Public Country-by-Country Reporting

A New Era of Tax Transparency for Multinational Groups Requiring Immediate Action

-

June 22, 2026

Downloads Download Article

Download Article

-

Global tax transparency continues to evolve rapidly, with governments placing increasing emphasis on public accountability and visibility into multinational tax practices. One of the most significant developments in recent years is the introduction of Public Country-by-Country Reporting (“Public CbCR”), a regime requiring certain multinational enterprise (“MNE”) groups to publicly disclose key financial and tax information across jurisdictions.

Public CbCR has been discussed globally for several years following the adoption of the EU Public CbCR Directive and subsequent developments in Moldova and Australia.1, 2, 3 However, the regime is now becoming immediately relevant for many MNE groups as the first reporting periods have already commenced in several jurisdictions. For many MNE groups with a December year-end, FY 2025 may represent the first year for which Public CbCR disclosures will be required, with public filings expected from 2026 onward. As a result, organizations should now move beyond awareness and begin assessing applicability, data readiness, governance framework and potential reputational considerations arising from public disclosure of tax and financial information.

What is Public CbCr?

Public CbCR requires large MNE groups to publicly disclose selected financial and tax information on a country-by-country basis. The regime builds on the traditional CbCR framework first introduced by the Organisation for Economic Co-operation and Development (“OECD”) as part of Action 13 of the OECD/ G20 Base Erosion and Profit Shifting (“BEPS”) Project, under which MNEs report jurisdictional tax and financial information to tax authorities. Public CbCR regimes, extended this framework by requiring similar information, is broadly derived from but not identical to the OECD CbCR framework, to be publicly disclosed, through government registries or official company websites.

Why Was Public CbCR Introduced?

MNE groups have come under increasing scrutiny from regulators, investors and the public primarily due to concerns regarding BEPS, where profits are reported in jurisdictions with lower tax rates rather than where substantive economic activities occur. This has created a perceived misalignment between profit generation and tax payments. As a result, stakeholders are demanding greater transparency to assess whether multinational groups are paying their “fair share” of tax, which has driven the introduction of enhanced reporting frameworks. In response, Public CbCR has been introduced to provide greater visibility into the tax and economic activities of MNE groups across jurisdictions. The regime is intended to improve stakeholder understanding of corporate tax practices while encouraging greater consistency and accountability in tax reporting.

Key Objectives of Public CbCR Include:

