The Caracas Investment Clock

A Framework for Navigating Venezuela’s Reopening

-

June 26, 2026

-

Note: The recent earthquakes in Venezuela have understandably shifted the focus to safety and recovery. As the situation stabilizes, we will update the investment clock. Our thoughts are with the Venezuelan people during this time.

Complexity Without a Compass

Venezuela should be an investor’s dream: the world’s largest proven oil reserves, a young and educated population and strategic geography linking Caribbean, Andean and Atlantic markets. Instead, for more than two decades, it has been a cautionary tale, sealed shut by expropriations, comprehensive U.S. sanctions, executive consolidation of institutional authority and the entrenchment of informal networks deeply embedded in state institutions.

But something has shifted. The events surrounding the capture of Nicholas Maduro on January 3, 2026, cracked open a door sealed for nearly a decade. Sanctions are being lifted and compliance pathways are being defined. Sophisticated investors are now asking a question that was unthinkable 150 days ago: Is it time to look at Venezuela again?

Strategic and tactical answers are nuanced — and navigating those nuances requires a purpose-built framework.

Enter the Caracas Investment Clock: Reading the Hands

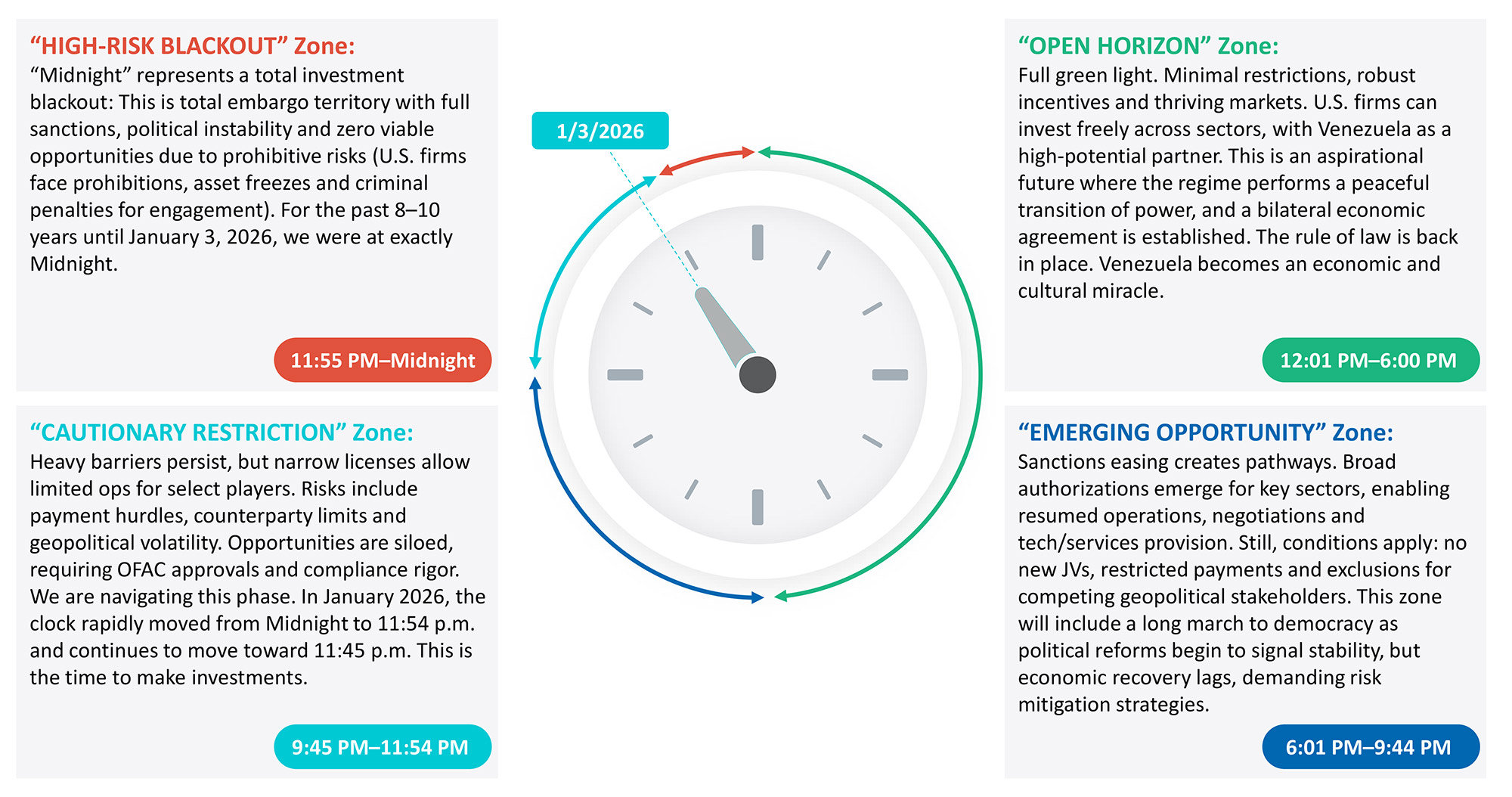

The Caracas Investment Clock translates an extraordinarily complex web of sanctions policy, government behavior, political reform and geopolitical risk into a single, intuitive and dynamic metaphor. The clock face spans from Midnight (total investment blackout) to High Noon (a fully open, thriving investment environment) across four distinct zones.

The clock can move forward and backward and is asymmetric by design. The two restrictive zones — High-Risk Blackout and Cautionary Restriction — occupy 25% of the clock face. The two opportunity zones — Emerging Opportunity and Open Horizon — span 75%. This encodes a fundamental truth of political economy: It is far easier to destroy value than to build it. A single policy action, a disputed electoral cycle or a recalibration of the sanctions architecture can slam the hands to Midnight in days or hours. Building the conditions for open investment — institutional trust, rule of law, bilateral agreements, economic stability — requires sustained effort across multiple dimensions over a prolonged period of time.

