The Chemistry of Uncertainty

What is the Outlook for European Chemicals M&A in 2026?

-

07. Mai 2026

Herunterladen Download Dashboard

Download Dashboard

-

2025 will be remembered for significant chemicals mergers and acquisitions (“M&A”) activity in Europe, driven by companies’ portfolio optimization programs, exits from the European market, restructuring situations, large divestments and early consolidation across certain value chains. Although the total number of deals has continued to decline in this sector, several mega-deals significantly increased the overall transaction value in 2025. Structural challenges across the European chemicals industry are expected to persist, continuing to drive market exits, portfolio divestments and consolidation; however, the conflict in the Middle East adds another level of uncertainty to the M&A landscape in 2026.

From Small-Cap Divestments to Mega-Deals in 2025

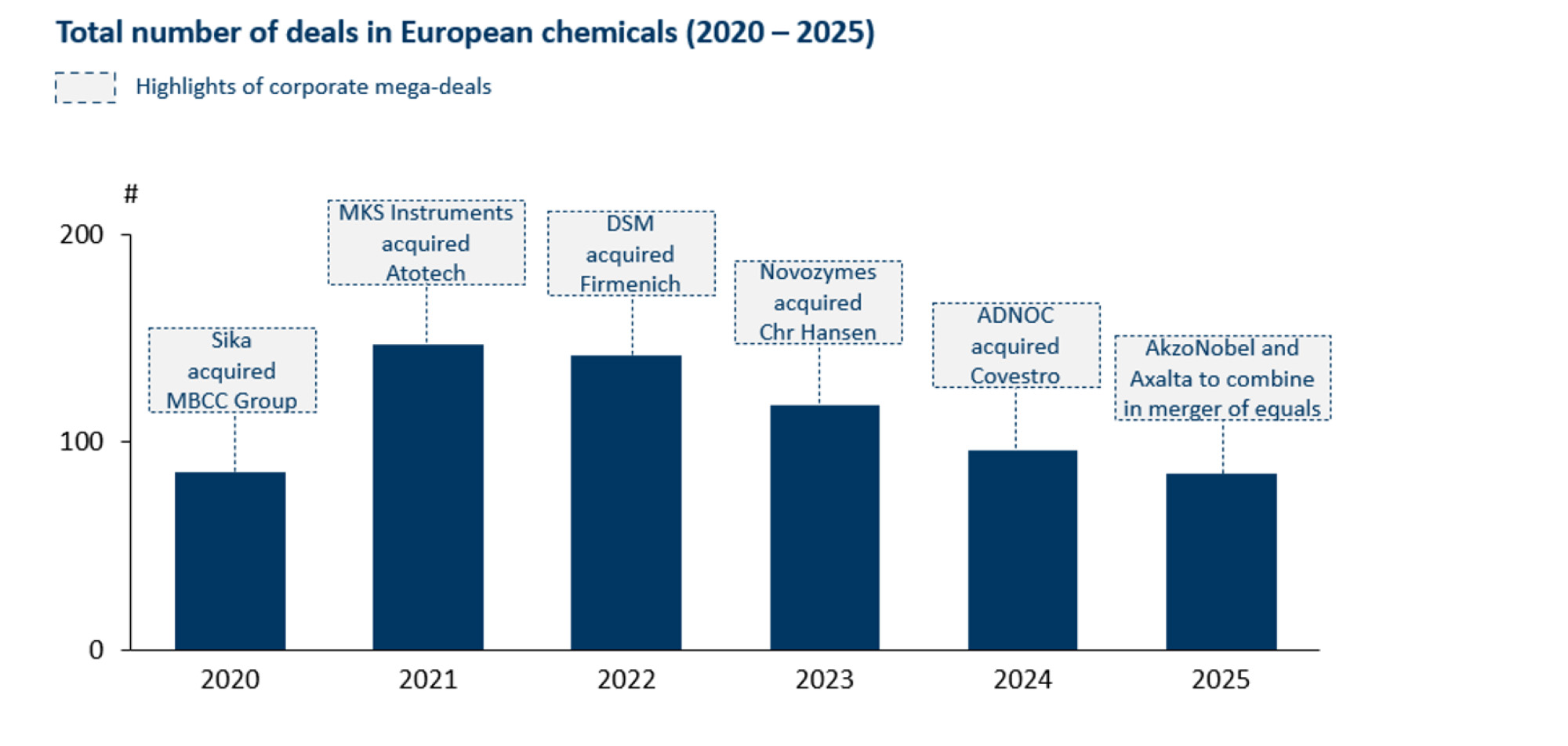

The European chemicals sector faced significant pressure throughout 2025, with a growing recognition that the challenges in the sector are structural rather than cyclical. The M&A market saw transactions across all formats — from small-cap portfolio divestments and fire sales to market exits and large-cap consolidation deals. Most prominently, this included the announced merger of equals between Akzo Nobel N.V. (“AksoNobel”) and Axalta Coating Systems Ltd. (“Axalta”).

