The Economics of Minority Stakes in Merger Assessments

-

08. Apr 2026

-

In December 2025, the Competition Commission published draft guidelines on minority shareholder protections. The guidelines set out its approach to assessing transactions that would not ordinarily “cross the bright line of merger notification”1 but would amount to the acquisition of a form of control by a minority shareholder in terms of the Competition Act. This has become an important area of merger assessment, extending regulatory scrutiny beyond traditional majority acquisitions.

The recent Vodacom/Maziv transaction, which saw Vodacom acquire a minority shareholding in Maziv, presents an informative case study of partial ownership assessments in practice. While the acquisition of a minority shareholding typically does not require notification, this transaction was notified due to negative control provisions in the shareholder agreement. For this transaction, FTI Consulting was briefed by DLA Piper to assess the economic impact of the proposed minority shareholding.

The Competition Commission’s Guidance on Minority Shareholder Protections

Competition authorities recognise that in some cases non-controlling investments can raise potential competition concerns.2 Minority shareholdings may, depending on the circumstances, warrant scrutiny based on their potential competitive effects.

The Commission’s guidelines distinguish between ordinary investment safeguards, which protect minority shareholders’ financial interests, and rights that effectively enable strategic control over competitively significant decisions, such as veto rights over a firm’s budget, business plan or key executive appointments.3 The test is whether the minority protections provide the shareholder with a right to steer the firm or appoint persons who can direct its strategic orientation. The guidelines recognise that determining whether such a minority shareholder can influence strategic decisions and commercial strategies of a target firm is a factual question that must be determined on a case-by-case basis.4

Theoretical Foundations: When Minority Stakes Matter

The economic framework for analysing partial ownership recognises that financial interest and corporate control represent distinct yet interconnected dimensions of competitive influence. Economic analysis reveals that partial ownership interests can represent more than passive financial investments: in some cases, they can alter firms’ competitive incentives and reshape competitive dynamics.

Unlike full mergers, whereby control transfers automatically, partial ownership can create intricate scenarios in which firms can exercise varying degrees of influence over competing entities without assuming full operational responsibility. This can result in a range of competitive effects, from a negligible impact to an outcome that may even be potentially more harmful than an outright acquisition.5

These competitive effects depend critically on how financial interest and corporate control combine in specific transactions. Financial interest refers to a firm’s entitlement to share in another firm’s profits, while corporate control involves the ability to influence competitive decision-making such as pricing strategies, product selection and market entry decisions.6 These elements can align in various configurations: a firm might hold substantial financial interest with minimal control rights, or conversely, exercise disproportionate influence through governance mechanisms despite modest financial stakes.

Governance structures may introduce additional complexity by creating scenarios where minority shareholders wield influence exceeding their nominal ownership percentages. This can occur through mechanisms like strategic board compositions, veto rights or information-sharing arrangements. In these cases, the competitive assessment must examine the structure of governance rights and their practical implications for competitive conduct. Even if the test for control is met, the financial incentive to exercise that control still has to be investigated (i.e., whether it would be profitable). The Vodacom/Maziv transaction provides an illustration of an assessment of partial ownership in practice.

