-

July 02, 2018

-

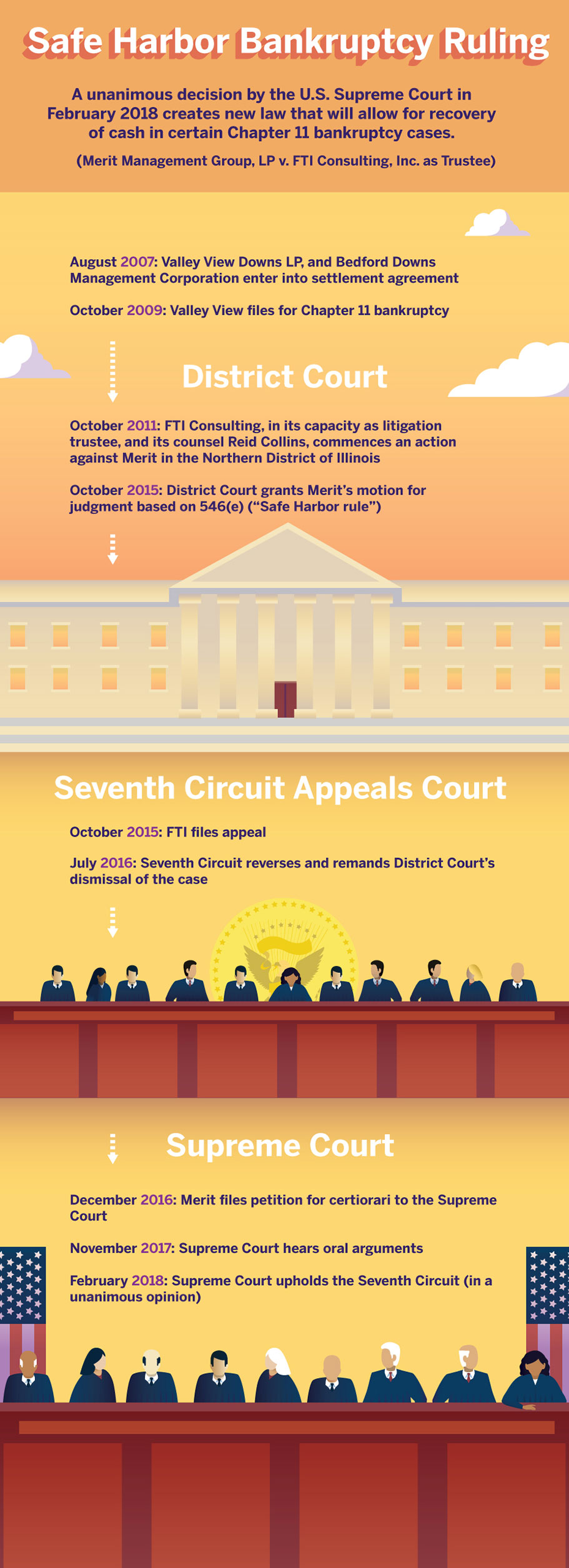

A unanimous decision by the Supreme Court in a case argued by FTI Consulting as trustee will lead to recovery of funds in certain Chapter 11 bankruptcy cases.

How did two Pennsylvania harness racing companies wind up changing the law of the land in the highest court in the land?

That question may sound facetious, but its ripple effects on future financial transactions may not be. In February, the United States Supreme Court upheld a lower court’s ruling that will allow FTI Consulting, as the trustee for creditors of a one-time harness racing operator (Valley View Downs) to sue for recovery of cash in a failed deal with a partner in the same industry.

As trustee, FTI Consulting and its litigation attorneys, Reid Collins & Tsai and Kirkland & Ellis, argued against the questionable application of a long-standing Bankruptcy Code rule by Merit Management. Merit, the former partner, was a shareholder in Bedford Downs.

Attorneys for Merit cited Section 546(e) of the Bankruptcy Code (i.e., the “safe harbor rule”) in the case. The intention was to try to shield $16.5 million Merit had collected in the deal from being “clawed back” and distributed amongst creditors who sustained losses from the bankrupt company.

The safe harbor rule is intended to protect financial institutions from being sued by creditors of a bankruptcy estate, as financial institutions are systemically important to our economy. However, the rule had been historically applied broadly to protect other, non-financial institutions.

The Supreme Court had a different interpretation on February 27. In Merit Management vs. FTI Consulting, all nine justices ruled in favor of FTI Consulting’s position that the safe harbor cannot be used in this instance. Here’s how it happened, and what it may mean in the long run for dealmakers, from starting gate to finish line:

Out of the Gate

In 2007, Valley View Downs agreed to purchase the stock of Bedford Downs Management for $55 million. Valley View’s goal was to limit competition and obtain the last available “harness racing” license in Pennsylvania. From there, Valley View planned to open a “racino” — combination racetrack and casino. $16.5 million was transferred to Merit Management, investors in Bedford Downs in a settlement agreement (i.e., Merit’s ratable share of the $55 million purchase price).

First Turn

Valley View could not secure a gaming license for the casino and filed for Chapter 11 bankruptcy in 2009. FTI Consulting, hired as trustee to recoup losses suffered by Valley View’s creditors, commenced litigation to claw back the $16.5 million from Merit.

Back Stretch

Rather than file in Delaware Bankruptcy Court with unfavorable precedents, FTI Consulting and its counsel Reid Collins selected the Northern District of Illinois Court in 2011 to file suit. In response to FTI Consulting’s action, Merit filed a motion to dismiss, and pointed to Section 546(e) of the Bankruptcy Code (safe harbor). Merit noted that Credit Suisse (the financing bank) and Citizens Bank (Merit’s escrow agent) were financial institution participants in the deal and thus Merit was protected by the safe harbor provision.

Merit won the case in 2015, with the Court decreeing that a transfer is safe harbored if it is made “by or to (or for the benefit of)” a financial institution — even if that institution did not benefit from the transfer.

Second Turn

FTI Consulting and Reid Collins filed an appeal with the 7th Circuit Appeals Court in October 2015. Eight months later, the 7th Circuit reversed the earlier decision, ruling that “it is the economic substance of the transaction that matters” and not merely whether a transfer was made “by or to (or for the benefit of)” a financial institution.

Essentially, because neither Valley View nor Bedford Downs (Merit) were financial institutions, the safe harbor rule did not apply.

Home Stretch

Merit petitioned for the United States Supreme Court to hear the dispute in December 2016. Oral arguments were conducted the following November, which were done by FTI Consulting’s counsel Kirkland & Ellis.

Finish Line

In February, the Court affirmed the 7th Circuit ruling. It made the point that the only relevant transfer to be considered is the one the trustee sought to avoid, and not the component parts. In other words, when considering a safe harbor ruling, the transfers do not apply to the financial institutions between the two parties.

Winner's Circle

FTI Consulting, through its counsel Reid Collins and Kirkland & Ellis, was able to create new law, which may empower creditors who lost money in a bankruptcy to successfully recoup some or all of those losses through litigation. However, as is often the case, the Supreme Court ruling was narrowly tailored; the opinion left certain items open (including the definition of a “financial institution”) — which may be the subject of future challenges and litigation.

© Copyright 2018. The views expressed herein are those of the authors and do not necessarily represent the views of FTI Consulting, Inc. or its other professionals.

About The Journal

The FTI Journal publication offers deep and engaging insights to contextualize the issues that matter, and explores topics that will impact the risks your business faces and its reputation.

Published

July 02, 2018

Key Contacts

Key Contacts

Senior Managing Director