Brazil 2026: Business Perception in an Electoral Year

Business Leaders’ Views on Political, Regulatory and Economic Issues in Brazil’s 2026 Election Year

-

2026年6月26日

下载 Download Report

Download Report

-

Public debate during Brazilian election cycles, especially in media and political discourse, is often framed through broad references to “public opinion,” “Faria Lima”1 or “market sentiment.” These labels try to fit mixed categories: mass attitudes vs. financial elites vs. abstract indicators mixed into a single narrative that obscures important distinctions among the audiences they seek to describe. In practice, different sectors, industries and types of firms — as well as varying levels of corporate decision-makers — perceive political and economic risks in materially different ways. As a result, aggregate claims about “what markets think” tend to flatten a far more heterogeneous set of concerns and expectations operating across the real economy.

Against the backdrop of Brazil’s 2026 electoral cycle — in which voters will elect not only a president but also 27 state governors, the full Chamber of Deputies, state legislative assemblies and roughly two-thirds of the Federal Senate — FTI Consulting’s Public Affairs team in Brazil conducted a targeted survey between February and March 2026 to capture real-time sentiment from business decision-makers operating locally and better understand how business leaders are assessing the country’s political, regulatory and economic environment during this pivotal electoral year.

This effort was undertaken amid an especially complex environment for business decision-making. Beyond the uncertainty traditionally associated with presidential and congressional elections in Brazil, companies are navigating a combination of domestic and international pressures, including debates over fiscal sustainability and tax reform, volatility in commodity markets and export demand, and heightened exposure to global trade tensions reshaping investment and supply-chain dynamics across the world.

The results presented in this analysis are based on a targeted perception survey conducted with companies operating in key sectors of the Brazilian economy, particularly Agriculture and Livestock, Consumer Goods, and Financial Services. The sample is composed primarily of large enterprises, with significant presence across the national territory and direct exposure to the country’s regulatory and political environment. Participants rated their level of concern across 11 policy and business-related themes.2 The survey was designed as a perception-based assessment, offering directional insights from select decision-makers rather than a statistically representative view of Brazil’s business community as a whole. As such, it provides a structured snapshot of how segments of Brazil’s business community are assessing risks, prioritizing challenges and interpreting the policy environment ahead of the October 2026 elections.

Key Insights From Business Perceptions

Economic Anxiety Extends Beyond Domestic Politics

Although economic policy emerged as the main concern among respondents, the factors shaping these perceptions appear to extend beyond domestic political dynamics alone. Key sources of business uncertainty — including inflation, exchange-rate volatility, commodity prices and investment conditions — are also influenced by external developments such as geopolitical tensions, trade disputes and global market fluctuations. The findings suggest that business perceptions of the 2026 elections are embedded in a broader environment of international economic uncertainty.

Business Concern Is Concentrated at the Macro Level

The survey suggests that concern is concentrated less around sector-specific regulation and more around broader macroeconomic and institutional conditions that shape the overall operating environment. Respondents consistently prioritized inflation, interest rates, exchange-rate volatility, regulatory predictability and institutional stability — factors that firms have limited capacity to anticipate and/or influence directly. By contrast, more sector-specific regulatory themes generated comparatively lower concern, possibly reflecting a greater perceived ability to influence and/or adapt at the operational level.

Electoral Outcomes Are Not Seen as a Complete Fix

The survey also suggests skepticism about the extent to which this year’s electoral outcomes can resolve structural instability on their own. While respondents expressed elevated concern about economic and institutional conditions, many also adopted neutral to cautious expectations regarding the post-election outlook. This indicates a perception that regulatory unpredictability, political polarization, institutional fragmentation and policy discontinuity are not temporary electoral anomalies, but structural features of Brazil’s governance environment likely to persist beyond a single administration.

