IPO & SPAC Market Update: Q1 2026

IPO Markets Reopen Unevenly As SPAC Activity Surges and Global Momentum Slows

-

May 11, 2026

-

Executive Summary

IPO activity in the first quarter of 2026 reflects an uneven reopening of capital markets, with momentum concentrated in the United States and more limited progress globally. The IPO market is reopening, but in a way that favors speed, flexibility and select issuers rather than broad-based participation. U.S. issuance increased meaningfully compared with both the prior quarter and prior year, while global activity declined from elevated levels in the fourth quarter of 2025, highlighting a continued divergence in market conditions.

The increase in U.S. activity was primarily driven by higher deal volume rather than larger transactions, suggesting that issuers are returning but investor conviction remains limited. While more companies are entering the market, only a subset are achieving strong investor support. Additionally, the growing share of SPAC issuance indicates continued use of alternative structures for flexibility in accessing public markets.

While capital formation remains above prior-year levels globally, ongoing geopolitical uncertainty and uneven sector participation continue to limit a wide-ranging recovery. Investor demand is selective, and access to capital is not broad-based across issuers or sectors. For executives considering a public listing, current conditions present a potential but selective window in the U.S. market, which remains sensitive to market dynamics. Access to public markets is improving but remains inconsistent.

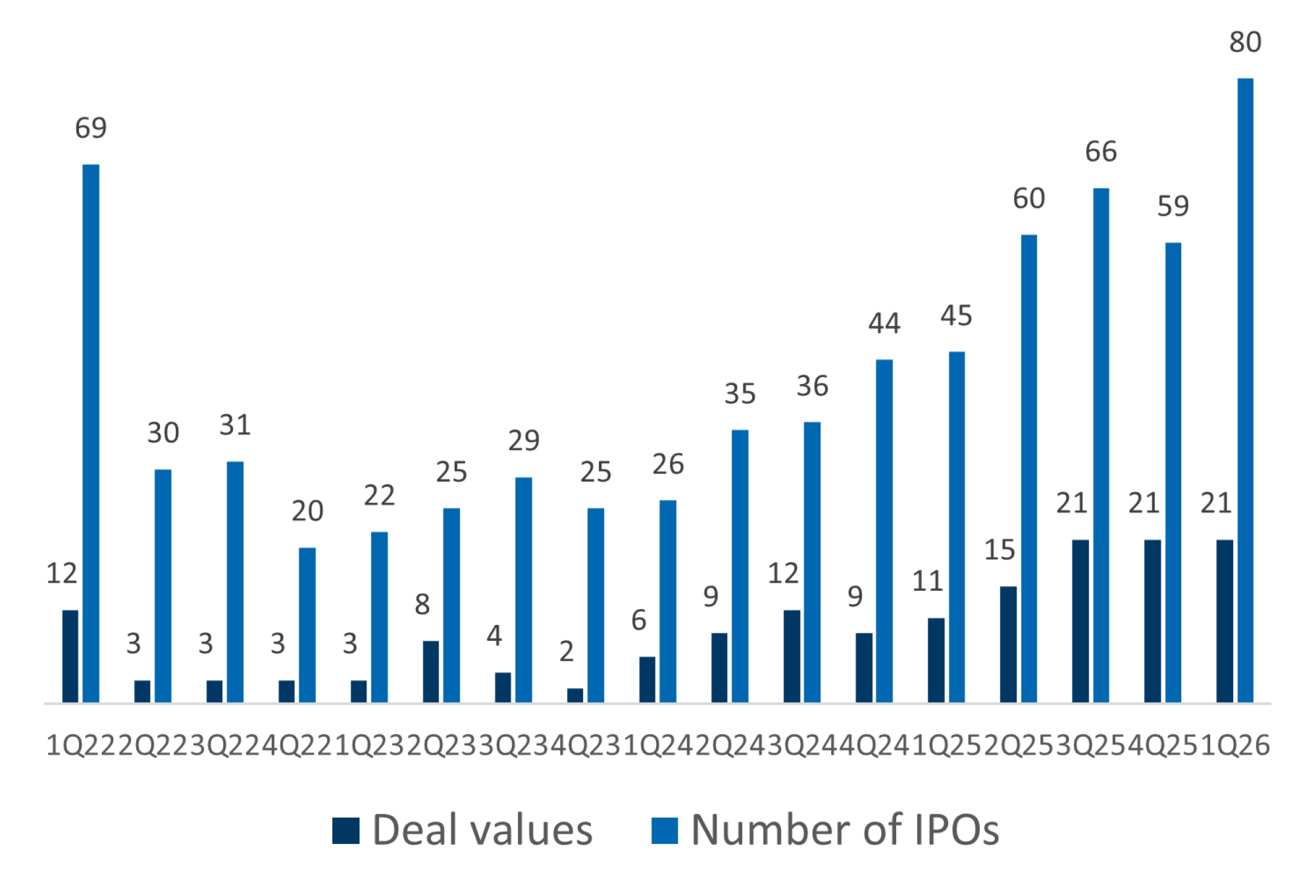

U.S. Market Overview

U.S. IPO activity increased in the first quarter of 2026, with deal count rising 36% quarter-over-quarter (“QoQ”) and 78% year-over-year (“YoY”). Transaction values remained flat compared with the fourth quarter of 2025 but increased 91% from the first quarter of 2025, reflecting a meaningful recovery in capital formation from prior-year levels.

The divergence between rising deal volume and stable transaction values indicates that activity is driven by more offerings than by larger transactions. This is consistent with an early-stage reopening of the IPO market, with investor appetite remaining selective. Momentum is returning, though not yet at scale.

For companies considering a public listing, current conditions indicate that while the U.S. market is becoming more accessible, success depends on strong positioning, sector alignment and preparedness to meet investor expectations in a discerning environment.

