Current Power Trends and Implications for the Data Center Industry

-

14. Jun 2024

Herunterladen Download Article

Download Article

-

As the data center (“DC”) industry grapples with transformation and unprecedented growth, most recently driven by the deployment of generative artificial intelligence (“AI”) at scale, it stands at an important inflection point. Given a rapid convergence of trends across the digital infrastructure, technology and energy sectors, the DC industry is rapidly evolving to secure remaining power in a constrained market to build the new, massive facilities needed to house AI workloads. Utility and independent power producers (“IPPs”) are uniquely positioned to partner with the DC industry to accelerate the development cycle and capitalize on the outsized sector growth. In this article, FTI Consulting’s experts discuss current market trends and offer perspectives on the implications for the DC and power industries.

DC Load Growth, a Shock to Utility and Grid

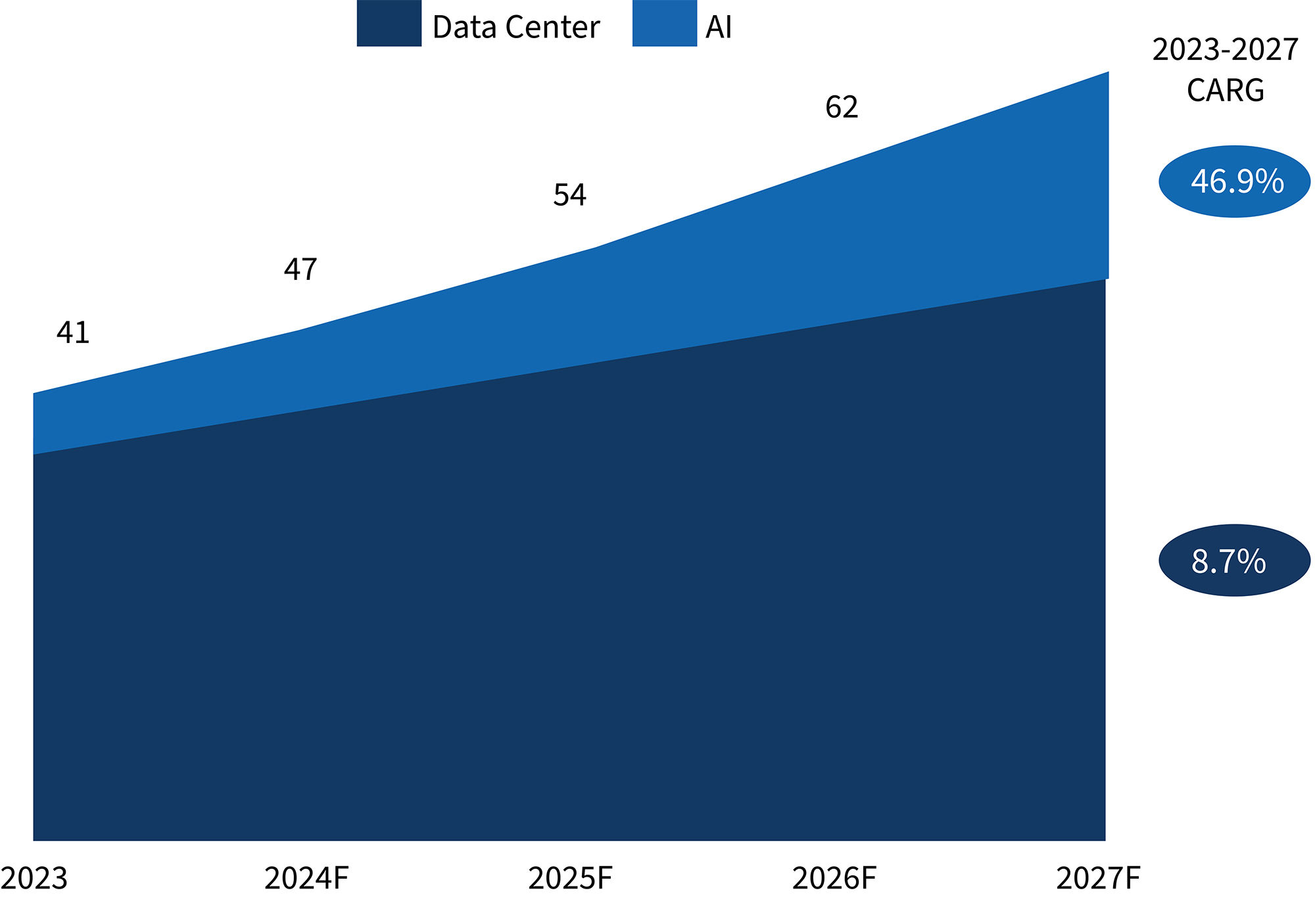

AI has taken the world by storm, and the demand for data centers to perform training, edge computing, inference and storage has skyrocketed. FTI Consulting projects global DC power demand to reach 71 gigawatts (“GW”) by 2027, with AI-related data center demand surging at a compound annual growth rate (“CAGR”) of 47.9%, far outpacing non-AI data center demand.

Large DC load interconnections are overwhelming utility and grid capacity, with no immediate relief in sight. FTI Consulting anticipates U.S. DC energy demand to almost double by 2027 from current levels of approximately 17 GW. The growth in DC demand, combined with the accelerating shift in broader electrification and energy transition, has profoundly disrupted traditional utility resource planning and cast a glaring spotlight on the constraints of the existing grid infrastructure.

Figure 1: FTI’s Global DC Power Demand Projection (in GW)

Historically, operators of data centers have gravitated towards metropolitan areas with robust connectivity. The preeminent data center market worldwide, Northern Virginia, is a prime example. Individual data center demand has grown from 30 MW to 60-90 MW, and large data center campuses have interconnection requests ranging from 300 MW to several GWs.1 This growth has led to a corresponding and significant increase in power demand, with summer peak load in the PJM Dominion Zone forecast to grow from 22 GW in 2023 to 34 GW by 2030.2 Currently, data centers in Northern Virginia have experienced multiyear delays and are only expected to see relief in 2026 when Dominion Energy completes new transmission projects in the region.

In parallel with the surging power demand from data centers to support the AI transformation, over 83 GW of baseload power resources are slated for retirement within the next decade. This impending loss of supply, driven by cost inefficiency or carbon intensity concerns, exacerbates an already strained energy equation.

To build a resilient backbone that can support the AI revolution, the DC and power industries must collaborate to forge new solutions in providing power to DC development and expand into new markets. One promising potential strategy: repurposing of legacy sites by exploring a different operating paradigm, one that unlocks synergies from the existing grid and fiber interconnections of the retiring assets to meet the growing energy demands of the AI revolution.

