Why Isn’t There More Concern About Recession Risk?

-

April 13, 2026

-

Since military action against Iran began on February 28, there has been considerable business media coverage about the wider implications of these hostilities on the global economy, mostly around their impacts on gasoline and other energy prices, and higher inflation generally, as reduced shipping of all products through the region inevitably makes its impact felt on the global supply chain. These are not exaggerated concerns. We’ve all learned in recent weeks that 20% of globally shipped oil travels daily through the Strait of Hormuz, which effectively has been closed, causing global oil supply to drop by 11 million barrels per day in March, or about 10%, even after coordinated efforts to counter some lost supply through the Strait — mainly a scheduled release of 400 barrels of oil arranged by the member nations of the International Energy Agency (“IEA”) and some temporary sanctions relief. The IEA claims the war’s impact, “has created the largest supply disruption in the history of the global oil market.”1 Knock-on effects for key energy-derived products or ingredients, such as agricultural fertilizer and chemicals, is less talked about but no less concerning. Moreover, damage to energy infrastructure in the Gulf region since the war began, such as substantial damage to nearly one-fifth of Qatar’s LNG processing capacity that will take several years to repair,2 will ensure some lasting impacts on energy production and processing long after hostilities eventually cease.

For the U.S. economy, the timing of these sudden events is especially concerning, as wholesale inflation ticked notably higher in February before hostilities began, while 4Q25 GDP was revised sharply lower from its initial estimate. Consumer sentiment was already hovering near record lows per the University of Michigan’s Surveys of Consumers.3 The business media’s singular focus on energy impacts and inflation is understandable, as that is the most immediate concern and first transmitted effect in a consumer-driven economy, but there has been considerably less explicit discussion from journalists, market observers and economic pundits about the dreaded R-word and what exactly it would take to tip the U.S. economy — perhaps the global economy — into recession. Furthermore, financial market selloffs since hostilities with Iran began have been fairly orderly and contained rather than panic driven, while capital markets activity, such as M&A and securities issuance, has only cooled slightly in the face of these daunting global concerns, with Goldman Sachs’ co-head of M&A in Europe heard recently stating, “…companies can’t afford to wait out the volatility gripping global markets to pursue strategic mergers and acquisitions.”4

Why aren’t financial markets and business leaders girding for something worse? There are several contributing reasons.

Recession Calls Are Usually Wrong: Predicting recessions always has been an occupational hazard for economists, and that has been even more true in recent years. The U.S. has not experienced economic contraction that qualified as a traditional recession since 2008-2009 — and along the way there have been many bad calls by a profession that supposedly knows best about these matters.5 True, the COVID-19 pandemic ushered in a very brief recession that was over by July 2020, yet many economists expected that downturn to endure many months longer than it did (and by the old textbook definition it would not have even qualified as one). Conversely, the spike in inflation in 2021-2022 and subsequent monetary tightening response by the Fed through early 2024 ratcheted up widespread expectations of recession — all of which came to naught as the U.S. economy kept chugging along. Market signals and other once reliable indicators of likely recession have been off the mark as well. Recessions have become more infrequent in recent decades, and most indicators that historically predicted them with some fair degree of accuracy are no longer dependable.6

Pollyannaish Optimism and FOMO Still Rule: Many seasoned, decision-making professionals have never experienced a good old-fashioned recession (or credit default cycle) in their working careers and are not inclined to think in terms of precipitous or prolonged business or market adversity. For many of the under-45 crowd, all storms will pass quickly, and all adversity is opportunity. Perhaps it is this perpetually upbeat outlook that has contributed to market resilience and helped keep our economy rolling along through some rough patches. The COVID-19 experience was a brief outlier event that reinforced this “plow through it” mindset, though it often goes unmentioned or unremembered that it required trillions of dollars in global government support to prevent economic collapse — money that won’t likely be there for the next major crisis. Such prevailing optimism arguably reflects underlying complacency.