Figure 1: Number of IPOs and Transaction Values ($B) — United States

| 1Q26 | Transaction Values | Number of IPOs |

|---|---|---|

| QoQ | 0% | 36% |

| YoY | 91% | 78% |

Source: S&P Capital IQ Pro, FTI Consulting Analysis

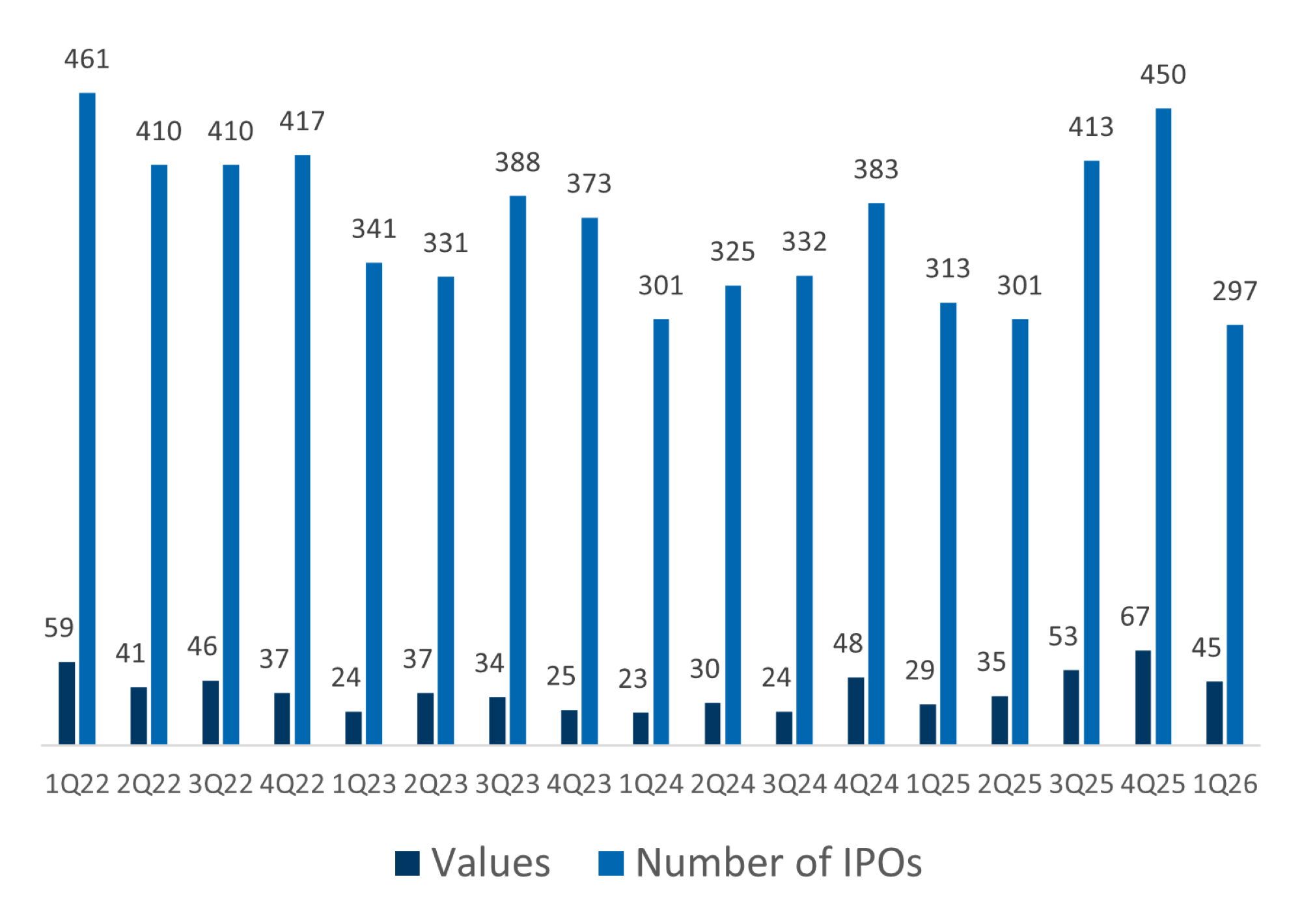

Global Market Overview

Global IPO activity moderated in the first quarter of 2026, with deal volume declining 34% and transaction values decreasing 33% compared with the fourth quarter of 2025. This pullback follows elevated activity in late 2025 and reflects a pullback from elevated levels rather than a sustained recovery trend.

Despite the QoQ decline, transaction values remained 55% above the first quarter of 2025, indicating that overall capital raised continues to exceed prior-year levels, even as deal volume has softened.

The uneven regional performance is likely influenced by ongoing geopolitical uncertainty, affecting investor confidence and cross-border capital flows. As a result, IPO activity outside the United States is more volatile, with recovery trends varying by region and sector. Consequently, recovery remains highly sensitive to external shocks.

For executives evaluating IPO timing, global markets are more volatile and time-sensitive than U.S. markets, with heightened sensitivity to macroeconomic and geopolitical developments that shape issuance conditions.

