Media and Entertainment M&A

Closing 2025, Looking Ahead to 2026

-

February 26, 2026

-

Media and entertainment dealmaking in 2025 felt like a late-cycle trough in volume but not in ambition — with fewer transactions overall, the market took a tilt toward larger “must-do” consolidation and more creativity in structure and financing. The biggest driver is still the same macro story: higher (but easing) cost of capital, easing bid/ask spreads and slow processes, while strategic imperatives (scale, IP, data, distribution, AI enablement) kept marquee deals moving.

“Hot” vs. “Cold” Heading Into 2026

Deal volume in 2025 remained soft. FTI Consulting’s proprietary deal-flow tracking shows media & entertainment (M&E) deal volumes down ~25% YTD 2025 vs. prior year, despite modest stabilization in Q3. This decrease aligns with the broader global backdrop: Refinitiv/LSEG data shows global announced M&A volumes down ~10% YoY through mid-2025, even as total deal value increased.1

M&E Deal Activity Has Contracted in 2025, With YTD Volumes Down ~25% vs, Last Year Despite Modest Q3 Stabilization

Q1 2024 - Q3 2025 M&E Deal Count

# of Deal Announcements

Source: FTI Consulting Research & Analysis using CapIQ

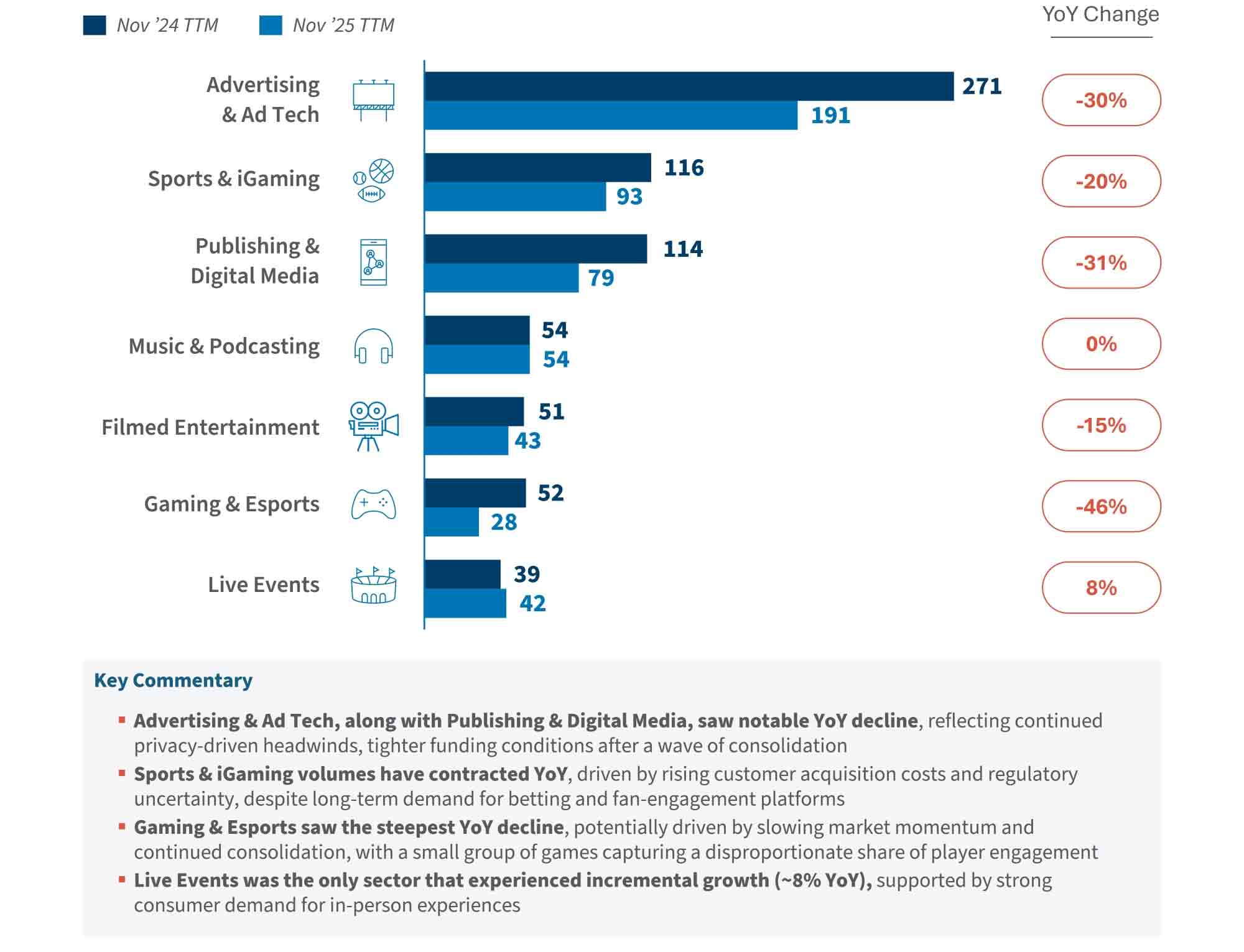

Sub-sector divergence underscores that the “market” isn’t one market. On an LTM basis (Nov ’24–Nov ’25), FTI Consulting analysis shows declines across most M&E sub-sectors, with Live Events up ~8% YoY and Music/Podcasting roughly flat, while Gaming & Esports fell ~46% YoY and Advertising/Ad Tech and Publishing/Digital Media were down meaningfully.