Figure 1 - Total Number of Investments in European Chemicals (2020 – 2025)

Source: Mergermarket, FTI Consulting analysis

AkzoNobel, a paints and coatings producer with a long industrial heritage, and Axalta, originally carved out from the DuPont de Nemours, Inc. Performance Coatings business, announced an all-stock merger of equals in November 2025.1 The transaction will bring together two companies that have followed markedly different performance trajectories in recent years. AkzoNobel has faced sustained share price pressure since its mid-2021 peak and has launched several performance improvement initiatives to restore profitability and investor confidence. By contrast, Axalta — with a portfolio more heavily weighted toward automotive refinish coatings — has delivered stronger operational results, a performance trend that has been recognized by capital markets.

The combination has the potential to create a global coatings leader with significant scale and portfolio breadth, even if it will likely require portfolio reshaping measures, including a potential divestment of AkzoNobel’s decorative paints segment and regulatory remedies in overlapping markets. Nevertheless, the relatively muted initial reaction from investors, reflected in share price movements around the announcement, suggests that disciplined execution and effective post-merger integration will be essential to capture synergies and deliver expected shareholder value.

Complex Investments and Large Buy-Outs in 2025

In 2025, financial investors’ activities in European chemicals recovered to historical averages, although some notable deals featured pre-distressed assets. The sector attracted significant interest from hands-on turnaround-focused private equity investors, who became increasingly active in the sector, targeting underperforming or non-core assets with transformation potential.