Backlog of Power Generation Resources Is Constraining New Data Center Supply

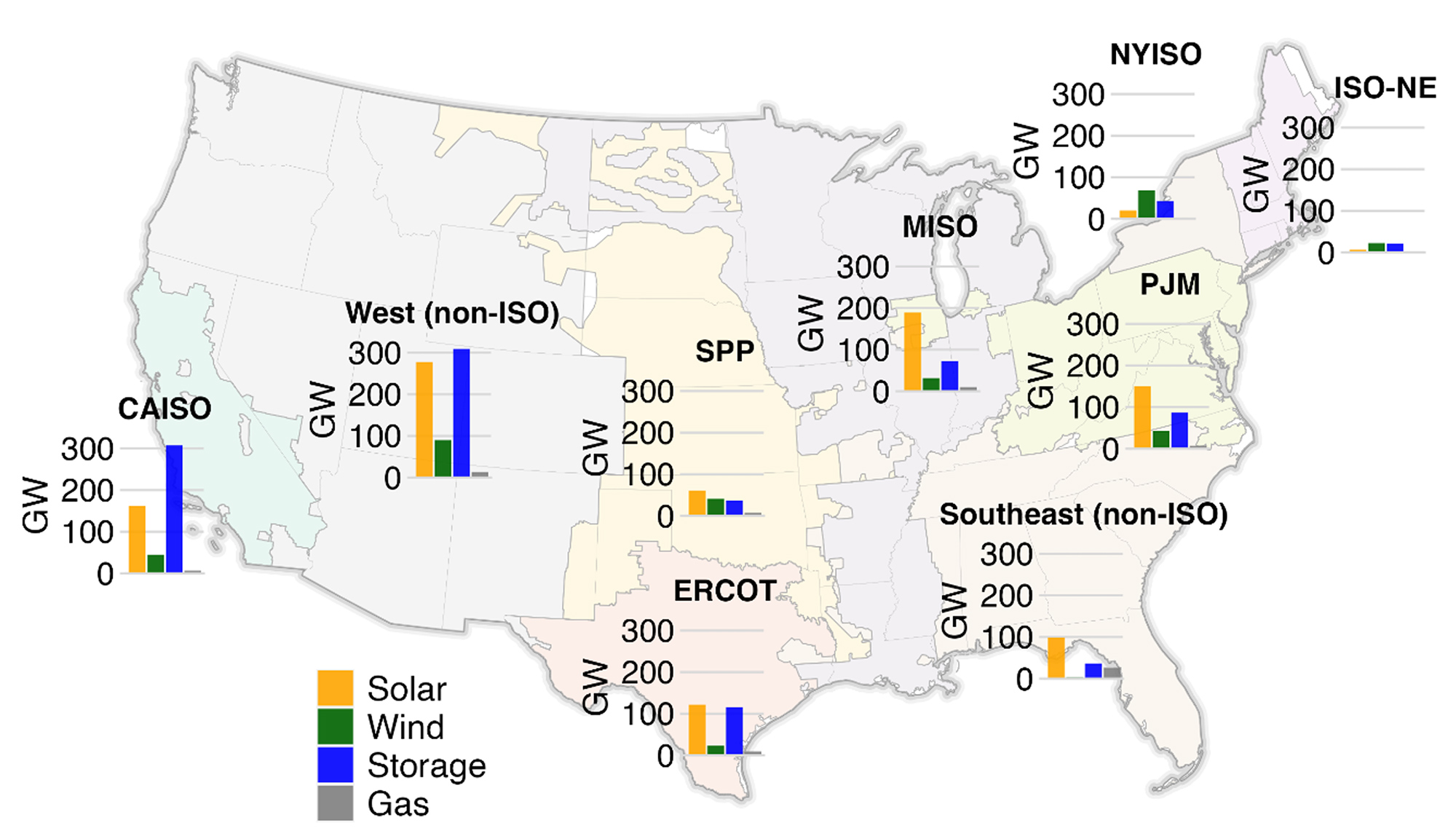

In many markets, power constraints are persistent owing to rapid load increase, resource retirements, and congested grid and interconnection. Federal Energy Regulatory Commission (“FERC”) Order No. 2023 mandated significant reforms to generator interconnection procedures to address development backlogs and improve certainty for projects seeking connection to the transmission system. These reforms are a significant step forward for more than 12,000 active projects currently seeking grid interconnection, totaling 1,570 GW of generator capacity and 1,030 GW of storage.3

Figure 2: Active Projects Seeking Grid Interconnection4

Despite the urgency of DC power needs, the development of new generation projects has faced significant challenges, leading to low completion rates and protracted development timelines. On average, the duration from submitting an interconnection request to achieving commercial operation has approached five years.5 Furthermore, less than 20% of power projects requesting interconnection from 2000 to 2018 were able to reach commercial operations by the end of 2023.6

Most of the project withdrawals occur during the early feasibility or system impact study phases, often due to high interconnection costs that could account for 20%-40% of the total project costs for solar projects. In comparison, completed projects typically have interconnection costs of only 5%-10% of the total costs. High network upgrade costs can materially impact the economic viability of a proposed new generation resource, leading to withdrawals. Other common reasons for project cancellations include issues with site control, right-of-way, permitting, offtake agreements, financing, or community opposition.

Bottlenecks in Electric Grid Infrastructure Are Impacting DC Markets

The lack of transmission and distribution (“T&D”) capacity to connect new DC loads has exacerbated bottlenecks and prolonged the development cycle. Utility and grid connection processes and timelines differ, but in many cases, delays in large load interconnection are driven by infrastructure constraints. Planning and construction of new transmission lines can take five to ten years, depending on various regionalized and localized factors including regulatory approval, permitting and right-of- way acquisitions. Utility processes also add to delays. In California, PG&E has stated that if new substation work is required to increase large load interconnection capacity, the large load interconnection process may take more than five years. This is similar to the situation faced by data centers in Northern Virginia, which experienced multiyear delays due to insufficient transmission capacity. However, relief is anticipated in 2026 when Dominion Energy completes a number of new transmission projects in the region.