Trailing Twelve Months (“TTM”) Deals Activity From Nov ’24 to Nov ’25

Declined Across Most M&E Sub-Sectors, With Only Live Events and Music & Podcasting Showing Signs of YoY Growth

TTM Deal Volume From Nov ’24 to Nov ’25

Number of Closed and Announced Deals by Sub-Sector

Source: FTI Consulting Analysis using Publicly-available Information

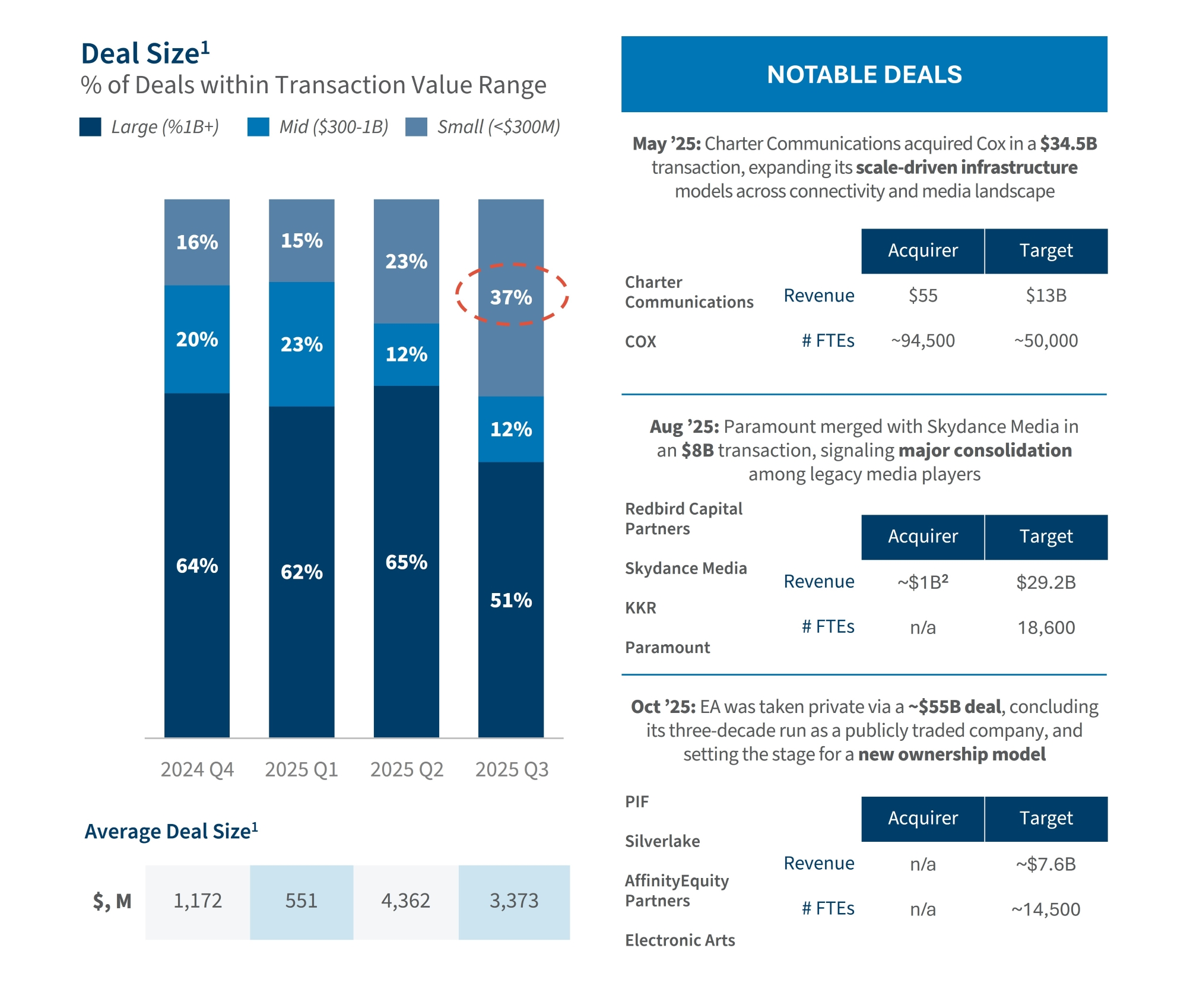

By contrast, deal sizes and values increased. Even as volumes contracted, transaction values and headline deal sizes strengthened — a classic pattern late in a cycle when capital concentrates into “conviction” assets, assets that investors view as strategically important. FTI Consulting data shows a rising share of $1B+ deals and average announced deal sizes spiking in 2025 (e.g., $4.4B in Q2 2025; $3.4B in Q3 2025 for deals with available values). This trend mirrors broader market data from S&P Global, which showed Q1 2025 announced deal values up (~+15% YoY) even as deal counts fell.2