- Enhancing transparency of multinational tax practices across jurisdictions

- Enabling informed public debate on corporate tax contributions

- Promoting fairness and a level playing field across markets

- Supporting better decision-making by investors and other stakeholders

- Strengthening corporate accountability and governance

- Reinforcing trust in the integrity of tax systems

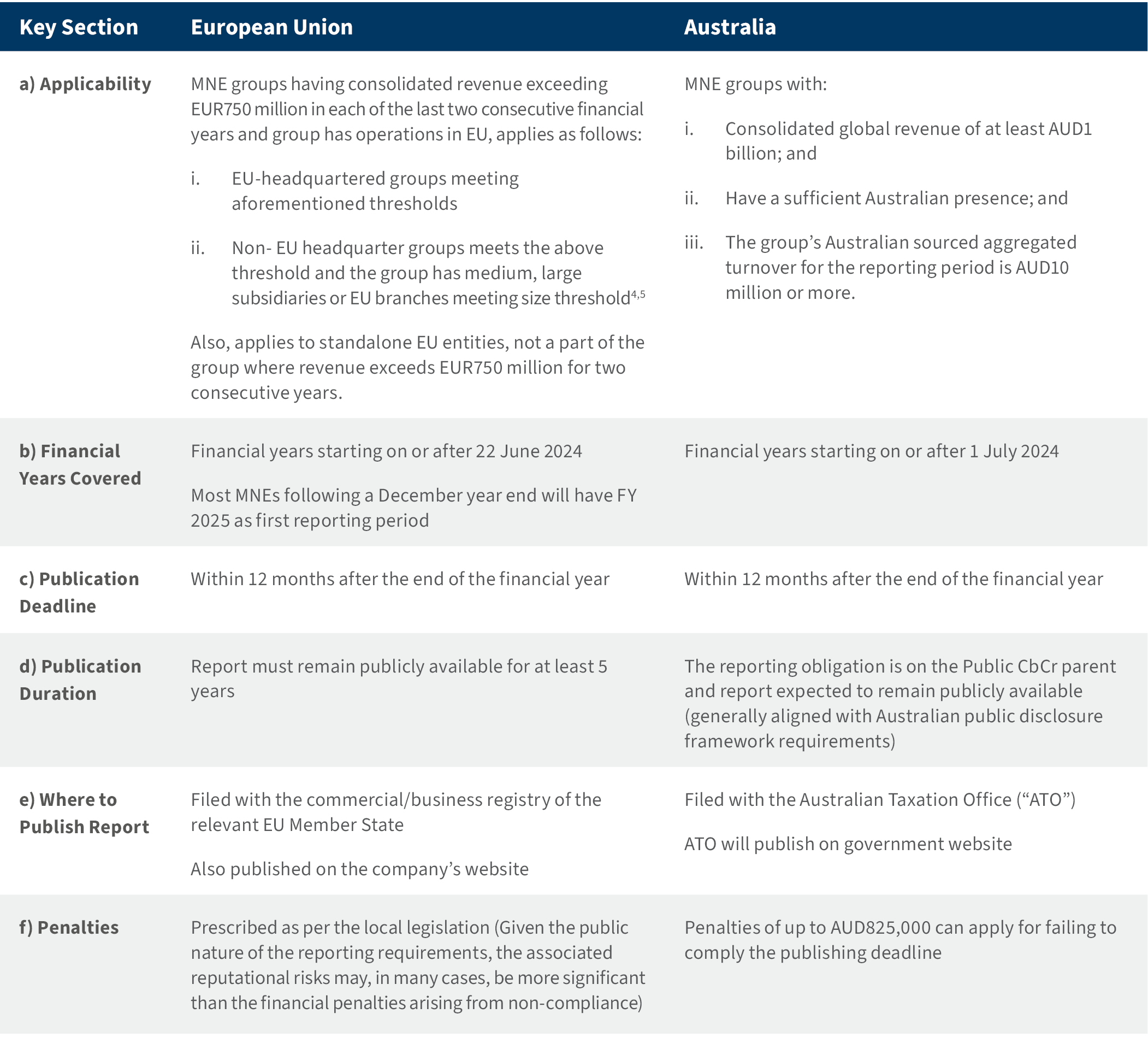

Below Table Provides Key Attributes of Public CbCR

While Public CbCR is currently implemented primarily in the EU, Moldova and Australia, it already affects multinational groups headquartered in other jurisdictions through their overseas operations. Although broader global adoption remains uncertain, MNE groups should monitor developments closely, as tax transparency initiatives continue to expand globally.