The Structure of the Vodacom/Maziv Transaction

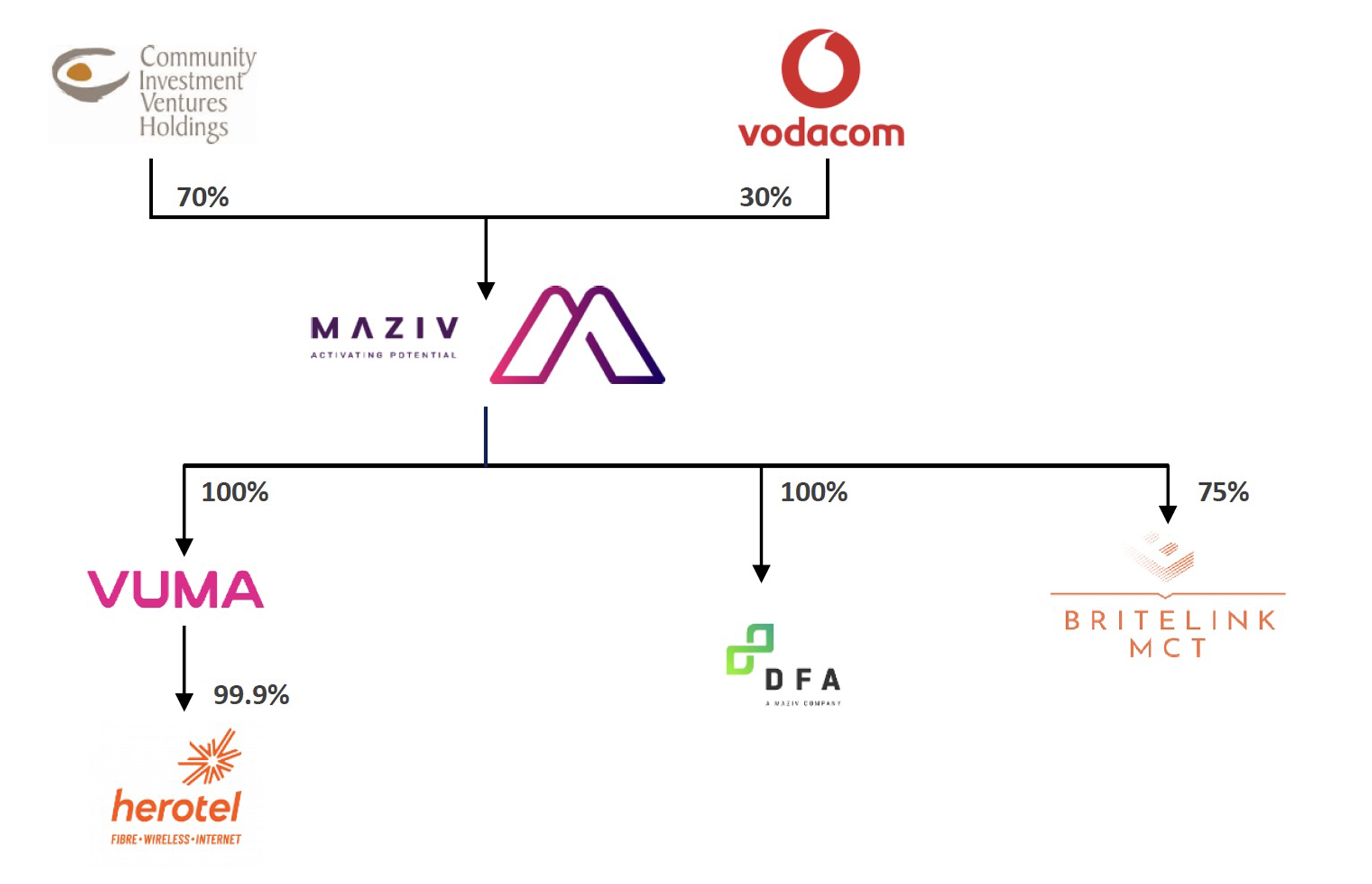

The proposed transaction involved Vodacom acquiring a 30% shareholding7 in Maziv, whose key subsidiaries include DFA (a wholesale open-access fibre infrastructure provider) and Vumatel (a fibre-to-the-home network operator). The transaction was filed as a merger because the transaction would give Vodacom joint control over Maziv through a minority shareholding and certain governance rights. This shareholding structure is shown in Figure 1.

The structure of the transaction was critical to assessing its competitive implications. This was not a vertical integration of an upstream infrastructure player and a downstream mobile retail player. Rather, it represented a strategic minority investment by Vodacom intended to enable Maziv to accelerate fibre deployment, particularly in underserved low-income areas. Indeed, Vodacom continues to operate its mobile and internet service provider businesses independently, while Maziv maintains separate operations focused on wholesale fibre infrastructure provision.

Despite the absence of true vertical integration, the competition authorities investigated competitive concerns associated with foreclosure theories of harm — centrally, that Vodacom’s minority control could enable it to influence Maziv in ways that disadvantage Vodacom’s rivals (for example, by inducing Maziv to raise their costs or to partially foreclose access to its fibre infrastructure). There were also concerns that the arrangement could give Vodacom access to commercially sensitive information about rivals’ infrastructure requirements.

Figure 1: Maziv Shareholding Structure

Source: Remgro presentation (2025)

FTI Consulting’s economic analysis employed a rigorous framework to evaluate these vertical theories of harm using the standard framework of ability, incentive and effect.8 The analysis showed that for the foreclosure theories to be credible, one would need to demonstrate that Maziv would sacrifice its own profits to create competitive advantages for Vodacom’s downstream operations. Drawing on extensive documentary evidence, internal strategy materials, financial modelling and expert testimony, FTI Consulting demonstrated that the transaction’s structure and economic fundamentals did not support the foreclosure theories of harm.

Ultimately, the analysis concluded that Maziv would not be able to recoup any foregone upstream profits through increased downstream profits at Vodacom, as Maziv would hold no shareholding in Vodacom post-transaction. Maziv would retain strong incentives to maintain non-discriminatory open access to maximise profitability across its customer base, while the governance structure (and fiduciary duties) prevented Vodacom from compelling Maziv to sacrifice its own commercial interests. Nevertheless, the parties designed a comprehensive suite of remedies to address the competition authorities’ concerns.

