Cost as a Design Choice

How Private Equity and Corporates Use Cost To Win Across the Business Lifecycle

-

June 05, 2026

-

In today’s environment, cost discipline is no longer just a defensive exercise. Persistent margin pressure, elevated financing costs and rising investment requirements around artificial intelligence (“AI”) and digital transformation are forcing both private equity (“PE”) sponsors and corporates to rethink how operating models are built and sustained.

Cost transformation is most effective when treated as a continuous, strategic capability rather than a reactive response to cost pressures. Organizations that embed cost discipline into their operating model design, instead of reactively adjusting it in response to external forces, are better positioned to sustain performance throughout the business lifecycle. Whether navigating growth performance, turnaround situations or transaction events, organizations that continuously reassess cost structures are typically better positioned to preserve performance and maintain optionality.

While PE sponsors and corporates may approach cost from different starting points, both face the same underlying challenge: complexity accumulates quietly over time. Growth, acquisitions, overlapping systems and incremental organizational decisions can create structural inefficiencies that remain hidden until margin pressure, liquidity constraints or transactions expose them.

Cost Transformation as a Lifecycle Capability

Cost programs can underdeliver when they are episodic, narrowly scoped and disconnected from strategy. In discussions with client stakeholders, senior executives often express frustration with missed cost‑reduction goals, driven by fragmented initiatives, weak governance, limited bottom-up validation and system constraints that make it difficult to trace savings to the bottom line.

A sustainable cost transformation program is better viewed as a continuous improvement journey, rather than a one-time initiative. It requires a thorough understanding of the operational and structural levers that drive performance, alongside management’s ability to refine optimization priorities as business requirements continue to evolve. Incentives play a critical role. Aligning performance expectations with value creation, instead of budget adherence, helps ensure that cost actions are sustained and measurable.

PE sponsors and corporates start from different vantage points. PE sponsors typically underwrite deals with explicit value‑creation plans in which cost, pricing, working capital and capital allocation are tightly linked and tracked at the board level. Corporates may preserve greater flexibility in overhead, shared services and research and development to support brands, innovation and a broader set of stakeholders.

Despite these differences, both face the same underlying challenge: complexity accumulates quietly over time, particularly after periods of growth or mergers and acquisitions (“M&A”) activity. Growth can mask inefficiencies for years until margin pressure, liquidity constraints or transactions expose structural cost issues that have already become embedded in an organization’s operating model.

The organizations that outperform across the business lifecycle are increasingly treating cost differently. Rather than viewing cost as a periodic restructuring exercise, they continuously redesign cost structures to align with growth priorities, operational realities and long-term value-creation objectives.