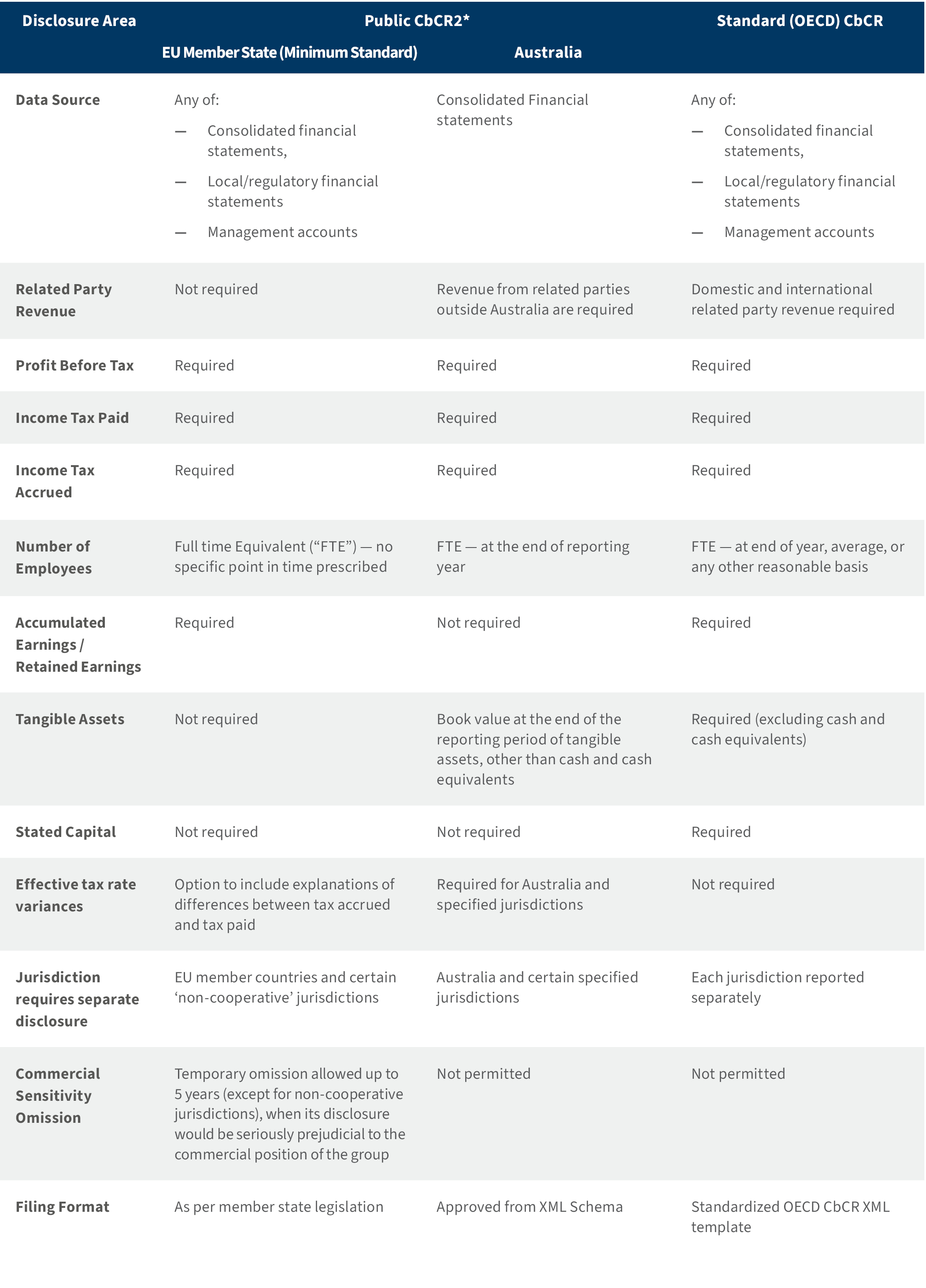

Below Table Provides a Comparison of Key Disclosure Requirements Under Public CbCR and Standard CbCR

*While Moldova’s Public CbCR regime is broadly aligned with the EU framework, it is generally more closely aligned to the OECD CbCR model and may require more granular jurisdictional disclosures, with relatively limited aggregation compared to the EU regime.

Case Study – Applicability of Public CbCR for a UAE Headquartered Multinational Group

