities exist both through cross-selling their current customers and by leveraging the benefits of convergence as a driver of new customer acquisition.

The key limiting factor to driving these new customers is home broadband availability, both physical infrastructure (i.e., fiber-to-the-home) and wireless network capacity (i.e., FWA). A combination of organic and inorganic growth can address both bottlenecks, and an effective convergence-focused go-to-market strategy would allow them to convert new infrastructure into lower-attrition and higher share of wallet.

Implications for Cable Providers: Accelerate Wireless Adoption Among Customer Base, and Focus on Customer Experience

Cable providers, most notably Xfinity and Spectrum, have been aggressive in driving their customers toward convergence. Despite this, their converged customers have lower NPS and markedly higher switching intent than their non-converged peers, limiting cable companies’ ability to reap the rewards of their increased drive toward convergence. Careful examination of the customer experience and targeted improvements to their home and mobile offerings will be necessary to accelerate the pace of convergence and ensure that the benefits associated with it are captured.

Implications for Providers That Are Not Convergence-Enabled: Focus on Strategic Mitigation of Risks, Including Creating a New Converged Offering

Convergence is a key risk, but defensive measures can help providers protect against market share erosion. In particular, driving adoption of +1000 Mbps home internet speeds can help reduce the churn risk, especially against convergence-enabled cable competitors. Additionally,

it is possible for any provider to create a converged offering themselves, following the blueprint created by the cable providers and negotiating MVNO deals with MNOs. Unaddressed, the risks posed by competition with convergence-enabled providers are high. But a strategic approach to mitigating those risks can level the playing field and protect market share.

Footnotes:

1: T-Mobile was the only large player that did not mention fixed-mobile convergence.

2: Fixed Wireless Access providers use radio waves to offer internet services to customers.

Related Insights

Related Information

Published

May 07, 2026