The “Brazil Cost” Remains Central

Several of the concerns identified by respondents — including taxation, regulatory complexity, labor regulation and legal uncertainty — converge around longstanding structural challenges associated with the “Brazil Cost” (extra costs and operational friction that companies face when doing business in the country — costs that would not exist, or would be much lower, in most other markets). In this context, the recently approved tax reform appears to occupy an ambiguous place in business perceptions: While broadly seen as a potentially positive step toward simplifying the tax system over the medium and long term, its gradual implementation also introduces a short- to medium-term uncertainty that will require constant regulatory adaptation and legislative coordination.

Political Risk Is Still Focused on the Presidential Role

The survey suggests a disconnect between the issues respondents identify as most concerning and the political arenas most responsible for shaping them. Although participants consistently highlighted taxation, fiscal policy, regulatory stability, labor regulation and institutional coordination, qualitative responses remained heavily centered on the presidential election result itself, with comparatively limited attention to congressional, gubernatorial or broader legislative dynamics. This indicates that business perceptions of political risk may still be filtered through a predominantly presidential lens, heightened by current political polarization, even when most of the relevant policy areas depend on legislative negotiation, budgetary control and executive-legislative coordination.

Beyond the Election: Structural Risks and Strategic Priorities

Overall, the survey captures the perspectives of a focused group of business leaders, primarily from large enterprises with substantial operational presence in Brazil. As major employers, capital allocators and participants in policy and regulatory discussions, these organizations shape investment trends, business confidence and broader perceptions of Brazil’s economic and institutional environment. Their responses provide a relevant snapshot of how economically significant actors are interpreting the risks and uncertainties of the 2026 electoral cycle.

The findings suggest that business concerns ahead of the elections are less about isolated policy proposals or electoral preferences and more about broader questions of economic management, institutional stability, regulatory predictability and governance capacity. This perception emerges within an already complex environment: Beyond domestic political and economic uncertainty, respondents are navigating heightened exposure to global trade tensions reshaping investment flows, supply chains and macroeconomic conditions. Many respondents view the principal challenges facing Brazil’s business environment as structural, extending beyond the outcome of a single electoral cycle.

In increasingly complex and polarized political contexts, understanding how different segments of the business community interpret risk and policy direction is essential for strategic decision-making. Effective navigation requires not only monitoring political developments, but also engaging stakeholders through coordinated strategies that advance institutional objectives, protect reputation and strengthen long-term license to operate amid evolving regulatory and political conditions.

Respondent Profile and Concerns Overview

This section offers a descriptive overview of the participants’ profile, the sectors represented, geographic distribution and the levels of concerns identified among the policy- and business-related themes presented in the survey, providing the necessary context to interpret the findings previously presented.

