Early Signals, Safer Returns: Fraud Detection in Private Credit

Private Credit: Second of a Series

-

March 13, 2026

-

The boom in the private credit market has enabled institutional investors to chase higher returns. While speed and innovation can drive attractive returns, rapid expansion often outpaces governance, creating structural blind spots that fraudsters can exploit. When detection lags, manageable exposures can escalate into material losses, threatening returns and investor confidence.

In a previous article, we outlined why a risk-based approach is essential to manage financial and regulatory exposure in this expanding asset class. When creditors and debtors face difficulties, allegations of fraud start to spread, which could harm the entire industry if proven true.

Opacity and immature controls can conceal weak fundamentals, even from sophisticated investors. Private credit losses can stem from any number of mistakes or intentional misdirection, despite creditors’ presumed oversight, field exams, and review processes.

Much like a car’s “check engine” light, early warning signs aren’t necessarily catastrophic. They simply indicate something that requires attention. It could be something minor, like a loose gas cap or a faulty spark plug. Worth investigating, of course. Ignoring these signals risks escalation.

How can creditors and debtors spot early indicators of potential fraud and identify patterns requiring deeper scrutiny? In this article, we will focus on how private creditors can accelerate fraud detection and strengthen investigative rigor to prevent financial and reputational damage.

Fraud Risks Grow Where Oversight Lags

The fraud schemes alleged in private markets are like those in traditional markets and contain the same attributes of the fraud triangle – incentive, opportunity, and rationalization. One of the core challenges here is that fraudsters have home-field advantage. Familiar lender controls, evolving governance, numerous creditors with available/deployable capital, and the rapid pace of deal execution create conditions where fraudsters can operate before warning signals are fully visible.

While creditor diligence and vetting of debtor fund structure and capital sources can serve as a baseline for trust, they cannot anticipate future misrepresentation or operational failures.

Diligence frameworks identify opportunities for fraud but often miss incentives or justifications hidden within operations. Understanding how both elements interact is key to early fraud detection.

Early Warning Signs of Fraud

In high-growth environments, risk concentrates in two places: the data and models that inform credit decision and the debtor-creditor interactions and communications. Fraud can originate from either side but often conceals itself in the grey space between data, incentives and human behavior. When transaction velocity outpaces diligence and performance pressure mounts, models strain – this is where fraud thrives.

