Consumers Squawk at “Higher for Longer” Oil Prices but Financial Markets Couldn’t Care Less

-

May 28, 2026

Downloads Download Article

Download Article

-

The United States and Iran continue to work towards a permanent end to hostilities in the Gulf region that are inflicting daily damage on global trade and causing energy prices to soar while a shaky ceasefire holds. But financial markets have moved on from the conflict after an initial sharp selloff, convinced either that a peace deal is coming and economic normalcy will soon return, or that the economic impact of this Middle East showdown doesn’t matter enough in the larger scheme of things. Either way, such assumptions seem blithely optimistic. The toll that this conflict is inflicting on the global economy mounts weekly, and there is a point at which the financial damage cannot be easily repaired even if a peace agreement is reached.

While both parties to this conflict have given indications they want hostilities to end for good, there are incentives in place that motivate its continuation in some form, perhaps for longer than the global economy can tolerate. Knowing that it cannot win a military confrontation, Iran understands that its best leverage to negotiate an acceptable outcome is to continue holding the global economy hostage via its near closure of the Strait of Hormuz and its ongoing ability to threaten or attack Gulf region energy assets. By prolonging its blockade of shipping traffic in the Strait while reportedly refusing to surrender its uranium stockpile1 under any deal it would accept, Iran is also betting that any resumption of attacks will not happen.

Meanwhile, the Trump administration cannot exit this conflict without credibly projecting to Americans that it has achieved its stated objectives, which do not include Iran maintaining its nuclear ambitions2 or enriched uranium stockpiles or exerting any degree of influence or control over shipping passage in the Strait of Hormuz. The situation has the ingredients of an enduring impasse, and the fits and starts that peace negotiations have encountered in recent weeks are evidence of that stalemate.

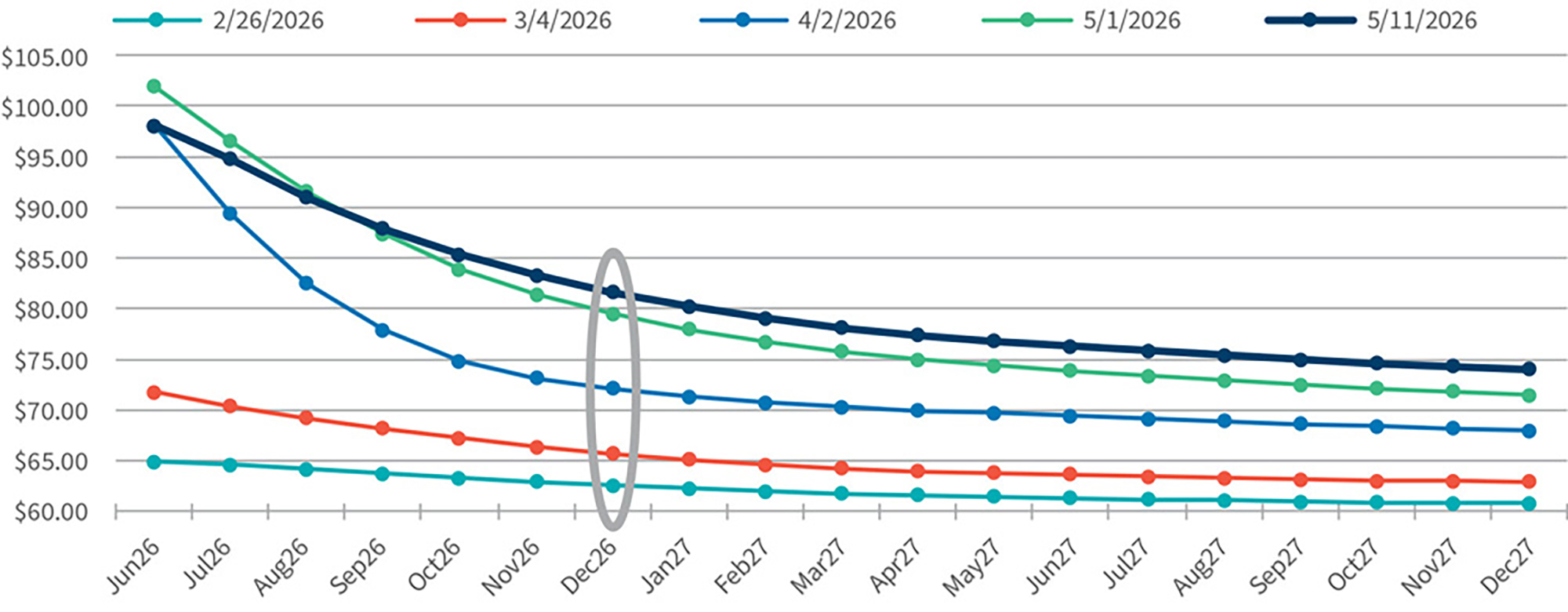

Concavity of the WTI Oil Strip Curve Has Changed Since March, Now Indicating Higher Prices for Longer