Respondent Profile

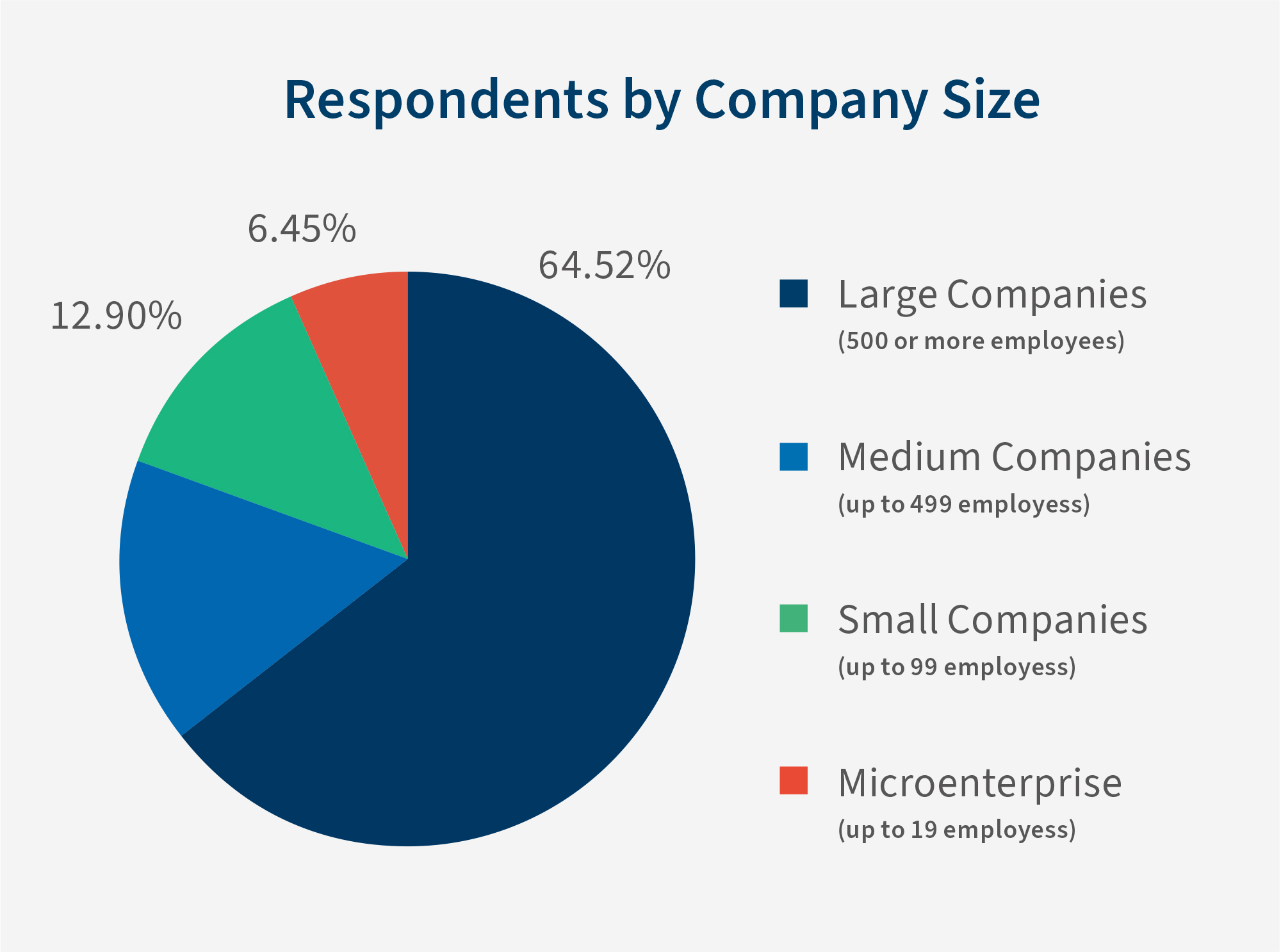

The survey captured responses from 31 companies between February and March 2026, with participation concentrated among larger enterprises. Companies3 with more than 500 employees represent 64.52% of respondents, while medium-sized companies account for 16.13%. Small businesses comprise 12.90% of the sample, and microenterprises represent 6.45%. As a result, the perspectives reflected throughout this report are weighted toward organizations with significant employment bases, capital allocation capacity and exposure to Brazil’s regulatory and political environment.