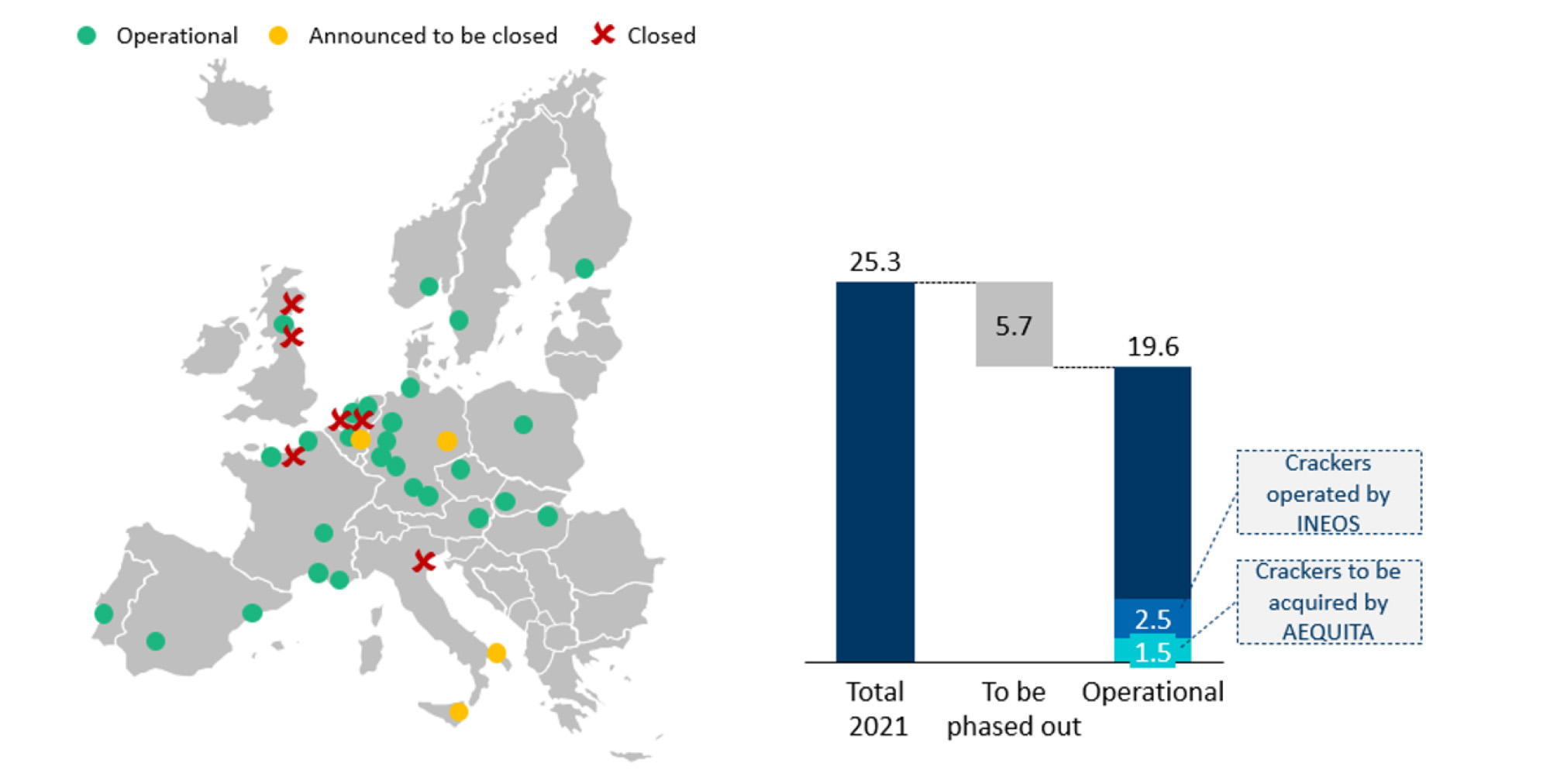

A case in point unfolded in the petrochemicals segment, where the European market has been marked by substantial domestic overcapacity in naphtha cracking and mounting pressure on profitability. Moreover, the anticipated 2027 start-up of INEOS’s new ethane cracker, with a capacity of 1.4 million tons per year, is set to add further pressure to the already strained industry margins.2 In response, several major ethylene producers initiated portfolio reviews that resulted in asset shutdowns and divestments.

Against this backdrop, Munich-based mid-cap private equity firm AEQUITA — previously focused on industrial goods businesses and with limited prior exposure to chemicals — announced deals to acquire olefins and polyolefins assets from LyondellBasell Industries N.V. and Saudi Basic Industries Corporation.3 Both transactions are structured with limited cash proceeds and include substantial seller support, highlighting the distressed nature of the assets.

Figure 2 - European Cracker Capacity (Kt Ethylene Per Year, Status as of 2025)

Source: Petrochemicals Europe, FTI Consulting analysis

The situation draws parallels to INEOS’s 2005 acquisition of petrochemical subsidiaries from BP p.l.c., a move that ultimately positioned INEOS as a major industry consolidator.4 Whether AEQUITA will follow a similar path and evolve into a new European consolidator for olefins and polyolefins, or instead pursue a more selective restructuring and turnaround strategy, remains an open question.