Oil prices have gyrated in recent weeks as rumors of an impending peace deal take hold and then fade, with the most severe price action hitting contracts for delivery in the next couple of months. From the war’s onset, oil futures markets have priced in an assumption this conflict would be short-lived, resulting in an inverted price curve for most exchange-traded crude oil products, with near-month prices running considerably higher than contracts for delivery that are months away. However, pricing trends have changed shape notably when we compare WTI oil strip curves at various dates since the war began. What these strip curves tell us (Figure 1) is that expected oil prices in late 2026 currently are considerably higher than they were just a few weeks ago, indicating a lasting impact of this conflict on oil prices for months after hostilities assumedly will end. WTI oil prices for the June 2026 contract hovered above $98 per barrel on May 11, the same price for the same contract month as on April 2. However, the WTI price for the December contract was nearly $82 per barrel on May 11, higher than the $72 per barrel price on the April 2 strip curve, and far above the $66 per barrel price for the December contract back on March 4, the week after the war began. Prior to the start of the war, WTI oil for the December contract was $63 per barrel on February 26. What these price changes point to is an evolving expectation since the war began that oil prices will remain well above pre-war prices at least through 2026 and into next year (Figure 1). Whether the U.S. economy can withstand oil prices remaining in the $80-$85 per barrel range indefinitely (accompanied by higher inflation overall) is a worthwhile debate, as very few energy pundits or traders now expect a fallback to early 2026 prices within the near future. Moreover, energy prices propelled by a shock event always come down more slowly than they spike at the consumer level, so meaningful relief at the gas pump likely is still months away.

Figure 1 - WTI Oil Strip Curve

Source: Bloomberg

Financial Markets Roar Despite the War

Incredibly, financial markets have brushed off earlier concerns of economic fallout resulting from the Iran war and other hostilities in the Middle East region. Market sentiment firmly seems to believe President Trump will push for the best deal possible with Iran but will not prolong the war if it jeopardizes the global economy. However, it is not that simple. Should Iran continue to refuse to surrender or dilute its enriched uranium stockpiles—a sine qua non for U.S. negotiators—President Trump will need to choose between tightening sanctions and imposing more economic pain on Iran that will take time to produce its intended results, or resuming hostilities, which would provoke Iranian retaliation on its Gulf neighbors’ key energy assets and could widen the conflict regionally.