Facts

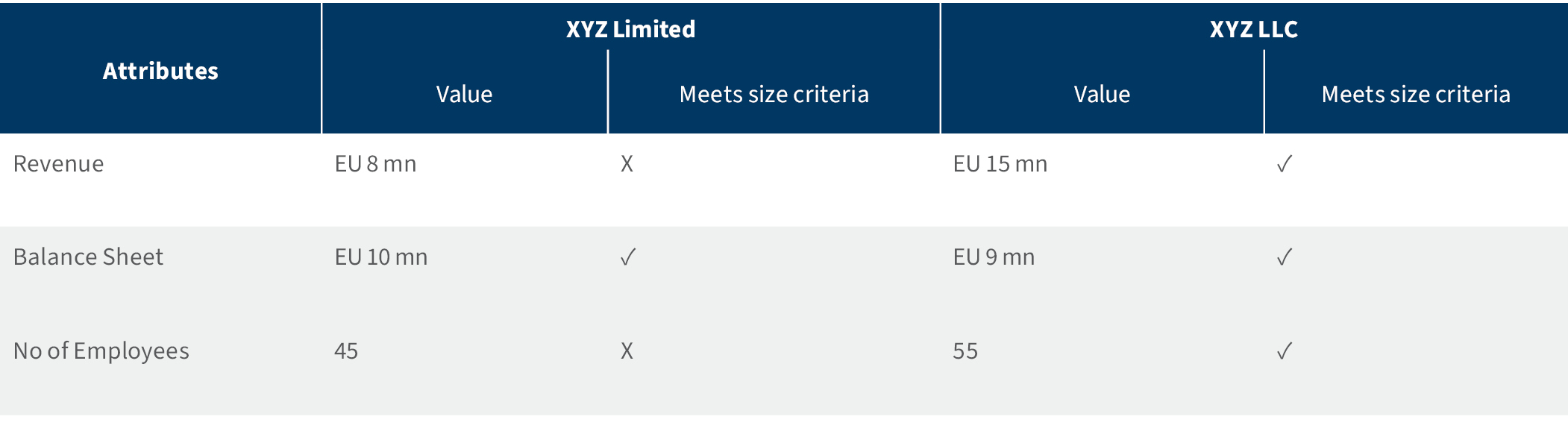

XYZ Group is a MNE headquartered in the UAE, with its Ultimate Parent Entity (“UPE”) located in the UAE. The group reported consolidated revenue exceeding EUR1.5 billion in both FY 2023 and FY 2024 and operates across multiple jurisdictions, including subsidiaries in EU Country 1 and EU Country 2. The financial details of the subsidiaries are set out below:

Assessing the Applicability of Public CbCR

Step 1 – Assessing the consolidated revenue threshold for MNE group: The consolidated revenue of the XYZ Group exceeded EUR750 million in both FY 2023 and FY 2024. Accordingly, the group meets the global revenue threshold applicable for Public CbCR purposes.

Step 2 – Determine whether EU presence triggers Public CbCR: Public CbCR obligations arise where the group has EU subsidiaries meeting the applicable size criteria

For the purposes of our analysis, we have considered the size criteria specified under the EU Directive. However, the thresholds and size criteria under each EU Country Public CbCR regulations may differ and should therefore be assessed separately for each jurisdiction.

Conclusion:

XYZ Limited – The subsidiary does not meet at least two of the three applicable size criteria and, accordingly, does not independently trigger Public CbCR obligations in EU Country 1.

XYZ LLC – The subsidiary meets all three applicable size criteria and, therefore, satisfies the threshold for triggering Public CbCR obligations in the EU Country 2.

Step 3 – Public CbCR Filing Obligations in EU Country 2: The report must be submitted to the commercial registry in EU Country 2 and published on the company’s website.

Although XYZ Limited does not independently trigger Public CbCR filing obligations, the financial and tax information relating to XYZ Limited would still be included in the Public CbCR disclosure, as EU Country 1 is an EU Member State.

Step 4 – Potential disclosure in Public CbCR7: Based on the EU Public CbCR framework, the disclosure may generally be presented as follows:

- Information relating to EU Member States (including EU Country 1 and EU Country 2) would be required to be disclosed separately on a jurisdiction-by-jurisdiction basis

- Information relating to certain “non-cooperative” jurisdictions or other specifically designated jurisdictions may also be required to be disclosed separately

- Information relating to other jurisdictions may generally be aggregated and presented under a single category such as “Rest of the World”

Middle East Perspective

Regional Impact

While Public CbCR has not yet been formally implemented in the Middle East, MNE groups headquartered or operating in the region may still be impacted due to their international footprint. Many Middle East-based groups have operations in the EU, Moldova and Australia through subsidiaries, branches or holding structures. In such cases, Public CbCR obligations may arise in those jurisdictions even where the group’s ultimate parent entity is located in the region.

Practical Readiness Considerations for Middle East Groups

Regional MNE groups with international operations should consider initiating Public CbCR readiness assessments. An effective readiness approach requires clear prioritisation, and a focus on higher-risk and higher-impact areas first. Key steps include: Risk Identification and scoping (Immediate Action)

- Identifying EU and Australian entities within the group

- Assessing whether thresholds in each jurisdiction are met

- Map the reporting requirements across relevant jurisdiction (considering the legislation in each jurisdiction of the MNE group)

The above steps form the foundation for all subsequent work.