Markets Don’t Expect the War in Iran To Last Much Longer: Oil futures markets are inverted, with spot prices trading considerably higher than futures prices. While WTI crude oil is trading at $92 in the spot market, December 2026 futures are trading near $76 per barrel and June 2027 futures are near $72. Such price inversion reflects a market expectation that oil markets will soon normalize. Not everyone is so sanguine, though: Saudi Aramco said oil prices could reach $180 per barrel if the war continues past April.7 Optimism implied by futures prices suggests that oil is a merely a spigot flow that will resume at pre-war levels once the bombs stop falling. That view seems simplistic and overlooks the damage done to “the plumbing” as well as the lingering economic impact of heightened tensions in the region even after current hostilities cease. Several prominent industry experts are not as hopeful that energy markets get back to normal so quickly: for example, the CEO of Kuwait Petroleum Corp. said it would take several months for shut-in wells in the Gulf region to get oil production back to pre-War levels.8

TACO Traders Still Believe: President Trump often is unpredictable when it comes to key U.S. policy decisions, making it difficult to predict his next move or make economic calls based on his last move. But he seems to pivot in response to extreme financial market reaction to some policy overtures. It happened with tariffs and Greenland, and again recently when he postponed his threat to bomb Iran’s power infrastructure when markets went into selloff mode. TACO traders believe the President walks back from the precipice when markets sell-off sharply. Will he persist with a war that could soon imperil the global economy? Many traders believe that declaring victory before that moment comes is a more probable outcome, but it is not evident where that tipping point is. Moreover, damage to the global economy has been done and a snap-back response doesn’t seem to be a most likely scenario, especially in light of other nagging economic concerns.

Prediction Markets: New Ways To Gauge Recession Risk or Amateur Hour?

