-

February 29, 2020

-

As the tariff dispute between the U.S. and China continues to create uncertainty, U.S. businesses are considering all alternatives to maintain cost-effective production.

Is “Made in China” still a top choice for American manufacturers?

That is the prominent question America’s business sector has been contemplating since July 2018, when the U.S. government slapped an additional 25 percent tariff on top of existing tariffs on products imported from China.

With the tariffs valued at $USD 34b annually, this has ignited a volatile, unpredictable two-year trade war between the world’s two largest economies. Recent additional tariffs from the U.S., reaching upwards of 30 percent ($550b), only heightened the tension.

While the two countries continue to negotiate a new trade deal — the U.S. and China signed “Phase 1” of an agreement on January 15 intended to reduce tariff rates and improve business relations between the two countries — the ongoing uncertainty of the situation, combined with the rapidly increasing wages in China, have called into question the viability of China as a one-stop source for low cost sourcing of goods.

If China is off the table, despite its powerful supply chain system, economy of scale, and well-developed infrastructure, then which country should U.S. manufacturers consider as alternatives?

China Plus One

The trade war came at a time when large Chinese manufacturers were beginning to shift smaller portions of their production capacity to other Southeast Asian countries to take advantage of low labor costs. However, these manufacturers still maintained a majority of their production in China to give them a degree of flexibility — a strategy now known as “China Plus One.”

As the trade war escalated and tariffs increased, moving the entire manufacturing process to outside countries was becoming an attractive option, especially for Chinese suppliers heavily dependent on the U.S. market. Doing so helped these businesses capitalize on competitive cost advantages.

To better understand the situation, FTI looked at alternative low-cost countries in Asia, focusing analysis on the two potential impacts that may benefit those nations:

- Short term product replacement

- Long term production and Foreign Direct Investment (“FDI”) shift.

FTI found that for U.S. customers, Vietnam and India were ranked as first-tier alternate sourcing destinations. The Philippines, Malaysia, Indonesia, Thailand and Bangladesh were ranked second-tier low cost countries, given their unique advantages on certain country-specific resources and products. Third-tier countries included Laos, Mynamar and Cambodia.