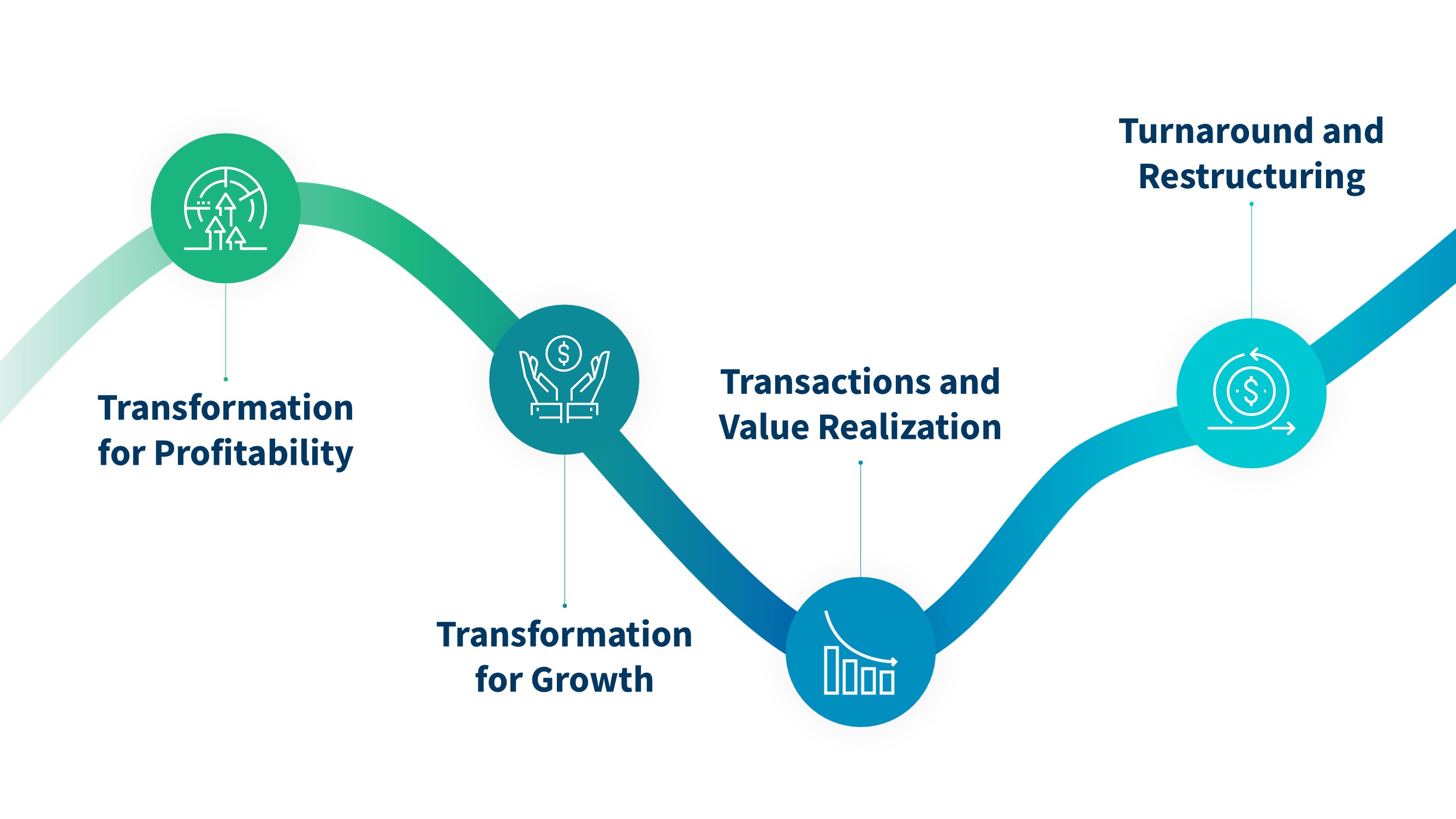

Lifecycle Stages and the Shape of Cost Transformation

Cost priorities evolve significantly across growth, performance improvement, turnaround and transaction situations. In each stage, cost is not only a constraint but also a lever that shapes how the business operates and scales.

Source: FTI Consulting

Transformation for Growth: Funding Scale Without Future Bloat

In growth phases, the core question is not “Where can we cut?” but “How can we scale without embedding future inefficiencies?”

In growth businesses, sales can outpace the development of processes and systems, with selling, general and administrative expenses rising faster than revenue. Complexity rarely arrives all at once. It accumulates gradually through overlapping systems, disconnected processes and incremental hiring decisions that become harder to unwind over time.

PE-backed companies typically prioritize early discipline to prevent complexity from constraining scale. This usually includes simplifying the operating model, improving data visibility and maintaining tight alignment between headcount growth and revenue. Increasingly, digital and AI-enabled approaches support scaling revenue while limiting cost creep.

Corporates often pursue the same levers, but with greater emphasis on preserving culture and optionality. They may accept a higher overhead buffer to support internal mobility, innovation projects and global governance, using shared services and automation to manage indirect costs.

The organizations that outperform during growth introduce cost discipline before external pressure forces them to do so.

Transformation for Performance: Protecting Profitability While Sharpening the Business

As organizations enter performance improvement environments, transformation priorities shift toward restoring performance while preserving competitive positioning.

For PE owners, this phase can trigger rapid, high-impact actions, including headcount reductions, role and process simplification and product and operational rationalization. Sponsors are usually more willing to trade marginal volume for a healthier product mix, prune customer segments and close underperforming sites if it protects earnings before interest, taxes, depreciation and amortization, and covenant headroom.

Corporates generally face a more complex balancing act. They must protect brand equity, customer relationships and regulatory commitments while still delivering financial performance. Strategic cost programs in this context often combine procurement optimization, pricing improvements and productivity initiatives with targeted reinvestment into differentiating capabilities.