FTI Consulting Brazil, 2026

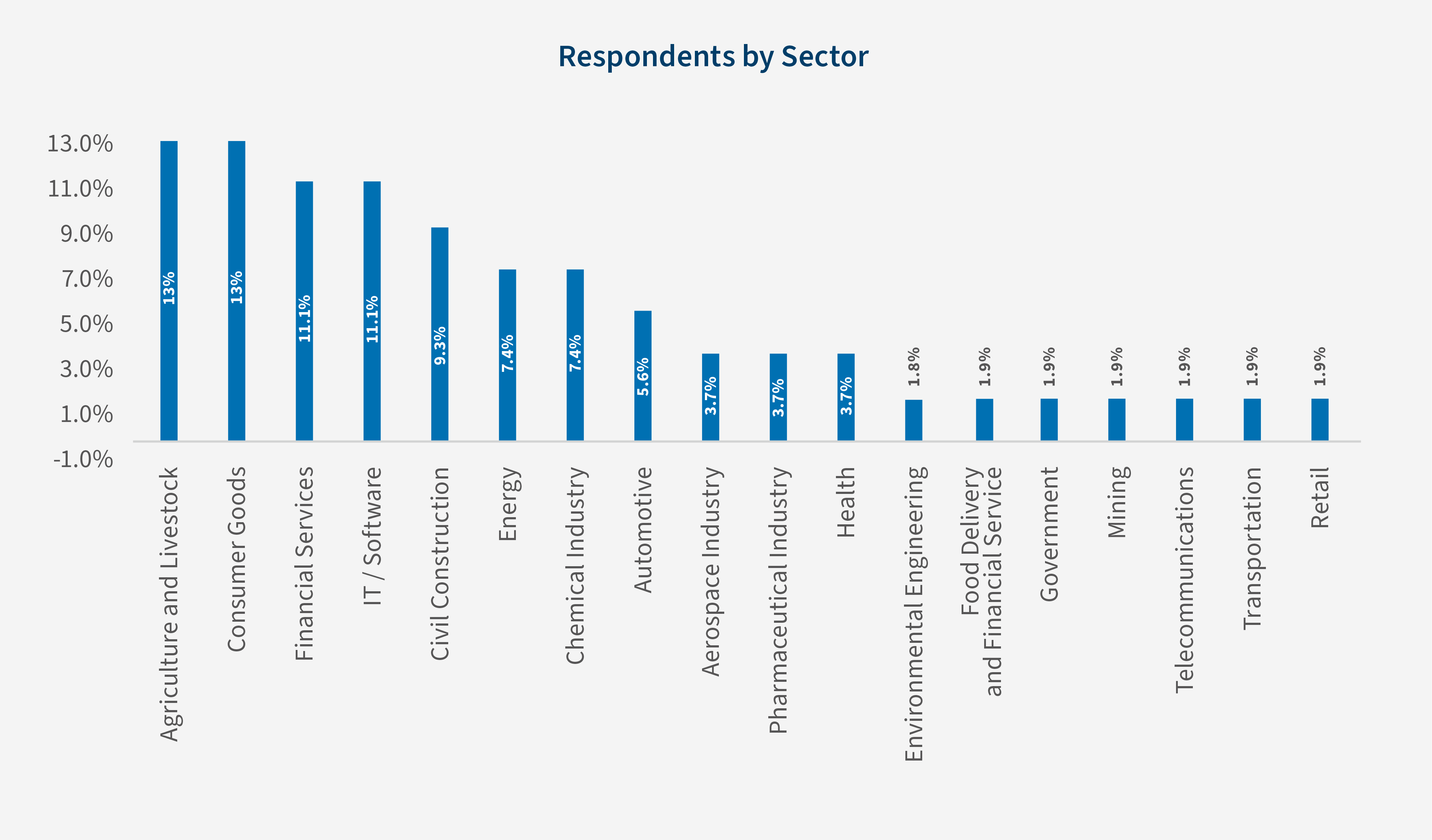

The participating companies operate across 19 distinct economic sectors, generating a total of 54 sector representations (respondents were able to identify more than one area of activity). Agriculture and Livestock, Consumer Goods, Financial Services, and Information Technology Services emerged as the most frequently represented sectors, each accounting from 11% to 13% of total responses. Other areas represented in the responses include Aerospace, Automotive, Chemical Industry, Civil Construction, Energy, Food and Beverage, Health, Mining, Pharmaceuticals, Retail, Telecommunications and Transportation. This reflects a diversified cross-section of companies operating within Brazil’s broader economic landscape.