Many utilities and IPPs find themselves at the center of the AI transformation and, as part of their growth strategy, have made commitments to support DC load. Some utilities are receiving interconnection requests that more than double their existing peak loads. The paradigm shift requires a proactive and innovative approach to resource planning, transmission and distribution infrastructure development, and customer engagement. Utilities are currently revisiting their capital expenditure plans to ensure they can meet increasing demand for electricity and modernize the electrical grid. This will likely take several years to adequately address — but DC providers need power today.

DC Expansion into New Markets

The rapid growth in data centers has attracted new capital to build data center facilities that are purpose-built for AI workloads. With power constraints limiting expansion capacity in primary markets, the DC industry is actively scouting new locations outside of traditional hubs and moving into secondary or even tertiary markets. As investors evaluate opportunities to develop data centers in these previously untapped regions, they must carefully consider a variety of factors.

Among new market considerations, several stand out to build future-proof data centers: the availability of high- quality power supply, sufficient interconnection capacity, fiber connectivity, latency, robust revenue outlook, competitive cost of energy, permitting risks, and community support and incentives. The Midwest, Southeast, Texas and several other areas have emerged as sought-after markets, as DC developers evaluate sites in these regions for their next-generation DC facilities.

Managing Cost of Energy in a Volatile Market

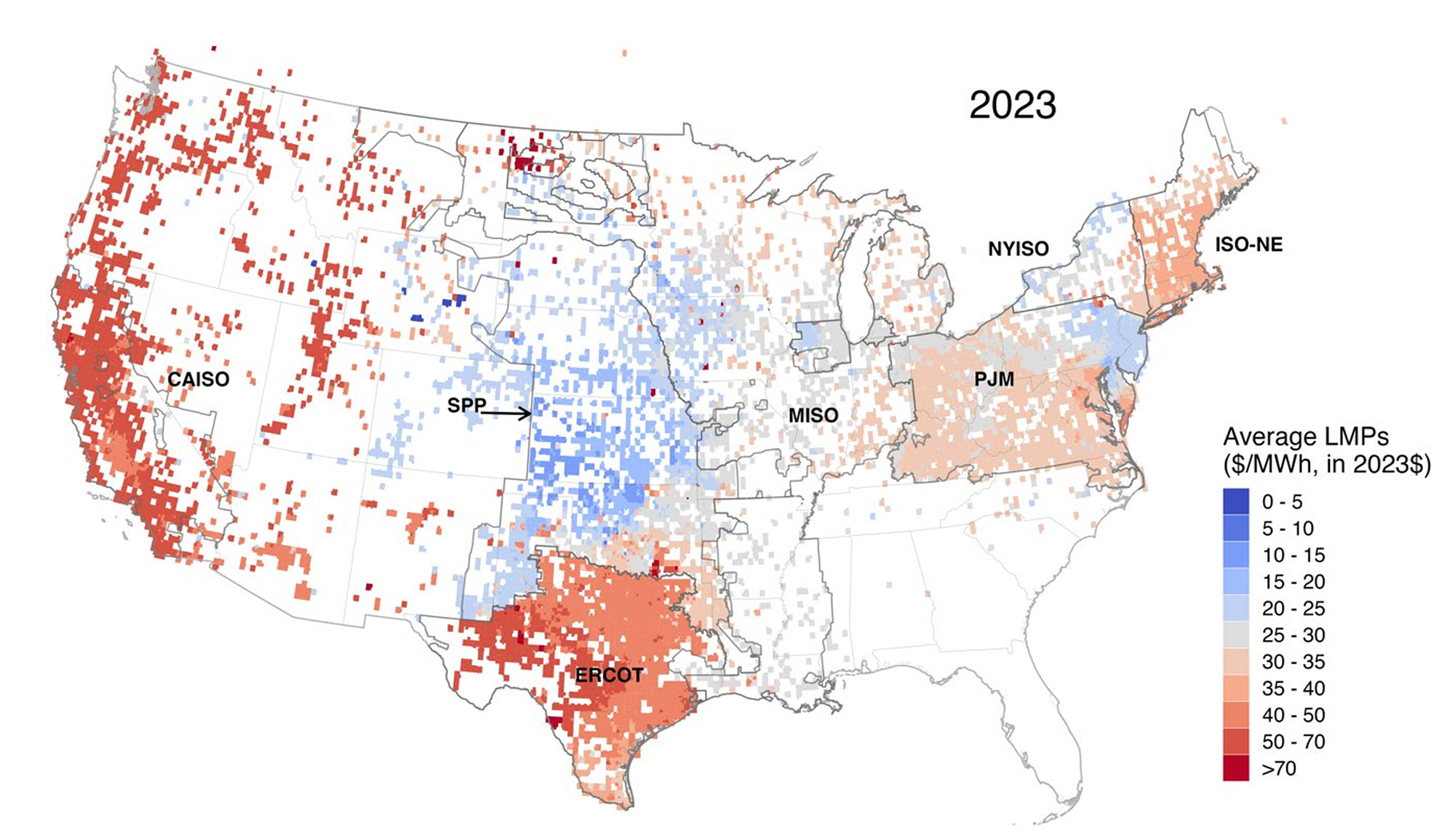

Energy prices are a crucial factor in lowering the total cost of DC ownership and have been top of mind when determining where to locate new DC development. Regional disparity in market design, transmission capacity, and supply and demand lead to varied average energy prices across locations, as shown in Figure 3.

Episodes of high or low prices typically occur as a result of transmission constraints (dislocation of load and resources), mismatch of load and generation profiles, fuel costs, or weather-driven variability of supply and demand. These factors lead to increased price volatilities and directly impact the bottom line of data centers. Some hyperscalers may have become less price sensitive to power due to the constraints, but for most data centers, the long-term competitive cost of energy, local and regional power market dynamics, and the regulatory environment are important considerations.

Figure 3: 2023 Average Locational Marginal Prices7

Data Centers Are Moving to the Power Generation Source (i.e., BTM Configurations)