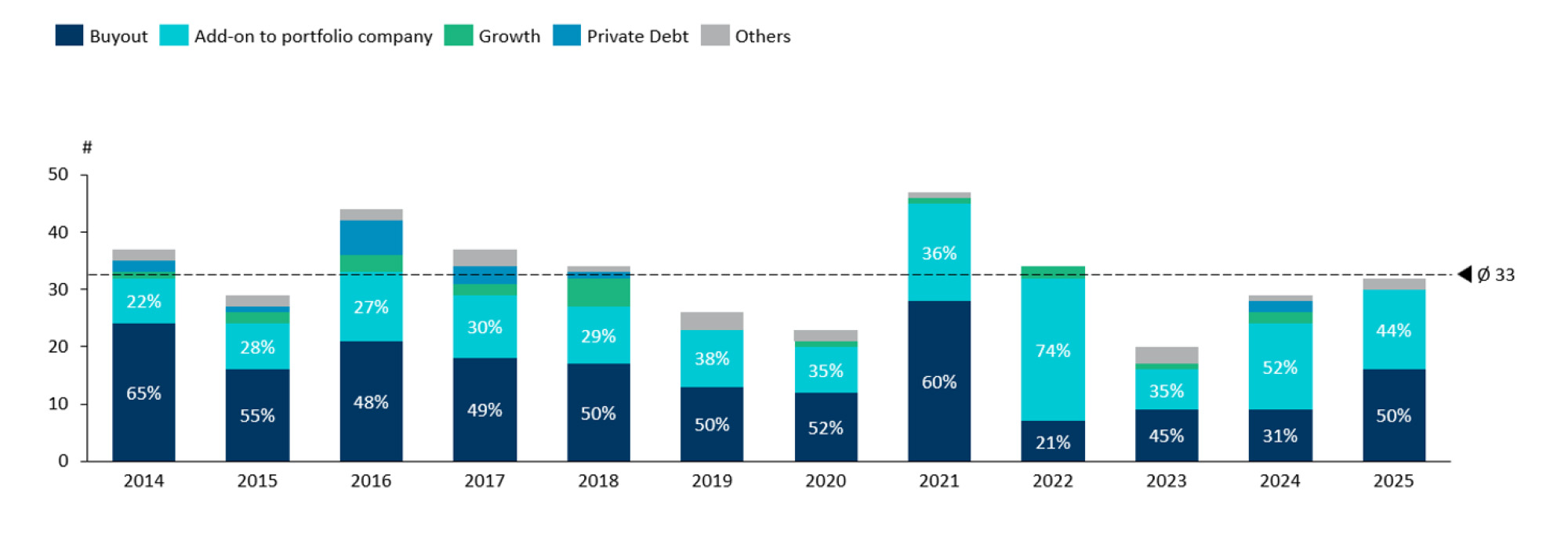

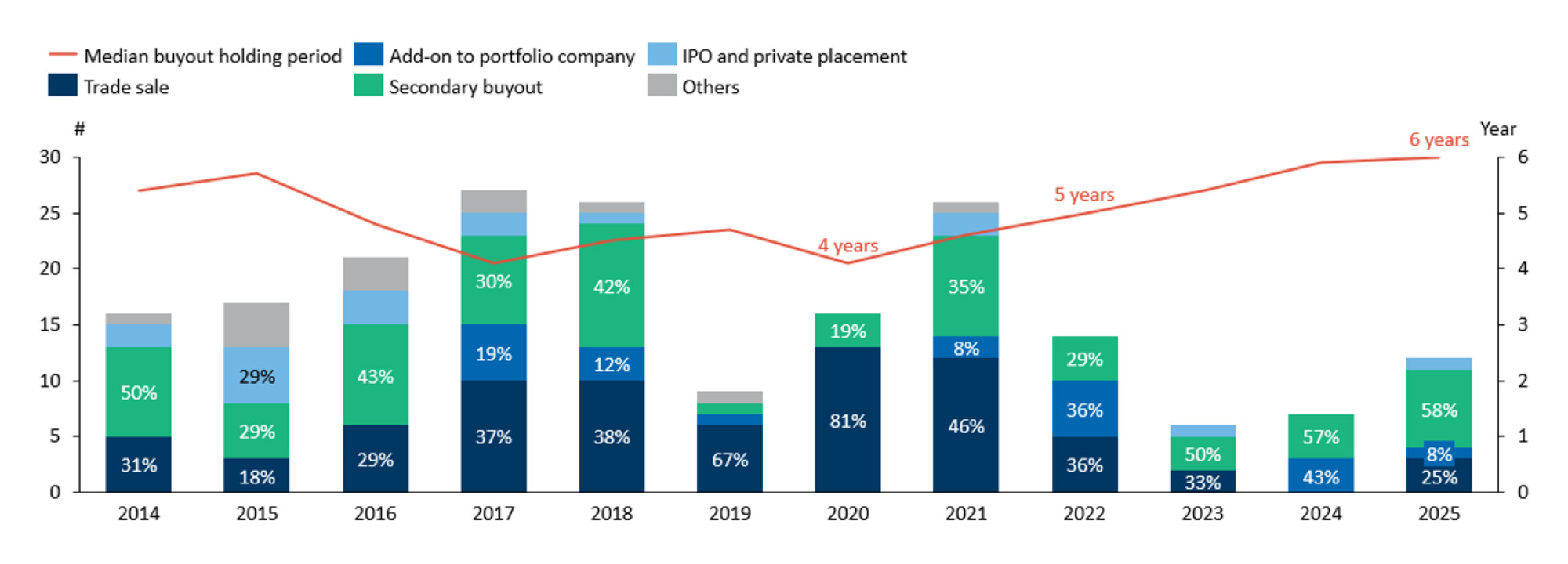

Figure 3 - Number of Financial Sponsor-Backed Investments By Deal Type (2014 – 2025)