FTI Consulting Brazil, 2026

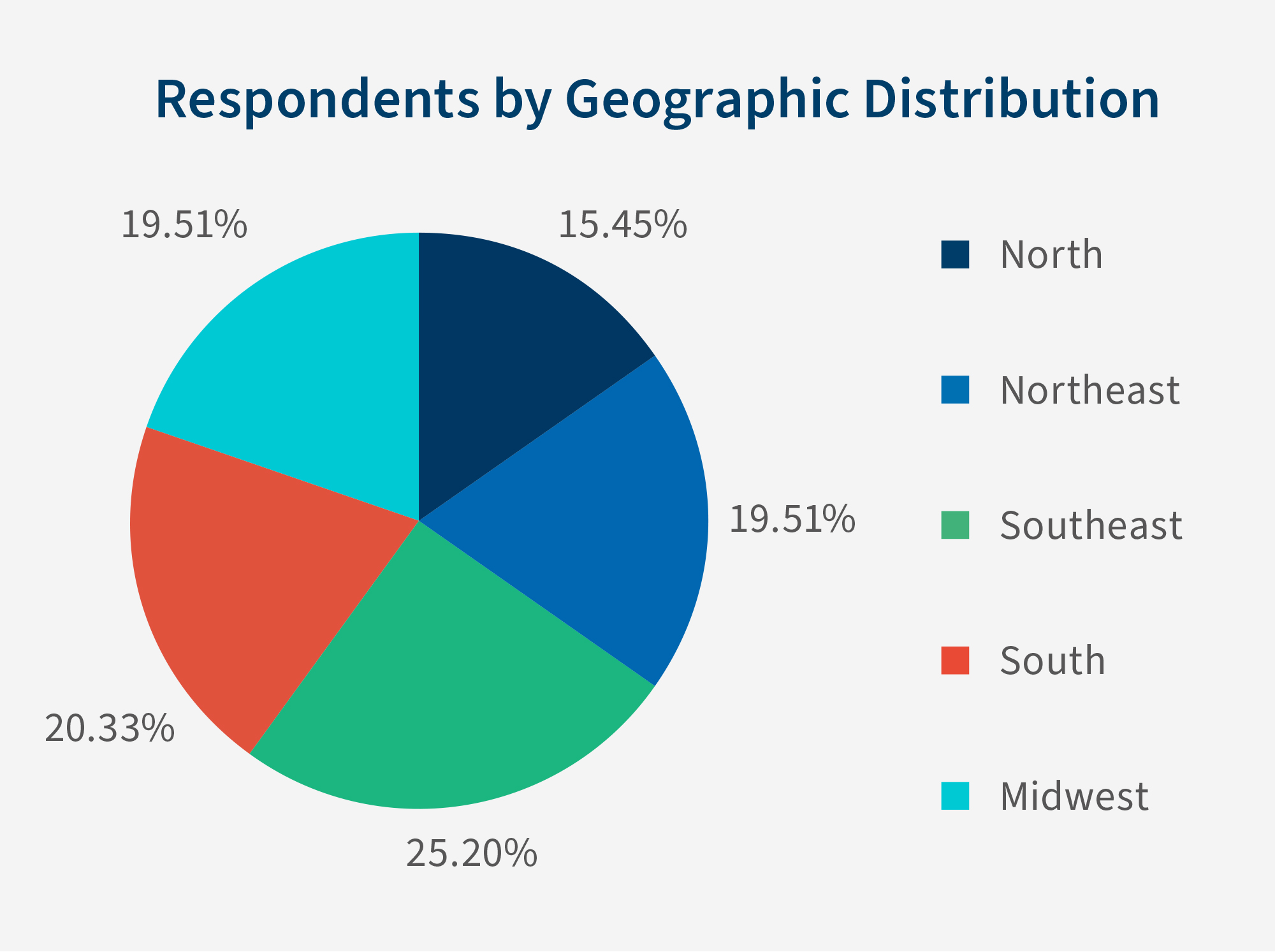

Geographic concentration of companies’ headquarters is heavily skewed toward Brazil’s economic center. The Southeast region dominates with 90.3% of respondents, while the Midwest represents only 3.2% and foreign-based operations account for 6.5%. However, in terms of local presence, respondents represent a well-balanced presence in Brazil’s territory — 25.20% Southeast, 20.33% South, 19.51% both for Northeast and Midwest and 15.45% North.

FTI Consulting Brazil, 2026

This concentration of headquarters presence reflects the continued centrality of the Southeast — particularly São Paulo, Rio de Janeiro and Minas Gerais, which together account for approximately 55% of Brazil’s GDP4 — within the country’s corporate and industrial landscape. At the same time, many of the companies represented in the survey maintain operations across multiple regions of Brazil, providing broader exposure to the country’s national business environment beyond the location of their headquarters.