For roughly a decade, the clock sat frozen at Midnight. The events of January 3, 2026, moved it rapidly to approximately 11:54 p.m. — firmly within the Cautionary Restriction zone. Since then, the clock has been trending toward 11:45 p.m. This is not an all-clear, of course. Governance structures face significant transparency and compliance deficits. Requirements by the U.S. Office of Foreign Assets Control (“OFAC”), that administer and enforce economic and trade sanctions based on U.S. foreign policy and national security goals, are stringent and in force. Competing geopolitical stakeholders (Russia, China and Iran) maintain significant strategic interests. But, for the first time in a decade, the door to Venezuela is open: barely, conditionally and with hazards on every side, but ultimately open.

The Paradox of the Cautionary Restriction Zone

The optimal time for foreign direct investments to position for an opportunity is not when conditions are ideal — it’s when conditions are just barely permissible. History validates this, though with an important caveat.

In Myanmar, after reforms beginning in 2011, in Cuba during the Obama-era opening in 2014, in Iran during the Joint Comprehensive Plan of Action (“JCPOA”) window, early players sought to capture disproportionate value relative to those who waited. In Myanmar, Coca-Cola, GE and VISA moved to establish structural footholds across a 50-million-person untapped market years ahead of slower entrants.1 Cuba became Airbnb’s fastest growing market globally within months of entry.2 And Airbus moved quickly to deliver three aircrafts to Iran Air while Boeing, who moved more cautiously, delivered zero before the window re-closed.3

But the windows closed in all three cases. Myanmar’s 2021 coup forced mass corporate withdrawals. Trump-era reversals forced Airbnb to drastically curtail services in Cuba and nullified Total’s $5 billion South Pars gas concession in Iran. Firms with heavy fixed-capital exposure absorbed real losses.4

The lesson is not “invest blindly when the door cracks open.” It is that ‘positioning’ and ‘deploying’ are fundamentally different acts. Positioning when basic conditions are permissible allows for firms to eventually deploy and capitalize on new markets. Firms that follow this approach tend to be more resilient when political reversals occur and are able to be first in line for the next cycle. However, those who wait for certainty that never fully arrives will get nothing in any scenario.

For Venezuela, this distinction is critical. Without an independent judiciary or durable rule of law, heavy capital deployment remains premature. The firms that will capture the most value in Venezuela’s eventual reopening are those positioning themselves now — building the institutional muscle memory that converts optionality into action the moment the clock advances.

What Moves the Clock — Forward and Backward

Three interlocking levers — and a constellation of secondary forces — govern the clock’s direction. Investors who track only one will misread it.