Facing significant challenges to bring power to data centers, some data centers are adopting a new approach — bringing the data centers to the power generation source through behind-the-meter (“BTM”) configurations. In a BTM setup, the data center directly draws power from the generation facility located on the same site. A BTM data center can function independently from the utility for most of its power needs and rely on the utility as a “provider of last resort.”

This approach provides competitive advantages in terms of cost savings and speed to market. Talen Energy, for example, successfully implemented a BTM strategy on a large scale through its Cumulus data centers in Berwick, Pennsylvania. The data centers are directly connected to Talen’s 2.5 GW Susquehanna Steam Electric Station, a nuclear power plant, and receive power via a Power Purchase Agreement (“PPA”). In March 2024, Talen Energy sold Cumulus Data to Amazon Web Services (“AWS”); the transaction highlights the growing interest in BTM strategies.

The BTM model has also been adopted on a smaller scale in other locations. Many IPPs are actively evaluating sites with the potential to collocate data centers. Interest in existing nuclear generation resources is at an all-time high, and natural gas power plants have emerged as pivotal assets in providing the power lifeline to data centers, especially when paired with renewables, fuel cells and batteries, and supplemented with grid power to create an around-the- clock (“ATC”) solution, which is important for mission- critical data centers. In addition, the potential viability of collocating BTM data centers with efficient combined cycle gas turbines (“CCGTs”) in otherwise transmission- constrained locations provides a valuable optimization strategy for IPPs to enhance asset performance. While many DC BTM or microgrid implementations have been successful, it is essential to consider the unique challenges and circumstances associated with each project to ensure long-term viability.

Implementing on-site power generation capabilities can provide several key advantages by overcoming grid congestion, avoiding transmission losses and alleviating environmental impacts. When implemented through existing or new generation resources, a BTM alternative can often accelerate speed-to-market and reduce the impact of T&D outages. The DC value of lost load (“VOLL”) is estimated at a staggering $9,000 per minute, with 25% of the DC outages costing over $1 million.8, 9 Adopting BTM alternatives not only mitigates the risk of costly outages, but also offers a competitive advantage. The realizable T&D and utility savings, ranging from $7 to $12 per megawatt- hour (“MWh”), can further enhance profitability and operational efficiency.