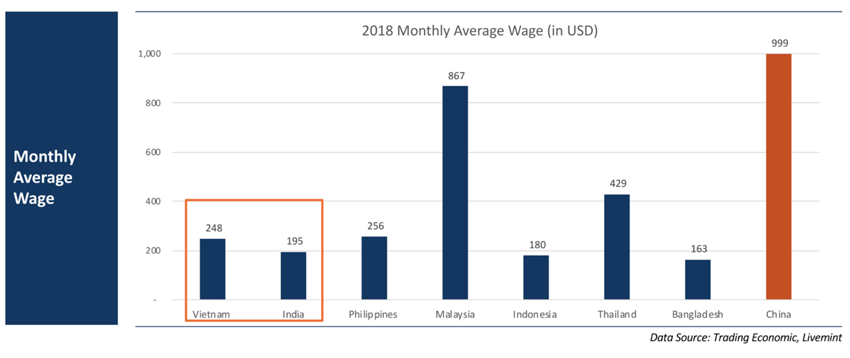

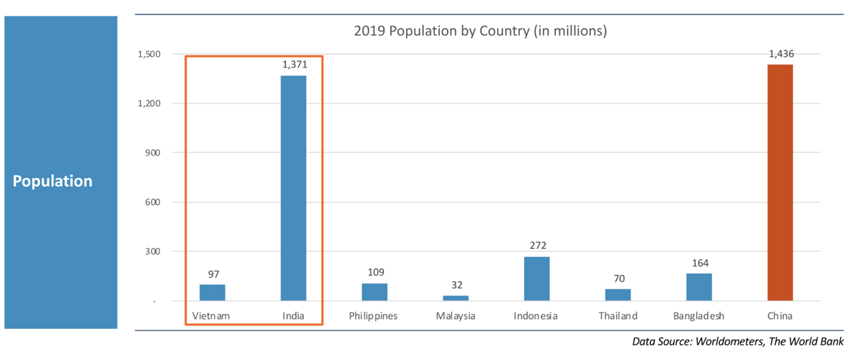

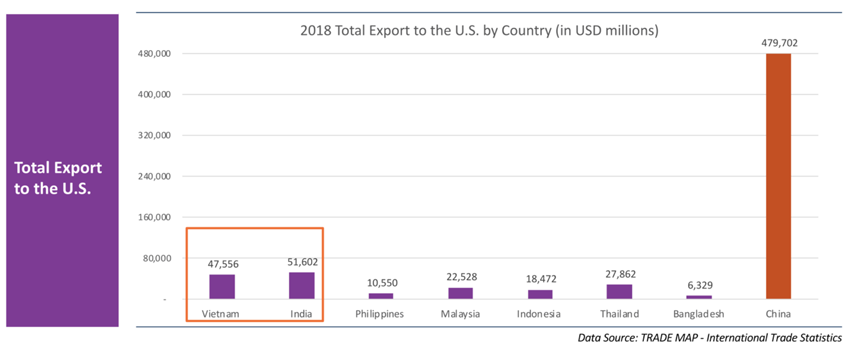

The following three charts show various data often used by U.S. manufacturers when considering major Asian countries for low-cost sourcing.

Which Alternative Country is Best?

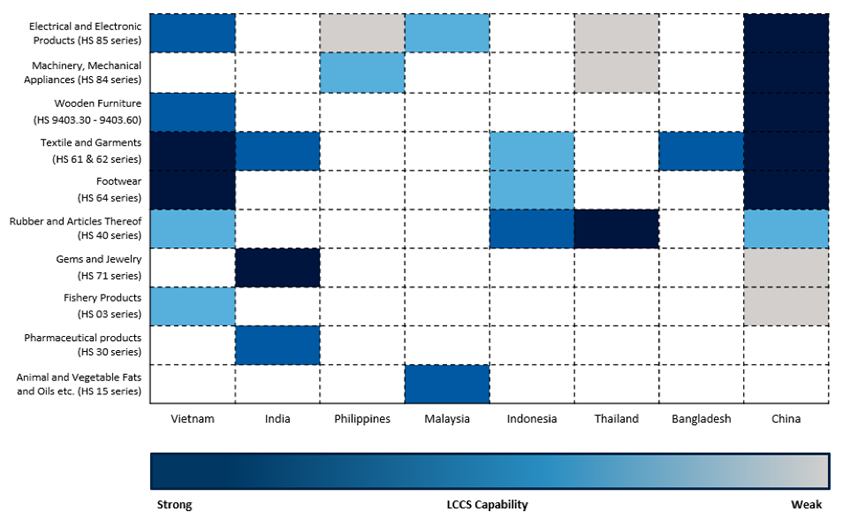

By breaking down the main product groups that are exported from these countries to the U.S., FTI created a heatmap (see below) that highlights the LCCS capabilities of each alternate country by listing their advantaged product categories.

This heatmap clearly illustrates that traditional labor-intensive industries such as textile, apparel and footwear — which are threatened by rising labor costs but with relatively low technological barrier — will be mostly affected by the extra tariff increase. For that reason, U.S. companies may want to consider shifting their procurement focus from China to countries like Vietnam, India, Indonesia and Bangladesh.

For product categories that require some sort of engineering processes (e.g. electrical and electronic products, machinery and mechanical appliances), countries such as Vietnam, Malaysia, and the Philippines have proven value. These countries have already gained necessary experience and built up strong capabilities over the years by acting as original equipment manufacturers (OEMs) for large corporations like Apple, Nokia and Samsung.

Although the current strengths of these Asian countries are largely tied to low value-added assembly works, it is expected that with an increase of incoming FDIs into those nations, a better fundamental of a capital-intensive industry and supply chain system will emerge. This should be a benefit both local suppliers and the buyers from the U.S.

The heatmap also indicated several other low-cost sourcing opportunities for natural resource products like rubber, fishery products, animal and vegetable oils. These opportunities are primarily found in Vietnam, Malaysia, Indonesia and Thailand. In India, the country offers resource opportunities like gems, jewelry, and pharmaceutical products (e.g., generic drugs) due to culture, tradition, and regulation factors.

Heatmap highlighting low-cost country sourcing capabilities in major Asian countries.

Despite the appeal and diversity of resources these alternative trade partners offer, one truth remains: they’re still not China. China will continue to be a top sourcing destination, now and in the foreseeable future.

A look at China’s well-developed and powerful supply chain system that has been built up over the last 30 years demonstrates unique advantages in raw material availability, scale of production, logistic efficiency, human capital and business intelligence.

Because of this, a more balanced “China Plus One” approach is recommended as a preferred LCCS strategy for procurement executives in order to factor all risks into their sourcing decisions and processes.

© Copyright 2020. The views expressed herein are those of the author and do not necessarily represent the views of FTI Consulting, Inc. or its other professionals.

About The Journal

The FTI Journal publication offers deep and engaging insights to contextualize the issues that matter, and explores topics that will impact the risks your business faces and its reputation.

Related Information

Published

February 29, 2020