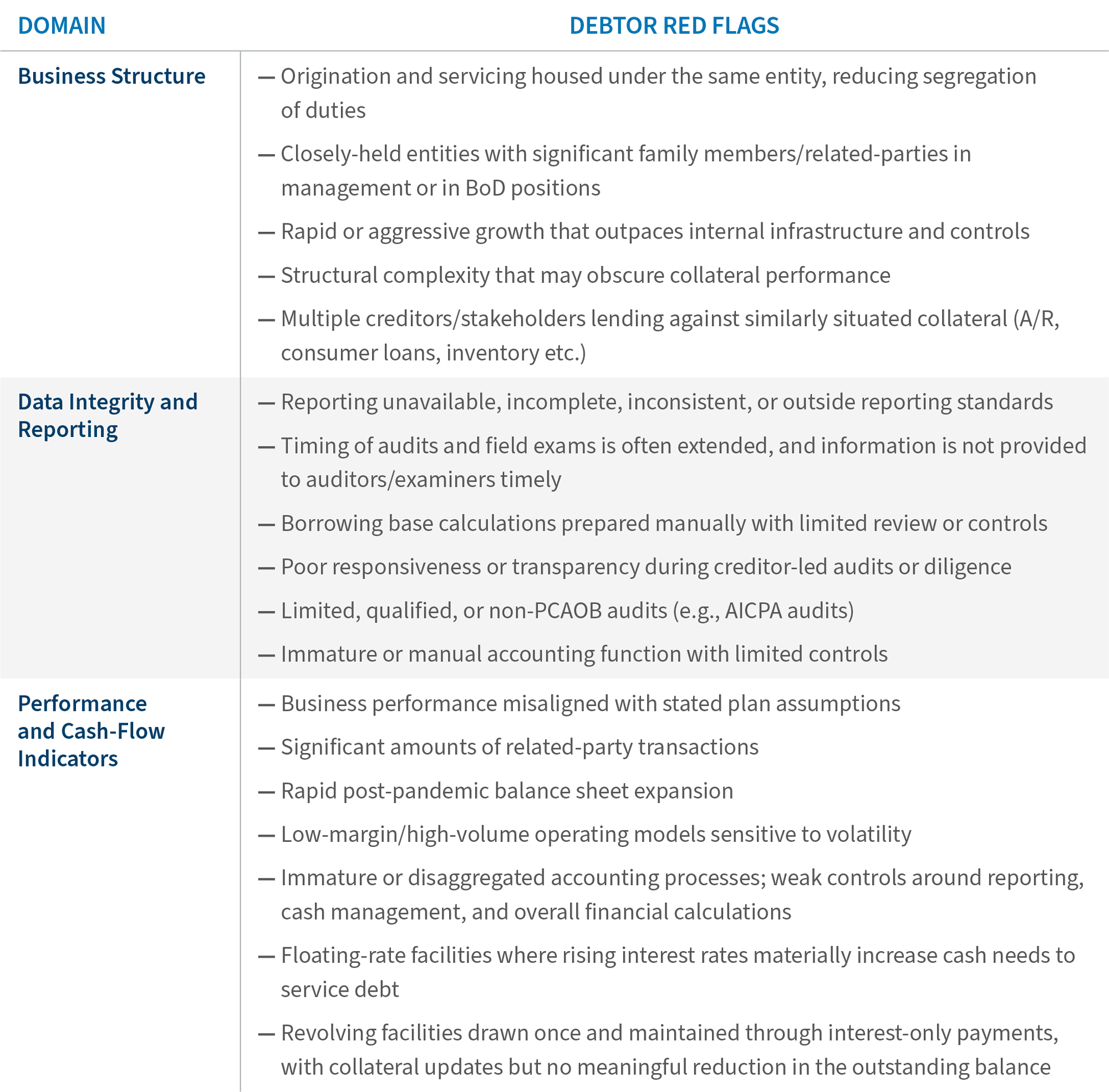

Debtor-side fraud signals often stem from operational strain, governance immaturity or intentional concealment of information (e.g., performance and assets). While these signals don’t imply wrongdoing, they are the “check engine” signal that must be addressed.

Below are early borrower-related fraud signals that may require closer scrutiny by lenders:

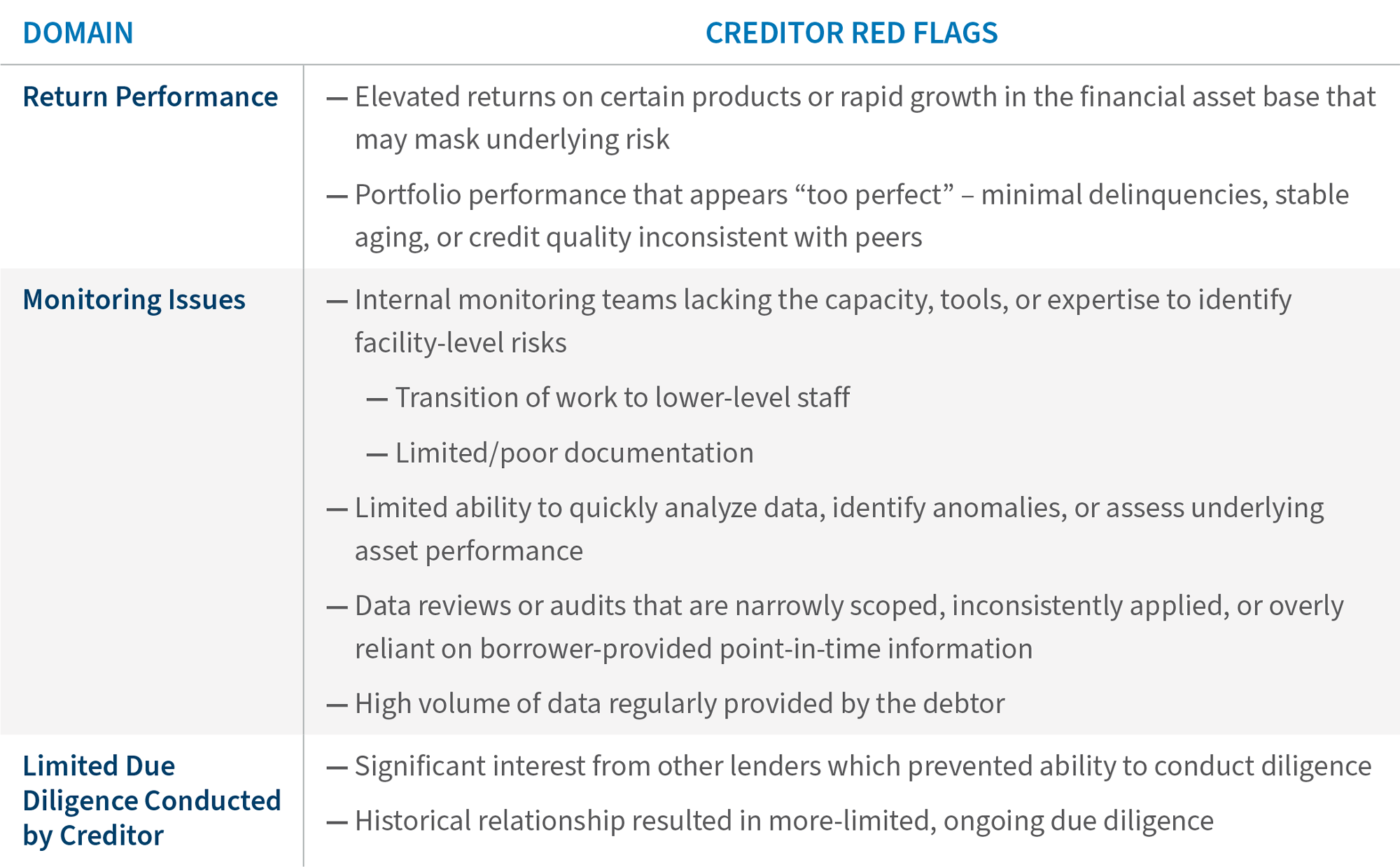

When initial diligence overlooks key factors or a loan underperforms, fraud opportunities can emerge on the creditor's side.

Below are red flags for creditors that may indicate elevated fraud risk at debtors and require further investigation.

Proactively identifying and addressing creditor-side signals ensures that diligence is not just a static checklist, but a continuous tool to safeguard investments.

From Red Flags to Resilient Returns

Rapid growth in private credit magnifies both opportunity and hidden risk. Investors who combine rigorous diligence with proactive pattern recognition are better positioned to surface early warning signals, protect returns, and sustain market confidence. With a firm understanding of red flags and how they reveal themselves, both lenders and debtors can sleep more easily.

Related Insights

Published

March 13, 2026