Opportunities in Game-Changing Resources of the Future

Currently, solar, wind and battery storage accounts for over 95% of the proposed capacity additions in the U.S. market. Due to the lack of commercially available and cost-effective long-duration energy storage solutions, the industry has yet to crack the code on how to power the growing data centers sustainably and reliably around the clock on a large scale, except with existing nuclear generation resources and some fuel cell applications.

Data centers are becoming valuable partners in developing capital-intensive, long-term energy solutions. These potentially game-changing solutions include fuel cell, advanced geothermal, fusion, small modular nuclear reactors, hydrogen, and carbon capture, among others. Breakthroughs in long-duration storage, whether in the form of advanced batteries, flow batteries, compressed air, pumped storage, hydrogen, or other approaches, will be critical to enabling a renewable-powered digital economy. Just as tech companies have been a formidable force driving the development of wind and solar in the past decade, data centers are now front and center in enabling accelerated innovation across the value chain.

Conclusions

As the data center industry navigates through a period of high growth and intense competition, a holistic assessment of the market landscape will help build pivot strategies to navigate the increasingly complex development process and market uncertainty.

As data centers expand geographically to serve the growing demand for cloud computing and AI, investors must look beyond the basic requirements of power, land, water and fiber when evaluating the long-term viability of DC sites. Key factors include competitiveness, scalability and flexibility to adapt to constantly evolving computing needs and technology advancements. These considerations are critical to preserve and enhance the life-cycle value proposition of the assets in order to avoid becoming obsolete or stranded capacity. The utilities and IPPs are uniquely positioned to partner with data centers to de-bottleneck the development cycle. Establishing a “first mover” advantage is paramount in capitalizing on the current immense demand and projected growth in the data center space.

How FTI Consulting Can Help

FTI Consulting’s Power, Renewables & Energy Transition Practice (“PRET”) offers a team of highly experienced economists, industry specialists, former utility executives, regulators and accountants to serve the regulatory and strategic needs of our power and utility clients. For data centers, investor-owned utilities, municipalities, cooperatives, developers or regulators, the PRET team provides our clients with holistic and actionable strategies, pertinent analysis, and approaches to compete across the energy value chain.

FTI Consulting’s Data Center Practice is an industry leader offering an expansive suite of services to investors across the globe, including due diligence, M&A advisory, market assessments, strategy, merger integration & carve-out support, performance improvement, business transformation, and turnaround & restructuring. Our data center team has worked on dozens of recent North American M&A transactions, providing commercial, operational, technical, ESG & sustainability, Workplace Health Safety and Environmental (“WHSE”), financial, tax and cyber due diligence services with expertise across the colocation spectrum (retail, wholesale, hyperscale, edge, crypto mining, GPU cloud and carrier hotel segments).

Our services include:

- Growth Strategy

- Financial and Operational Strategy and Business Transformation

- Turnaround & Restructuring

- Utility Rate Case Advisory and Rate Design

- Capital Project Planning

- Regulated and Unregulated Asset M&A

- Power Market Price Forecasts

- Safety and Reliability Compliance

- Financial and Operational Compliance

- Dispute and Expert Witness

Footnotes:

1: “Q1 2024 Earnings Call,” Dominion Energy (May 2, 2024).

2: “2024 Load Forecast Report,” PJM (January 2024).

3: Joseph Rand, Nick Manderlink, Will Gorman, Ryan H. Wiser, Joachim Seel, Julie Mulvaney Kemp, Seongeun Jeong, and Fritz Kahrl,”Queued Up: 2024 Edition, Characteristics of Power Plants Seeking Transmission Interconnection As of the End of 2023,” Berkeley Lab (April 2024).

4: Ibid.

5: Ibid.

6: Ibid.

7: Dev Millstein, Eric O’Shaughnessy and Ryan Wiser, “Renewables and Wholesale Electricity Prices (ReWEP) Tool,” Lawrence Berkeley National Laboratory (May 2024).

8: “The High Cost of Downtime In 2023 Data Centers,” Prosource (2023).

9: “Annual Outage Analysis 2023,” Uptime Institute (2023).

Related Insights

Related Information

Datum

14. Jun 2024

Ansprechpartner

Ansprechpartner

Senior Managing Director

Global Practice Leader Power, Renewables & Energy Transition (PRET)

Senior Managing Director