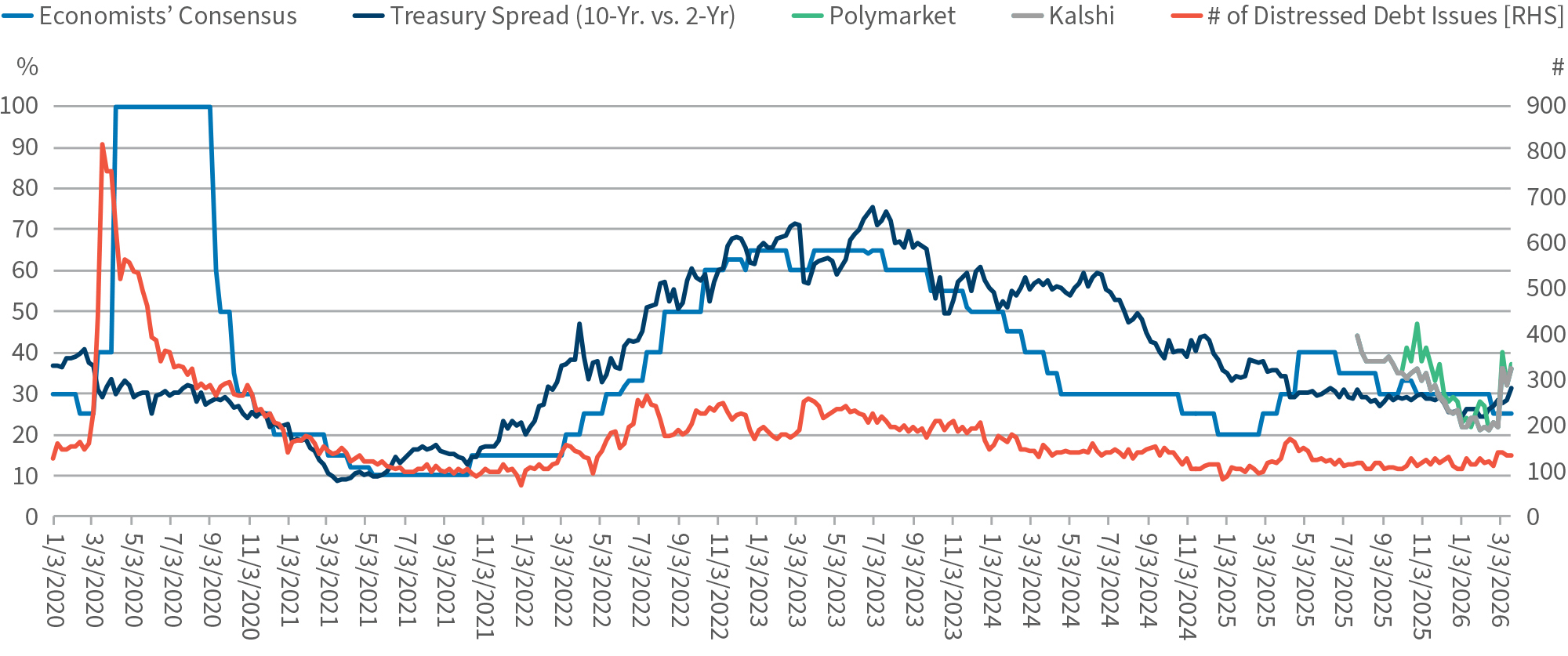

As we’ve said, predicting recessions is often a fool’s errand. Figure 1 shows recession probabilities stated or implied by three indicators since 2020, including Bloomberg’s consensus expectations of recession likelihood among polled economists, a recession prediction model derived from the yield spread between 10-year and 2-year Treasuries, and the number of corporate debt issues trading at distressed yields. The first two indicators spiked to a 60%-75% likelihood of recession throughout much of 2023 amid the Fed’s monetary tightening cycle. Leveraged credit markets were far closer to getting it right during that time, with the number of distressed debt issues moving slightly higher in 2023 but nowhere remotely near its peak levels during the early days of COVID-19, which, incidentally, it also got closer to right in anticipating a quick economic recovery from the pandemic several months before most economists did.

Currently, none of these three indicators is flashing red with respect to an upcoming U.S. recession, though Bloomberg’s most recent polling of economists came in late February before the war with Iran began, and almost certainly will tick higher than 25% in the next monthly reading. Of note, the number of distressed debt issues moved slightly higher in March to 134 from 105 at year-end but remains well below its level of 171 in April 2025 when reciprocal tariffs were announced. In short, credit markets became more unglued in the month following Liberation Day than at the start of the Iran conflict. By July 2025, the number of distressed debt issues was back to pre-Liberation Day levels, as markets concluded that initially posted reciprocal tariff rates would not prevail. That might help explain the muted response to this war, with credit markets widely expecting a cessation of hostilities before its effects torpedo the global economy.

Prediction markets, which have exploded in popularity in the last couple of years, are a new way to divine recession risk and many other economic events, with some caveats. Prediction markets are still in their infancy, and it is hard to discern whether these markets are reliable indicators of future economic performance. Historical data on the recession market is only available going back to mid-2025. On the one hand, these are the expectations of “the rabble” lacking in subject matter expertise and deep insights. However, these participants are putting money on the line, so their betting convictions are more likely to be genuine, unlike myriad consumer surveys where respondents’ biases — particularly political biases — often seep into many of their responses. Moreover, prediction markets live in real time and trade 24/7, so there’s constant immediacy, and little concern about lagging or stale price-implied probabilities.

It’s helpful to view consensus expectations of prediction markets like Yelp or Rotten Tomatoes reviews. If 35 reviewers on Yelp rate a restaurant 4.5 out of 5, it may not sway you given the small number of reviews, but if 700 reviews rate it similarly, you are more likely to go there for dinner. Larger numbers usually confer greater confidence in the objective accuracy of the rating. And so it is with prediction markets. Both Polymarket and Kalshi offer markets odds on whether the U.S. will be in recession within a year, with probabilities derived from the Yes/No wagers in this market, and users on the Kalshi or Polymarket platforms can view total wagers and trading volume in any market in sizing up how deep and robust a market is.