The most effective organizations do not approach margin pressure as a temporary cost-cutting exercise. They use it as an opportunity to simplify operations, redeploy resources and strengthen long-term competitiveness.

Turnaround and Restructuring: Stabilizing Liquidity and Resetting to the Core

As liquidity tightens, cost actions become more immediate and focused on stabilizing business performance.

In this environment, cost transformation turns into triage. Leading actions focus on preserving cash, suspending noncritical expenses, rapidly reducing costs and evaluating asset sales or portfolio exits. In turnaround environments, PE sponsors often make sharper decisions around restructuring, operational stabilization and exit scenarios.

Corporates may have greater degrees of freedom, including cross‑subsidization, carve-outs, access to capital markets or leveraging political and regulatory relationships. These options, however, can also introduce complexity and delay. Distressed corporates must orchestrate cost actions alongside legal, labor and reputational considerations, often within formal restructuring regimes that constrain the sequence and pace of moves.

The organizations that emerge strongest from distress are rarely the ones that cut the deepest. They are the ones that use the moment to reset operating models, simplify portfolios and refocus around core value drivers.

By the time liquidity pressure becomes visible, operational complexity has already been building beneath the surface for years.

Transactions and Value Realization: Capturing Synergies and Eliminating Stranded Costs

Transactions are moments in a business lifecycle when cost structures can be reshaped most dramatically. Many deals underwrite substantial cost synergies through organizational consolidation, shared services integration and rationalization of information technology. Yet, realizing transaction value requires sustained focus on synergy execution and stranded-cost removal.

PE sponsors generally bring a more aggressive, time‑bound stance to transaction‑related costs. Their playbooks typically include quantified targets embedded in deal models, clear Day 1 and Year 1 milestones and dedicated integration or separation governance. For carve‑outs, sponsors typically focus on standing up the new company at an efficient cost base, exiting transition services agreements quickly and modernizing systems and operating models in parallel.

Large corporates, drawing on broad M&A experience, often set ambitious synergy targets and assume integration into existing infrastructure will be seamless. However, realizing these synergies requires disciplined execution and sustained operational focus long after the transaction closes.

In transactions, value leakage rarely comes from identifying the wrong synergies. It typically stems from a loss of execution discipline after close.

The most effective acquirers pair integration playbooks with dedicated stranded-cost and synergy-execution workstreams that remain active well beyond the first 100 days.

Building an Early Warning “Cost Radar”

One of the most consistent themes across successful transformation efforts is visibility. Organizations that identify pressure signals early maintain greater strategic flexibility and a broader range of options before intervention becomes urgent.

Many companies still rely too heavily on lagging indicators, responding only after earnings deteriorate, refinancing becomes difficult or liquidity tightens. By then, the cost structure is often far more difficult to unwind.

An effective “cost radar” monitors not only profitability and liquidity, but also the operational and organizational complexity building beneath the surface. That includes:

- Margin and cash conversion trends

- Revenue per employee and operational throughput

- Organizational layers and decision-making bottlenecks

- Vendor proliferation and fragmented systems

Many organizations do not have a pure cost problem. They have a complexity problem masquerading as a cost problem.

The organizations that elevate cost structure discussions into regular operating reviews, strategic planning cycles and board-level conversations are often better positioned to act proactively instead of reacting under pressure.

Why a Cost Takeout Mindset Is Now Non-Negotiable

The shift from tactical cost-cutting to strategic cost design is accelerating. Organizations are increasingly combining traditional levers such as procurement optimization and organizational redesign with AI-driven automation, advanced analytics and digital transformation to fundamentally reshape operating models.

For PE-backed businesses, this supports faster value creation and stronger exit outcomes. For corporates, it creates flexibility to reinvest in growth while improving resilience through economic cycles.

Viewed through a lifecycle lens, the implications are clear. Cost is not simply reduced; it is reshaped. In growth phases, transformation supports scalable expansion. In times of performance pressure, it enables reinvestment and operational simplification. In turnaround situations, it stabilizes the business. In transactions, it determines how much value is ultimately realized.

The organizations that outperform are rarely the ones that cut the deepest. They continuously redesign cost structures before pressure forces action.

Related Insights

Related Information

Published

June 05, 2026

Key Contacts

Key Contacts

Senior Managing Director

Senior Managing Director, Co-Leader of U.S. Business Transformation

Senior Managing Director