-

Rule of Law and an Independent Judiciary. This is the structural lever, the one that determines whether the clock can ever cross from the Cautionary Restriction zone into the Emerging Opportunity zone. Venezuela’s judicial institutions have not yet demonstrated the independence that institutional investors require for long-duration capital commitments. Expropriations and arbitration proceedings are still too fresh. Speculative capital can operate in the current zone on deal-specific risk appetite, but massive investments from the oil giants, pension funds, sovereign wealth funds and multilateral development banks — the capital that rebuilds economies — will not enter without enforceable contract law, credible property rights protections and a viable path for the resolution of arbitration cases.5

This challenge extends beyond establishing judicial independence. The effective exercise of state authority — including the ability to enforce contracts, guarantee security of personnel and operations, and ensure consistent application of regulatory frameworks across the national territory — requires a consolidation of institutional capacity. Where the state’s reach is uneven, informal power structures will inevitably fill the vacuum, creating layers of counterparty risk (e.g., opaque ownership structures, unreliable contract enforcement, informal actors embedded in local supply chains) that no OFAC license can address.

-

The U.S. Electoral Cycle. This is the tempo lever. The current policy architecture — OFAC licensing windows that moved the clock from Midnight — rests on executive action, not legislation. The November 2026 midterms and the 2028 presidential election are sequential inflection points. For instance, a congressional shift toward legislative sanctions would structurally seal a door that executive action can currently open and close. A change in administration could reset the clock entirely. This creates the window problem: The optimal time to act is now, but the durability of the window of opportunity is uncertain. The lesson here is that those who wait for political certainty may wait forever.

-

Geopolitical Realignment. This is the wildcard. Venezuela sits at the intersection of competing geopolitical stakeholders. For example, the Middle East dimension connects it to the most volatile theater in U.S. foreign policy. The paradox: U.S. pressure on Iran can accelerate Venezuela’s clock if Washington continues to push Caracas toward Western alignment. But, escalation that draws Venezuela into broader geopolitical confrontation would freeze or reverse it. The risk vectors are specific: sanctioned organizations maintaining operational or financial footprints inside Venezuela, Venezuelan entities serving as intermediaries for sanctions evasion by third countries, or deepening military and security cooperation between Caracas and designated foreign partners. Any one of these could trigger a U.S. policy response that re-escalates the sanctions architecture.

-

Other Forces. The three levers above are primary, but they are not exhaustive. Oil prices, the pace and scope of sanctions relief, regional migration dynamics, shifts in multilateral lending policy, and commodity market volatility, among others, all exert gravitational pull on the clock. No single lever is likely to move the hands as decisively as the primary three — but, in combination or in moments of compounding stress, they can accelerate or stall the clock’s movement in ways that resist prediction.

How they interact: Rule of law is the foundation. The U.S. electoral cycle sets the tempo. Geopolitical realignment is the shock variable. And, a constellation of secondary forces — from oil prices to sanctions architecture — shapes the environment in which all three operate. The framework demands monitoring them simultaneously.

A Call for Strategic Patience — and Strategic Urgency

The Caracas Investment Clock does not predict if or when Venezuela will reach the Open Horizon zone. It provides a structured and dynamic framework for assessing where Venezuela stands at a given point in time and what would need to change to move it toward more favorable conditions.

For policymakers, the clock interprets the impact of sanctions calibration in investment-relevant terms. For investors, it provides a shared vocabulary to discuss risk/reward in a jurisdiction that defies easy categorization. For Venezuelan civil society, it offers hope — framed in the concrete language of economic reopening.

Footnotes:

1: “Coca-Cola Starts Local Production in Myanmar,” The Coca-Cola Company (4 June 2013); Reuters, “General Electric Secures First Myanmar Deal After Sanctions Ease,” HuffPost (14 July 2012); and Mahtani, Shibani, “Visa Set to Enter Myanmar,” The Wall Street Journal (19 August 2012).

2: “Americans turn to Airbnb service to see ‘real’ Cuba,” CBS News (21 March 2016).

3: “First new Airbus in decades arrives in Iran,” Al Jazeera (12 January 2017).

4: “Foreign companies withdrawing from Myanmar after coup,” Reuters (27 January 2022); Lapan, Tovin, “U.S. settles with Airbnb over alleged Cuba violations,” Travel Weekly (4 January 2022); and Ellyat, Holly, “Oil giant Total has pulled out of Iran and giant gas project reports say,” CNBC (20 August 2018).

5: Alberro, Jose and Veronica Irastorza, “Venezuela’s Oil Sector Recovery: Navigating the Post-Maduro Investment Landscape,” FTI Consulting (10 March 2026).

Related Insights

Related Information

Published

June 26, 2026

Key Contacts

Key Contacts

Senior Managing Director

Managing Director

Managing Director

Managing Director