What Are Prediction Markets Saying Currently?

Currently, both prediction markets indicate a 36%-37% probability of U.S. recession by year end compared to the low 20% range just prior to the start of war with Iran (Figure 1). That is telling information, and though not alarmingly high, it is notably higher than the other incumbent recession indicators. The people have spoken and will continue to speak in prediction markets, and despite numerous criticisms leveled at prediction markets, including lack of regulation, insider trading allegations, encouragement of gambling and the gamification of all things including war and death, they likely are here to stay as many of these issues will be addressed in time. It invites the question: can bankruptcy market predictions be far off?

Implications for Restructuring Activity

While traditional restructuring activity isn’t exactly making eyes pop in recent months, there are some cracks in the foundation that everyone is watching, namely all-out efforts by distressed companies to effect a restructuring by any means other than a trip to the courthouse. Out-of-court tools like Liability Management Exercises (“LMEs”) and Distressed Debt Exchanges (“DDEs”) are the currency of the realm at the moment, but many of these remedies are just building a swell that could become a filing wave. Moreover, outsized investor redemption requests at some high-profile private credit funds and the sharp selloff of public Business Development Companies (“BDCs”) that provide debt financing to growing or stressed firms are indicative of a loss of confidence in a $1 trillion asset class globally.

Will deteriorating loan performance soon follow or is this a panic moment that will pass? Perhaps the selloff is overdone, but many investors are coming to the realization that they don’t really know what’s under the hood at some of these credit funds — and it’s not worth the capital risk for single-digit investment returns. It’s a paradigm shift in the making. Some other high profile bankruptcy cases involving alleged massive borrower fraud have elicited concerns about the consequences of lax lending standards and poor loan monitoring across leveraged lending markets in recent years. All of this is layered on top of a speculative-grade U.S. corporate sector that is as levered as ever. It adds up to heightened financial vulnerability to economic and business adversity.

There’s an old saying that the bigger the potential crisis, the less likely it is to occur. Why? Organized bodies, be they governments, markets, corporations or international agencies, inevitably will rise to the moment, perhaps at the eleventh hour, and act to avert a catastrophic event or outcome that is addressable before it occurs. That is a perfectly reasonable expectation — until it isn’t. Should hostilities in Iran and the Middle East region continue for just a couple of months longer, a possibility not entirely within U.S. control, a global recession likely lies in wait and there will be nothing “run of the mill” about it.

Figure 1 – Recession Probability

Source: Polymarket, Kalshi, Federal Reserve Economic Data (“FRED”).

Footnotes:

1: “Oil Market Report – March 2026,” IEA (March 12, 2026).

2: Patricia Cohen, “War’s Attacks on Energy Could Turn Economic Shock into Long-Term Damage,” The New York Times (March 23, 2026).

3: “Final Results for March 2026,” University of Michigan Surveys of Consumers (accessed April 7, 2026).

4: Crystal Tse, “Goldman Tells Dealmakers Not to Wait for Perfection in M&A,” Bloomberg News (March 19, 2026).

5: Tyler Cowen, “How Were So Many Economists So Wrong About the Recession?” Bloomberg (December 26, 2023).

6: Patricia Cohen, “The Global Economy’s Warning Signals Are Broken,” The New York Times (February 3, 2026).

7: Summer Said, “Saudi Arabia Sees a Spike to $180 Oil if Energy Shock Persists Past April,” The Wall Street Journal (March 19, 2026).

8: Spencer Kimball, “How the Big Oil and Gas CEOS Think the Iran War Supply Disruption Will Play Out,” CNBC.com (March 28, 2026).

Related Insights

Related Information

Published

April 13, 2026

Key Contacts

Key Contacts

Global Chairman of Corporate Finance