Remedy Design

Designing effective remedies in complex mergers requires a delicate balance between preserving the transaction’s underlying rationale and efficiencies, while adequately addressing legitimate competitive concerns. The Tribunal rejected the initial remedy proposals — a comprehensive package of access obligations, pricing commitments, infrastructure development pledges, restrictions on information sharing and governance limitations on Vodacom — on the basis that they would require the Commission to function as a de facto sector regulator.

The Commission and the parties subsequently developed amended remedies that were similar behavioural remedies in substance but included strengthened enforcement mechanisms through a monitoring trustee. The revised remedies included further governance restrictions limiting Vodacom’s ability to influence Maziv’s strategic decisions, information barriers to prevent Vodacom from accessing commercially sensitive data about Maziv’s dealings with competing operators, and open-access non-discrimination commitments to ensure Maziv would maintain competitive neutrality in its wholesale operations, preventing preferential treatment of Vodacom. The Commission subsequently abandoned its opposition to the parties’ appeal.

Upon review, the Competition Appeal Court set aside the Tribunal’s prohibition, approving the merger subject to the revised conditions. In its assessment, the Court did not engage in a detailed reconsideration of the merits, but concluded that the revised conditions were sufficient to remedy the identified harms.9 It held that consumer welfare considerations for vulnerable communities cannot be confined to the enumerated public interest grounds under section 12A(3) of the Competition Act but must instead inform a constitutionally grounded competition assessment.10 Conditions requiring fibre rollout to 1 million homes in lower-income areas, free connectivity for schools and clinics, and a substantial Enterprise and Supplier Development Fund were accordingly treated as directly relevant to the competition analysis, reflecting an evolution in how merger control balances competitive and public interest objectives.

Key Takeaways From Vodacom/Maziv

The Vodacom/Maziv transaction offers important lessons for practitioners navigating minority stake transactions. It underscores the importance of accurately characterising the structure of the proposed transaction and its competitive implications. Mischaracterisation can trigger flawed theories of harm and obscure genuine competitive concerns. It is therefore important to invest effort in clearly articulating transaction structure, governance arrangements and operational relationships.

When structuring transactions, practitioners should anticipate and proactively address potential competition concerns. This may require a pre-emptive strategy to gather evidence on market structure and business strategies, and to conduct economic analysis early in the transaction timeline. In cases involving minority stakes, the economic assessment requires an analysis of the competitive effects of both financial interests and corporate control.

The Vodacom/Maziv transaction ultimately included specific conditions to mitigate the competitive concerns. These remedies demonstrate the importance of flexible, targeted approaches to addressing regulatory concerns. Indeed, well-crafted remedies often determine whether complex transactions proceed. It is therefore important to anticipate regulatory risks and to design tailored and enforceable remedies that address specific risks, while preserving the transaction value and rationale.

The Competition Appeal Court’s judgment carries important practical implications, especially for transactions in infrastructure-intensive sectors where investment, access and transformation considerations carry significant public interest weight. It is important to articulate clearly how proposed conditions contribute to broader developmental objectives, supported by credible commitments and verifiable metrics — not as an afterthought, but as an integral part of the competition assessment.

Footnotes:

1: Competition Commission (2025). Draft Guidelines on minority shareholder protections in terms of the Competition Act No.89 of 1998 (as amended). December 2025, para 1.2, p.4.

2: See, for instance, the European Commission Delivery Hero/Glovo decision, 2 June 2025, Case No. AT.40795.

3: Competition Commission (2025). Draft Guidelines on minority shareholder protections in terms of the Competition Act No.89 of 1998 (as amended). December 2025, p.23.

4: Competition Commission (2025). Draft Guidelines on minority shareholder protections in terms of the Competition Act No.89 of 1998 (as amended). December 2025, p.17.

5: In extreme circumstances, partial ownership can even be more harmful to competition than a full merger because it can soften competitive incentives without delivering the countervailing efficiencies that typically accompany full integration. See Salop, S.C., and O’Brien, D.P. (2000) Competitive Effects of Partial Ownership: Financial Interest and Corporate Control, Antitrust Law Journal, Vol. 67, p.562.

6: Salop, S.C., and O’Brien, D.P. (2000) Competitive Effects of Partial Ownership: Financial Interest and Corporate Control, Antitrust Law Journal, Vol. 67, p.568.

7: The transaction initially involved Vodacom acquiring a 30% stake with an option to increase ownership to 40%, though this ceiling was subsequently reduced to 34.95% as part of the merger conditions.

8: An ability analysis examines whether the merged entity would possess the capacity to implement foreclosure strategies. An incentive analysis assesses whether foreclosure would prove profitable, considering both direct costs and potential benefits. An effects analysis evaluates whether any foreclosure strategy would materially harm competition.

9: Competition Appeal Court Judgment. Case No: 260/CAC/Nov2024, para 55-57, p.24.

10: Competition Appeal Court Judgment. Case No: 260/CAC/Nov2024, para 68-70, p.23.

Related Insights

Related Information

Datum

08. Apr 2026