Figure 2: Number of IPOs and Transaction Values ($B) — Global

| 1Q26 | Transaction Values | Number of IPOs |

|---|---|---|

| QoQ | -33% | -34% |

| YoY | 55% | -5% |

Source: S&P Capital IQ Pro, FTI Consulting Analysis

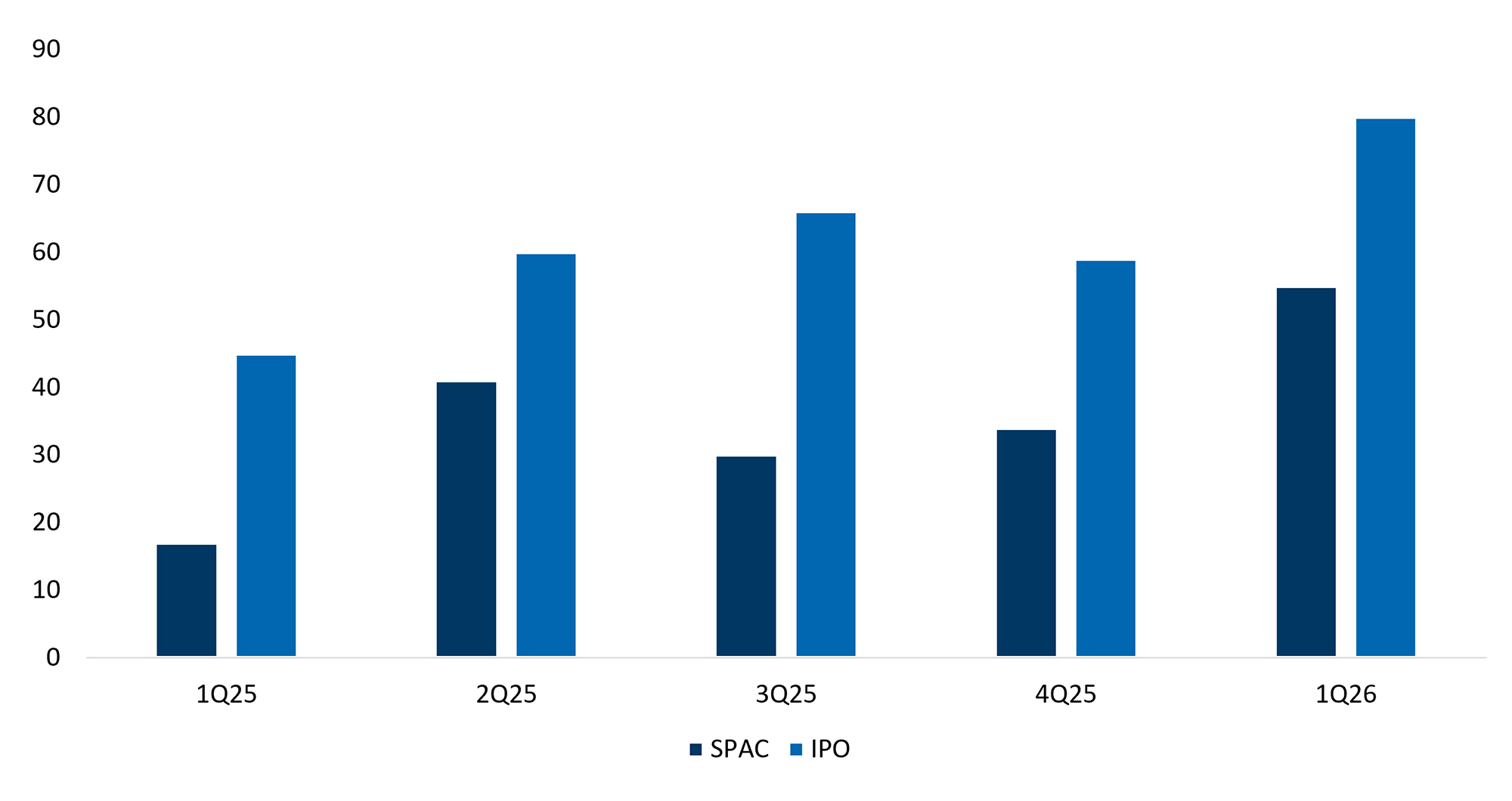

U.S. SPAC vs. Traditional IPO Activity

SPACs accounted for 69% of U.S. IPO deal volume in the first quarter of 2026, increasing from 58% in the fourth quarter of 2025. While traditional IPO activity also grew in absolute terms during the quarter, the disproportionate rise in SPAC issuance reflects a shift in the composition of market activity.