Data Readiness and Risk assessment (Near-Term Action)

- Evaluating availability and reliability of jurisdiction level financial data

- Reviewing consistency between OECD CbCR data and statutory financial statements

- Identifying and assessing commercial sensitivity risks associated with public disclosure

Governance (Medium to Long Term Action)

- Establishing governance and internal review frameworks

- Defining clear ownership across tax, finance and legal functions

- Monitoring ongoing regulatory developments globally

Early preparation is particularly important for MNE groups with complex multi-jurisdictional structures, as it allows time to clarify obligations, align data, and manage the narrative around disclosures This is not only due to the scale of coordination required, but also because of the strategic decisions on public disclosure.

Non-compliance with Public CbCR requirements may result in financial penalties, regulatory and legal exposure and reputational risks. Delays can lead to compressed timelines, increasing the risk of errors, regulatory non-compliance, and potential financial penalties. More importantly, given the public nature of reporting, inconsistencies or unclear disclosures may attract scrutiny from regulators, and investors/ stakeholders, creating significant reputational risk. A proactive approach helps mitigate these risks by improving data quality, strengthening governance, and ensuring a clear and consistent approach.

How FTI Can Help

Public CbCR should not only be viewed solely as a compliance exercise. It requires careful interpretation of legislative requirements, robust data alignment, and proactive risk management. FTI supports MNE groups throughout this process by providing:

- End-to-end readiness and risk assessment: We help organizations identify jurisdictions where Public CbCR obligations arise, assess exposure across relevant jurisdictions, and evaluate key compliance, and operational risks.

- Data integrity, alignment, and reputational risk management: We assist clients in ensuring consistency across Public CbCR disclosures, OECD CbCR filings, statutory financial statements, and other regulatory reporting requirements. By minimizing discrepancies and enhancing data integrity, we help reduce the risk of stakeholder scrutiny and reputational challenges.

In addition to these core services, we support implementation through registration and filing assistance, governance framework design, process enhancement, and ongoing monitoring. This enables MNE groups to move beyond reactive compliance and adopt a more strategic, controlled, and sustainable approach to Public CbCR reporting and disclosure.

Conclusion and Key Takeaways

Public CbCR represents a major development in global tax transparency, with implementation already underway in the EU, Moldova and Australia and additional jurisdictions expected to follow. MNE groups, should not view this a routine compliance exercise as it involves public disclosure of sensitive tax and financial data, where errors, inconsistencies, or misinterpretation can carry meaningful regulatory and reputational consequences. MNE groups that fail to adhere to appropriate disclosure and/or compliance, they could potentially expose themselves to public scrutiny, financial penalties and challenges from regulators and stakeholders. Therefore, MNE groups should act now to assess applicability and prepare for compliance to mitigate any potential risks, in particularly.

- Assess the scope independently in each jurisdiction

- Public CbCR Regime differs in jurisdictions in terms of data requirements, jurisdictional threshold and disclosure requirements, therefore, get the data and framework in order

- Prepare for public scrutiny

- Avoid reliance on omissions and/or exemptions

Public CbCR should be approached as a high-stakes reporting disclosure rather than a box-ticking exercise.

Organizations that adopt robust governance and reporting frameworks early will be better positioned to manage both compliance and regulatory obligations and reputational risks in this increasingly transparent environment.

Footnotes:

1: EU Directive 2013/36/EU of the European Parliament and of the council of 26 June 2013

2: EU Directive 2021/2101 of the European Parliament and of the Council of 24 November 2021

3: Link

4: Medium and large subsidiaries are those meeting two of three requirements a) Average number of employees exceeding 50 b) Have balance sheet greater than EUR5 million and c) Have net revenue greater than EUR10 million. A branch simply needs to meet the revenue threshold. These thresholds may be different in some member states according to the local legislation. Refer to legislation in each member state

5: As a general comment, all thresholds for subsidiaries / branches need to be met for a period of two consecutive years. Local implementation might differ in some cases.

6: Some EU jurisdictions (i.e. Romania and Croatia) have incorporated Public CbCR from earlier years, 2023 and 2024 respectively.

7: The local implementation of Public CbCR rules may differ across jurisdictions and may prescribe specific inclusion, exclusion or disaggregation requirements.

Accordingly, the detailed disclosure requirements under the relevant local legislation should be independently assessed and complied with.

Related Insights

Published

June 22, 2026

Key Contacts

Key Contacts

Senior Managing Director

Managing Director

Managing Director