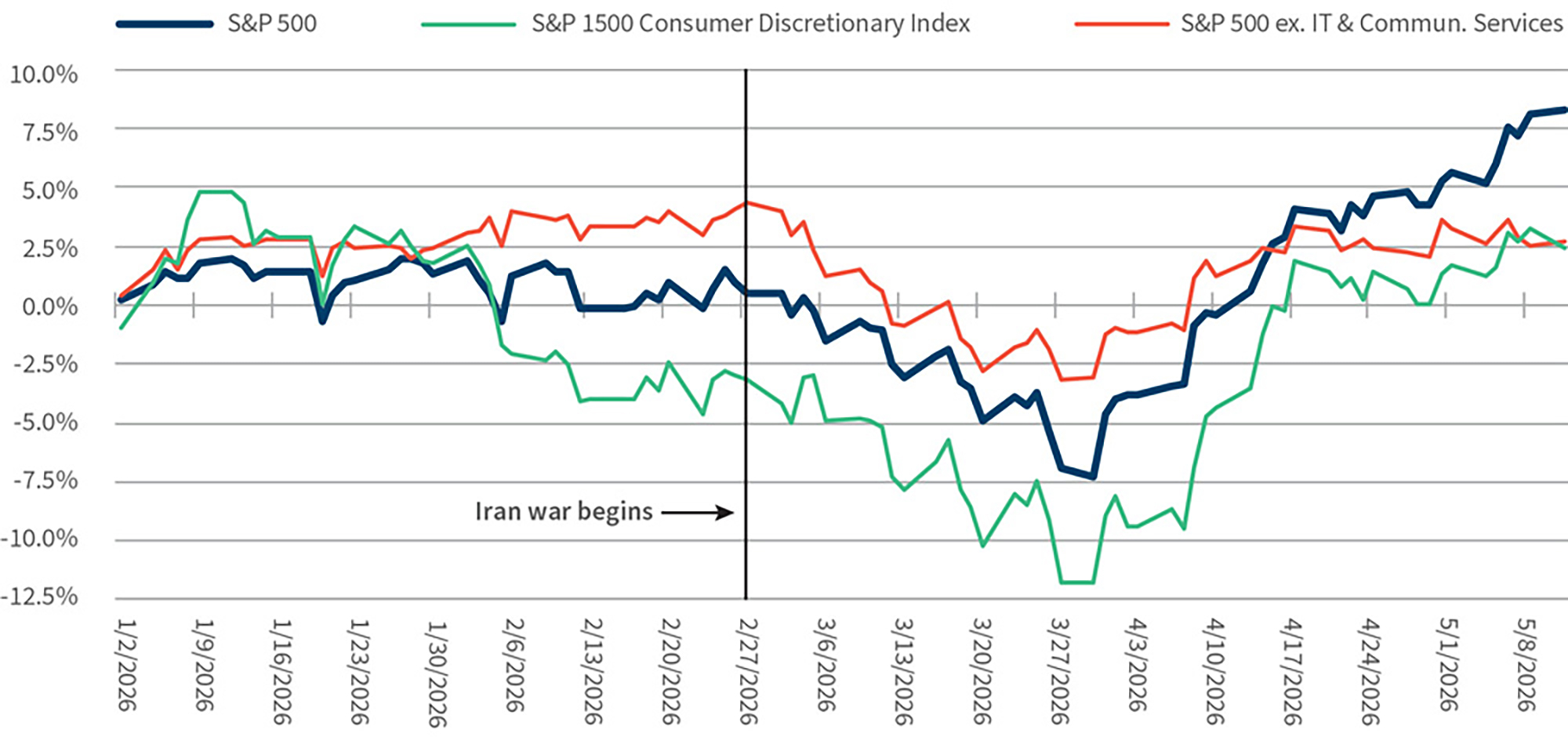

Following a sharp selloff in the early weeks of the war, major market indexes recently have rallied to record highs. This rally has been led by the AI and tech-related sectors, but S&P indexes that exclude the tech sector have also registered solid gains since bottoming in late March (Figure 2). Most major market indexes and valuation multiples are at record highs amid a tense and fragile geopolitical climate. Leveraged credit markets have been more circumspect than equities but also have rallied since the end of March despite lingering concerns about private credit lending and high exposure to the software sector, with overall issuance volumes improving notably in April from a month earlier. The leveraged M&A market, though hardly robust, is sufficiently active. The quantity of stressed and distressed corporate debt, whether measured by number or dollar volume, remains surprisingly tame while corporate debt default rates are not concerningly high. Given the tumultuous geopolitical events that have rocked the global order since January, the performance of financial markets to date in 2026 is nothing short of remarkable.

Figure 2 - S&P Index Returns: YT

Source: Bloomberg

The Great Consumer Divide: “Average Joe” Struggles To Fill the Gas Tank, While Airlines Prep for Record Summer Travel if They Don’t Run Out of Jet Fuel

It is the strangest of economic times. Financial markets have been disconnected from “the real economy” ever since the COVID-19 pandemic but we seem to be at a point of peak disconnectedness from ground level events. The juxtaposition of financial market rallies and extreme bullish sentiment by the investment community contrasted against a steady stream of news media stories about “pain at the pump” and hard choices facing many consumers, featuring firsthand accounts of the mounting financial hardship3 that many Americans are experiencing in 2026, especially since the war began, is hard to miss. Market indices are making all-time highs while the University of Michigan’s Index of Consumer Sentiment just registered its lowest reading since 1978.

Higher gas prices since March have impacted lower income households disproportionately, with current prices at the pump draining combustion engine vehicle-owning households of an additional $100 monthly, a considerable amount that is sending modest earners scrambling to offset where possible. The timing of the jump in gas prices was fortuitous for many struggling households as it coincided with tax refund season, but it has eaten into that windfall and eroded the financial reprieve that they were counting on. Moreover, record-high diesel prices will be further impacting retail prices of consumer products shipped by truck—a double whammy for strained shoppers.