Source: Preqin, FTI Consulting analysis

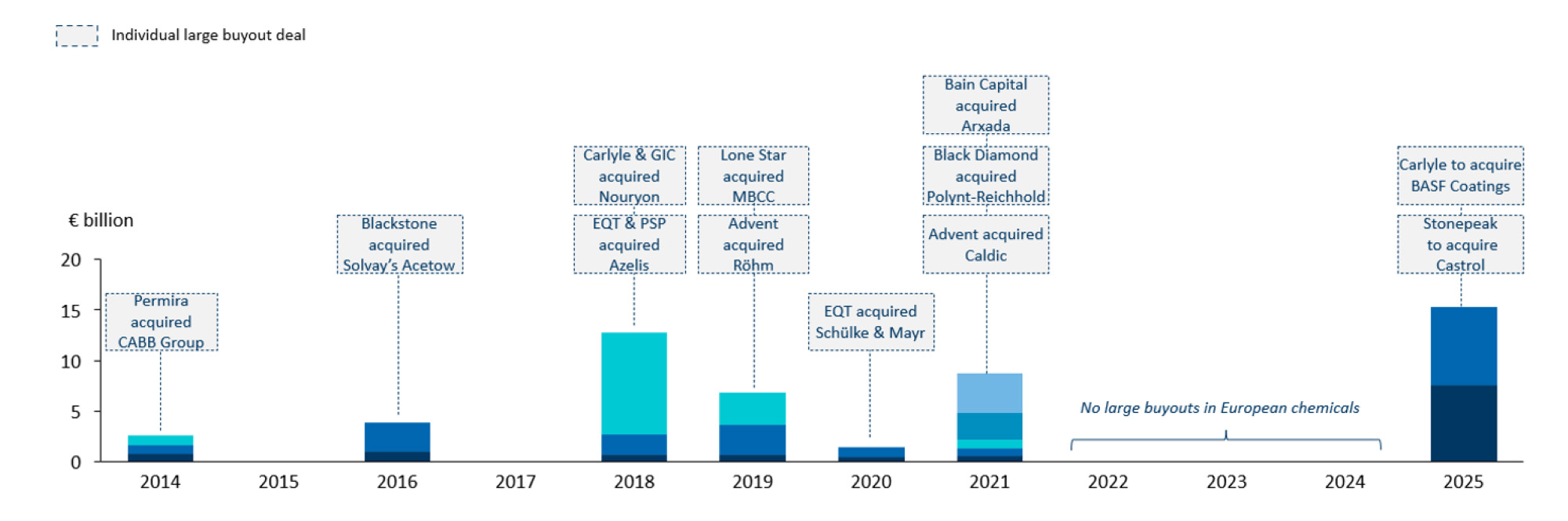

The European chemicals sector had not seen major buyout transactions from 2021 through 2025, largely due to a challenging dealmaking environment, characterized by elevated interest rates and persistent valuation gaps between buyers and sellers. However, following three relatively quiet years, financial investors returned to executing large-scale transactions in 2025. As European industry majors continued to optimize their portfolios and sharpen their focus on core businesses, several sizeable divestments came to market. Most notably, The Carlyle Group, Inc. (“Carlyle Group”) announced the acquisition of BASF Coatings, a division of BASF SE (“BASF”) and a global leader in automotive coatings and surface treatment.5

Figure 4 - Value of Large Buyouts in Chemicals (2014 – 2025)

Source: Preqin, FTI Consulting analysis

BASF outlined its intention to sharpen its strategic focus on core businesses during its 2024 Capital Markets Day, identifying several standalone units for potential divestment, including its Coatings division.6 Execution progressed rapidly in 2025: early in the year, BASF agreed to sell its South American decorative paints business, Suvinil, to global coatings leader Sherwin‑Williams Company.7 By year-end, the company had also reached an agreement to divest the remainder of its Coatings division to Carlyle Group at an enterprise value of €7.7 billion.

Carlyle Group brings relevant sector experience, having previously carved out Axalta from DuPont in 2013 and successfully listed it the following year.8 Looking ahead, several value creation levers are apparent, including potential portfolio separation and the divestment of the Surface Treatment business (the former Chemetall unit acquired by BASF in 2016). However, future exit pathways could prove more complex for the automotive coatings segment given the structurally-cyclical nature of underlying end markets.