The rising share of SPAC transactions reinforces the view that traditional IPO markets remain selective, particularly for larger or more complex offerings. This dynamic is driving issuers to prioritize execution certainty over valuation optimization. As a result, SPACs continue to serve as an alternative pathway for companies seeking greater flexibility and execution certainty in accessing public markets. Alternative structures are filling gaps left by a still-constrained IPO market.

For executives evaluating public market entry, the continued prevalence of SPAC structures highlights the importance of evaluating multiple pathways to liquidity, particularly in an environment where market receptivity can vary significantly by company profile, sector and transaction size.

Figure 3: SPACs vs. IPOs — United States (1Q26)

| 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 |

|---|---|---|---|---|

| 38% | 68% | 45% | 58% | 69% |

Source: S&P Capital IQ Pro, FTI Consulting Analysis

Sector and Regional Insights

IPO activity in the first quarter of 2026 remained concentrated in a limited number of sectors, highlighting continued selectivity in investor demand. In the United States, healthcare accounted for 40% of the top 10 IPOs by volume, while the largest transaction occurred in the industrials sector.

In Europe, IPO activity was more heavily concentrated in the industrials sector, which accounted for the majority of the top transactions, including the quarter’s largest deal.

Sector concentration in both regions reflects continued narrow investor demand, with capital flowing to sectors perceived as defensive or aligned with long-term growth. For issuers, this reinforces the need for clear sector positioning and the development of an equity story, particularly in a market where capital is not yet widely distributed.

Top 10 IPOs (1Q26) — United States

| Company Name | Transaction Value ($M) | Industry |

|---|---|---|

| Forgent Power Solutions, Inc. | 1,738.80 | Industrials |

| Janus Living, Inc. | 966.00 | Real Estate |

| EquipmentShare.com Inc. | 859.34 | Industrials |

| York Space Systems, Inc. | 629.00 | Industrials |

| SOLV Energy, Inc. | 589.38 | Energy and Utilities |

| Minimed Group, Inc. | 560.00 | Healthcare |

| Generate Biomedicines, Inc. | 400.00 | Healthcare |

| Eikon Therapeutics, Inc. | 381.20 | Healthcare |

| Bob’s Discount Furniture, Inc. | 380.25 | Consumer |

| Aktis Oncology, Inc. | 365.36 | Healthcare |

Source: S&P Capital IQ Pro, FTI Consulting Analysis

Top 10 IPOs (1Q26) — Europe

| Company Name | Transaction Value ($M) | Industry |

|---|---|---|

| CSG N.V. | 4,467.96 | Industrials |

| Capital Tankers Corp. | 502.73 | Energy and Utilities |

| Vincorion SE | 346.04 | Industrials |

| ASTA Energy Solutions AG | 227.14 | Industrials |

| AgomAb Therapeutics NV | 200.00 | Healthcare |

| Gabler Group AG | 154.47 | Industrials |

| Electro-Alfa International S.A. | 136.51 | Industrials |

| General Oceans ASA | 108.40 | TMT |

| Ata Turizm | 71.66 | Industrials |

| Pelagic Credit Plc | 57.56 | Financial Services |

Source: S&P Capital IQ Pro, FTI Consulting Analysis

Looking Ahead

IPO market conditions in the first quarter of 2026 demonstrate an early-stage reopening that remains uneven across regions and sectors. While increased U.S. activity suggests improved access, global issuance trends remain volatile and sensitive to macroeconomic and geopolitical factors.

For executives considering a public listing, the environment offers a potential window of opportunity, especially in the United States. Still, selectivity prevails and success depends on company-specific factors such as sector alignment, scale and readiness. Prevalent SPAC transactions and sector concentration further show that capital access is not yet broad-based.

In this context, companies that are well-prepared and able to move quickly may be better positioned to seize favorable windows, while those delaying may face continued uncertainty in timing and valuation outcomes.

Related Insights

Published

May 11, 2026

Key Contacts

Key Contacts

Senior Managing Director, Co-Leader of SEC Accounting & Advisory

Senior Managing Director, Global Head of M&A

Senior Managing Director