First quarter earnings results and commentary from many consumer-driven businesses have prominently mentioned the negative impacts of spending cutbacks and trade-downs by hard-pressed shoppers since the war began. Earnings for most consumer-facing businesses held up reasonably well in 1Q26 as notable spending adjustments didn’t begin until mid-March, but many earnings calls have cautioned about an accelerating spending pullback in April and May. In discussing Whirlpool Corporation’s disappointing first-quarter results that saw its stock price hit a 15-year low, CEO Marc Bitzer commented, “The U.S. appliance industry demand declined 7.4% in the first quarter, with March being down 10%. This level of industry decline is similar to what we have observed during the global financial crisis and even higher than during other recessionary periods.”4 Similarly, Zoetis, a leading maker of animal and pet pharmaceuticals, registered its biggest weekly price decline ever after announcing 1Q26 U.S. sales unexpectedly fell 8% (YoY) and lowering 2026 earnings guidance, citing a challenging operating environment and commenting that, “…pet owners demonstrated increased price sensitivity, resulting in a decline in veterinary visits and softer demand for premium innovative products.”5 (You know times aren’t good when consumers start cutting back on their pet spending.) Several fast-food chains, including McDonalds, also have provided cautious outlooks for slower consumer spending in the months ahead combined with rising product costs. The underlying message signaled by various retail executives is that sales weakness in 2Q26 very likely will be worse than 1Q26 if current economic conditions persist. This could be the start of the most challenging period in years for consumer discretionary businesses whose customers are non-affluent households.

As we have pointed out several times since 2023, the U.S. consumer economy is not as healthy as it is often portrayed in business media, notwithstanding positive retail sales growth overall. Seemingly endless references to “the resilient U.S. consumer” is a misleading characterization of a fictitious “average shopper” based on aggregated spending data that conceals what is going on beneath the surface. The “K-shaped” consumer economy so often referenced in business media attempts to visually convey the breakdown of income and spending disparities but misses some critical context. The upper diagonal of the “K” represents the top quartile of income earners who are propelling the consumer spending engine more than ever, while the bottom diagonal of the “K” represents a large majority of households who are stagnating or falling behind. Recently, there have been references to an “E-shaped” consumer economy6 that better illustrates these starkly different and highly fragmented spending patterns, and perhaps it is a more fitting depiction of the times.

Restructuring Activity—Still Waiting for the Action

It is too soon to expect any fallout from high energy prices and disrupted supply chains to make its way into elevated corporate distress and restructuring activity, but give it some time. The consumer products sector leads all industry sectors in potential credit rating downgrades per S&P and also topped S&P’s list of Weakest Links (B- or lower rating with negative outlook or under review for possible downgrade) through March. Retailers, consumer services and consumer finance companies also are exposed to weaker spending as more Americans are forced to make difficult spending and payment choices as the reality of higher prices for longer sets in. April saw a meaningful jump in consumer-level inflation, and the prospects for a Fed rate cut this year now seem remote. It was an uneventful first quarter for restructuring activity of any kind—in or out of court—but the balance of the year holds more promise.

Footnotes:

1: Hjelmgaard, Kim & Swapna Venugopal Ramaswamy, “Iran Won’t Give Up Enriching Uranium to Get Peace Deal, Official Says”, USA Today (Apr. 15, 2026).

2: Norman, Laurence, “Iran’s Nuclear Program Has Survived, Posing Problem for U.S. Negotiators,” The Wall Street Journal (Apr. 12, 2026).

3: Cowley, Stacy, “Consumers Lean on a “Hamster Wheel” of Credit to Manage Rising Costs,” The New York Times (May 10, 2026).

4: Whirlpool Corporation, Q1 2026 Earnings Call (May 7, 2026), S&P Capital IQ.

5: Singh, Vandana, “U.S. Pet Care Demand is Weak—Zoetis Cuts Outlook,” Benzinga (May 7, 2026).

6: Blasi, Weston, “What's an ‘E-shaped’ economy — and where do you fit in it?” MarketWatch (Apr. 4, 2026).

Related Insights

Related Information

Published

May 28, 2026

Key Contacts

Key Contacts

Global Chairman of Corporate Finance