However, Transaction Values Have Grown, As Recent Quarters Show a Surge in $1B+ Deals and a Growing Share of Activity Concentrated in High-Value, Marquee Assets

Note: (1) Deal values are only reflective of announced deals with publicly available financials; (2) Only includes revenue of Skydance Media Source: FTI Consulting Analysis using Publicly-available Information

What’s Driving the Shift (and How Buyers Are Adapting)

- Capital discipline + “structure is back.” Buyers are bridging valuation gaps with earn-outs, seller notes, minority-to-control pathways and more explicit performance triggers. In PE specifically, improved credit conditions plus creative structures are enabling larger deals again — data cited by Bloomberg shows deal value rebounded sharply in 2025, led by transactions above $1B.3

- “Consolidate or specialize” in legacy media. Streaming maturation and bundling/aggregation logic are pushing legacy media companies toward scale plays, asset swaps and joint ventures (often easier to underwrite than pure growth). MoffettNathanson has noted that premium streaming has entered a margin-optimization phase, reinforcing incentives for consolidation and portfolio rationalization.4

- Tech enablement is the fastest path to multiple expansion. In advertising and marketing services, “capabilities M&A” is increasingly favored over geographic roll-ups. FTI Consulting’s advertising analyst survey finds 64% believe the right M&A focus is offering new or expanded capabilities (vs. footprint or talent). Importantly, public holdcos still face a weighted-average 7–11% “conglomerate discount,” a structural incentive for portfolio reshaping and targeted acquisitions.

- Film/TV production remains a demand headwind. Content pipelines are recovering unevenly and remain well below peak. For context, FTI Consulting’s proprietary film and series production forecast indicates U.S. production was ~40% below peak-TV levels (Q2 2024 vs. Q2 2022)5

- That softness continues to pressure production services, certain studios/IP owners and adjacent vendor ecosystems — keeping more deals in “restructuring/carve-out/consolidation” mode than in growth mode.

What To Expect in 2026

- A cyclical rebound in volumes (modest), driven by rate relief + deployment pressure. With private-market dry powder still massive (PitchBook pegged global private-market dry powder just under ~$4T at end-2024),6 sponsors have real incentive to move from watching to buying — especially as financing windows stay open.

- Consolidation-led deal flow dominates in slower-growth sub-sectors (publishing/digital media, certain adtech stacks, scaled services), with bigger emphasis on cost takeout, data monetization and distribution leverage.

- Selective “innovation deals” are poised to outperform: expect more activity where assets can scale quickly or unlock strategic buyers’ priorities — AI ecosystem tooling (search optimization, creator tools, AI licensing marketplaces), retail media enablement, sports tech and digital out-of-home (DOOH) (benefiting from digitization and performance measurability).

- Advertising holdco portfolio simplification, capability buys and AI partnerships will be the ongoing response to challenges in performance from disintermediation by platform majors such as Meta (ranked a top concern by analysts in the FTI Consulting survey).

- Net: 2026 is less about “multiple expansion by narrative,” more about “multiple defense by execution.” Buyers will underwrite to cash generation, synergy certainty and measurable tech differentiation — then use structure to manage downside.

Footnotes:

1. Toole, Matthew, Lucille Jones, and Elaine Tan, “Report | The State of Global M&A: H1 2025,” LSEG (accessed February 11, 2026).

2. Toomey, Joseph, “Global M&A by the Numbers: Q1 2025,” S&P Global (May 14, 2025).

3. Davis, Michelle F. and David Carnevali, “M&A in 2025: A Year Defined by Megadeals,” Bloomberg (December 15, 2025).

4. Frankel, Daniel, “Streaming Wars settled for now, with Netflix on top – analyst,” StreamTV Insider (February 13, 2025).

5. Carras, Christi, “U.S. film and TV production down 40% from peak TV levels, report says,” Los Angeles Times (July 11, 2024).

6. Lai, Emily, “Dry powder is dwindling, but expect a fundraising rebound across four strategies,” PitchBook (September 22, 2025).

Published

February 26, 2026

Key Contacts

Key Contacts

Senior Managing Director