Overall, the survey reflects the perspectives of a selected group of business leaders, primarily from large enterprises with substantial operational presence across Brazil. The respondent base spans a wide range of sectors and includes companies with nationwide activities, providing a directional view of how key segments of the private sector are assessing the current environment.

Perceptions and Priority Concerns

Survey respondents reported a relatively high level of concern regarding the potential impacts of the 2026 elections on Brazil’s business environment. On a scale from 1 to 5, the average concern level reached 3.87 — above the midpoint and closer to the upper end of the scale — indicating that participants broadly view the upcoming electoral cycle as a significant factor shaping the operating environment for business planning and decision-making in the coming years. This level of concern suggests the 2026 cycle is perceived as more consequential than typical election periods, reflecting heightened sensitivity to political and macroeconomic uncertainty.

When asked about the potential impact of the elections on company performance over the following two years, respondents expressed predominantly cautious expectations. Neutral assessments accounted for the largest share of responses, suggesting that many view the ultimate business impact as contingent on the political and economic direction that will emerge after the vote. At the same time, negative expectations outweighed positive ones, pointing to a general bias toward caution regarding the post-election economic, regulatory and institutional environment. In practice, this caution may translate into more conservative investment, hiring and expansion plans through 2027, with firms prioritizing liquidity buffers, scenario planning and risk mitigation over aggressive growth strategies.

Among the issues covered in the survey, economic policy — particularly inflation, interest rates and exchange rate volatility — emerged as the most salient area of concern, concentrating the highest share of “most concerning” and “very concerning” responses. The prominence of these macroeconomic issues signals that economic stability, not just fiscal reform or tax policy, will be central to business confidence regardless of the election outcome. Legal certainty and regulatory stability, taxation and tax reform, and political and institutional instability formed a second tier of concerns, also attracting consistently elevated levels of attention.

These findings suggest that the next administration (as well as the current one) will face significant pressure to deliver on fiscal sustainability, regulatory predictability and institutional stability. Labor regulation and industrial policy were likewise identified as relevant, though with more varied levels of concern across respondents. By contrast, environmental policy, technology regulation, geopolitical tensions and trade tariffs generated more moderate and dispersed responses. While these issues remain important for specific segments, they were generally perceived as less pressing than domestic economic and institutional factors.

Importantly, while aggregate concern is high, the survey also reveals variation in how different sectors and firm types prioritize risks. This underscores that “what the market thinks” is not a single stance but a set of overlapping, sometimes divergent, assessments across Brazil’s heterogeneous business landscape. The extent to which the incoming administration addresses fiscal sustainability, tax reform and regulatory predictability will likely determine whether current caution gives way to greater confidence in 2027.

Footnotes:

1: Brazil’s Wall Street.

2: 11 policy and business-related themes present in the survey: Tax and Tax Reform (Carga tributária e reforma tributária); Labor Regulation (Regulação trabalhista (CLT, escala 6x1, etc.)); Economic Policy (Política econômica (inflação, juros, câmbio)); Law Security and Regulatory Stability (Segurança jurídica e estabilidade regulatória); Industrial Policy and Sector Incentives (Política industrial e incentivos setoriais); Environment and Climate Policy (Política ambiental e climática); Corruption and State Governance (Corrupção e governança pública); Political and Institutional Instability (Instabilidade política e institucional); Geopolitical Tensions and Sanctions (Tensões geopolíticas e sanções); Trade Tariffs (Tarifas Comerciais); Tecnology Regulation (Regulação de atividades de tecnologia (big techs, IA, etc.)); and Other (Outros).

3: FTI Consulting utilized Brazilian’s Institute of Geography and Statistics (IBGE’s) category that classifies the size of companies by the number of its employees. For further statistics on Brazilian companies’ demography, see: https://www.ibge.gov.br/estatisticas/economicas/servicos/22649-demografia-das-empresas-e-estatisticas-de-empreendedorismo.html.

4: Brazilian’s Institute of Geography and Statistics (IBGE), Gross Domestic Product (GDP) / Produto Interno Bruto – PIB (2025).

相关服务

相关信息

发布于

2026年6月26日