Financial sponsor exit activity showed signs of recovery in 2025, driven primarily by transactions in agrochemicals and consumer-focused chemical segments, while divestments in upstream chemicals remained particularly difficult — especially for Europe-based assets. Exit processes in polymers and performance materials continued to face headwinds amid the prolonged downturn in the European chemicals industry, resulting in several failed auction processes and instances in which buyers withdrew from signed transactions due to rapidly deteriorating operating performance of target companies.

Figure 5 - Number of Divestments in Chemicals By Exit Type and Median Buyout Holding Period (2014 – 2025)

Source: Preqin, FTI Consulting analysis

In this environment, sponsors increasingly explored alternative exit routes, particularly for portfolio companies with geographically diversified footprints across the United States and Asia, where break-up strategies and partial divestments can unlock value. One example is CABB Group GmbH, which has been owned by Permira since 2014 and operates across Europe, the United States and China; the company pursued a selective divestment strategy through the sale of a U.S. production plant while retaining its broader international footprint.9

What’s Next? The Chemistry of Uncertainty

We remain cautious on the outlook for the European chemicals sector in 2026, as structural headwinds continue to remain. High energy and carbon costs, geopolitical tensions around the world, ongoing overcapacity in China and only a modest recovery in downstream demand are expected to keep pressure on margins, particularly in commodity and intermediate chemicals.

In recent years, in an effort to support this structurally and strategically important industry, the European Commission has continued to impose anti-dumping duties on imports of various chemicals from Asia, the Middle East, and the United States, although the broader, holistic impact on the sector’s competitiveness remains to be seen. The ongoing conflict in the Middle East is creating additional uncertainty due to mixed dynamics. On the one hand, European chemical companies are likely to struggle to fully pass through increases in oil and gas prices to customers, and on the other hand, constrained production in the Middle East and a surge in Asian feedstock prices across a range of commodity chemicals could improve Europe’s competitive position.

While the Middle East conflict could postpone some M&A activity, we expect companies to make strategic decisions based on the fundamentals of the European chemicals sector, with portfolio streamlining, restructuring, and selective consolidation defining the deal landscape — particularly in petrochemicals and polyolefins, coatings and paints, fertilizers and crop protection and ingredients.

In summary, while organic growth in the industry will remain muted, 2026 may bring forced sales of high-quality assets from under-pressure corporates, alongside consolidation plays in overcapacity or margin-squeezed chains. Divestment decisions may be driven more by a company’s geographical footprint than by cost position alone, with global players potentially continuing to exit Europe to focus on the United States and Asian markets.

Ongoing financial pressure may also force companies to divest healthier, larger business units. These dynamics, combined with potential remedies arising from larger-scale consolidations, could create attractive opportunities for traditional private equity firms, including those that have historically avoided restructuring situations.

Footnotes:

1: “AkzoNobel and Axalta to combine in all-stock merger of equals, creating a premier global coatings company,” AkzoNobel (Nov. 18, 2025), AkzoNobel and Axalta to combine in all-stock merger of equals, creating a premier global coatings company | AkzoNobel.

2: “Project ONE groundbreaking,” INEOS (n.d.).

3: “LyondellBasell enters into an agreement and exclusive negotiations with AEQUITA for the sale of four European Strategic Assessment assets," LyondellBasell (June 5, 2025), and "SABIC further optimizes its portfolio for long-term sustainable growth, divests its European Petrochemical (EP) business and its Engineering Thermoplastics (ETP) business in the Americas and Europe," SABIC (Jan. 8, 2026).

4: "INEOS completes purchase of BP’s Innovene business for $9bn," INEOS (Dec. 16, 2005), .

5: "BASF and Carlyle reach binding transaction agreement on coatings business to create a leading standalone company," BASF (Oct. 10, 2025).

6: "BASF Capital Markets Day 2024 – Coatings," BASF (Sept. 27, 2024).

7: “BASF completes the sale of its Brazilian decorative paints business to Sherwin-Williams,” BASF (Oct. 1, 2025), BASF completes the sale of its Brazilian decorative paints business to Sherwin-Williams.

8: "The Carlyle Group Completes Acquisition of DuPont Performance Coatings," The Carlyle Group (Feb. 3, 2013).

9: "Sale of Jayhawk Fine Chemicals: The CABB Group signs a definitive agreement with Anupam Rasayan India Ltd.," CABB Group (Dec. 9, 2025).

Related Insights

Datum

07. Mai 2026

Ansprechpartner

Ansprechpartner

Senior Managing Director

Senior Managing Director

Managing Director

Managing Director