UK Competition Enforcement, Public and Private

-

April 10, 2026

-

Introduction

Almost ten years ago, the UK National Audit Office’s report on the establishment of the Competition and Markets Authority (“CMA”) was published. The report was wide-ranging, but perhaps its key criticism of the UK competition regime to that date was the limited extent of competition enforcement. The report concluded that “[t]he CMA and the regulators are acting to improve the detection of anti-competitive behaviour and to build a pipeline of cases, but the system has so far failed to produce a substantial flow of enforcement decisions.”1

How has public competition enforcement in the UK evolved over the past decade and what does that mean for the future of private enforcement?2

The History of Public Competition Enforcement in the UK

The UK has long had a highly-regarded competition regime. The 2024 Global Competition Review gave it a five-star rating and stated that “[t]he UK’s Competition and Markets Authority (CMA) is one of the world’s most important, influential and – whisper it – feared antitrust enforcers… At a time when other UK regulators are facing heat for missteps and other perceived failings, the CMA’s leadership has steered the agency to the front of the pack on the international stage.”3 Similar statements could have been made at almost any time since the 1998 Competition Act came into force in March 2000. For instance, in its 2010 report on the competition landscape, the NAO noted that “ratings in the Global Competition Review … show that the UK’s Office of Fair Trading and Competition Commission are globally recognised as amongst the leading authorities.”4

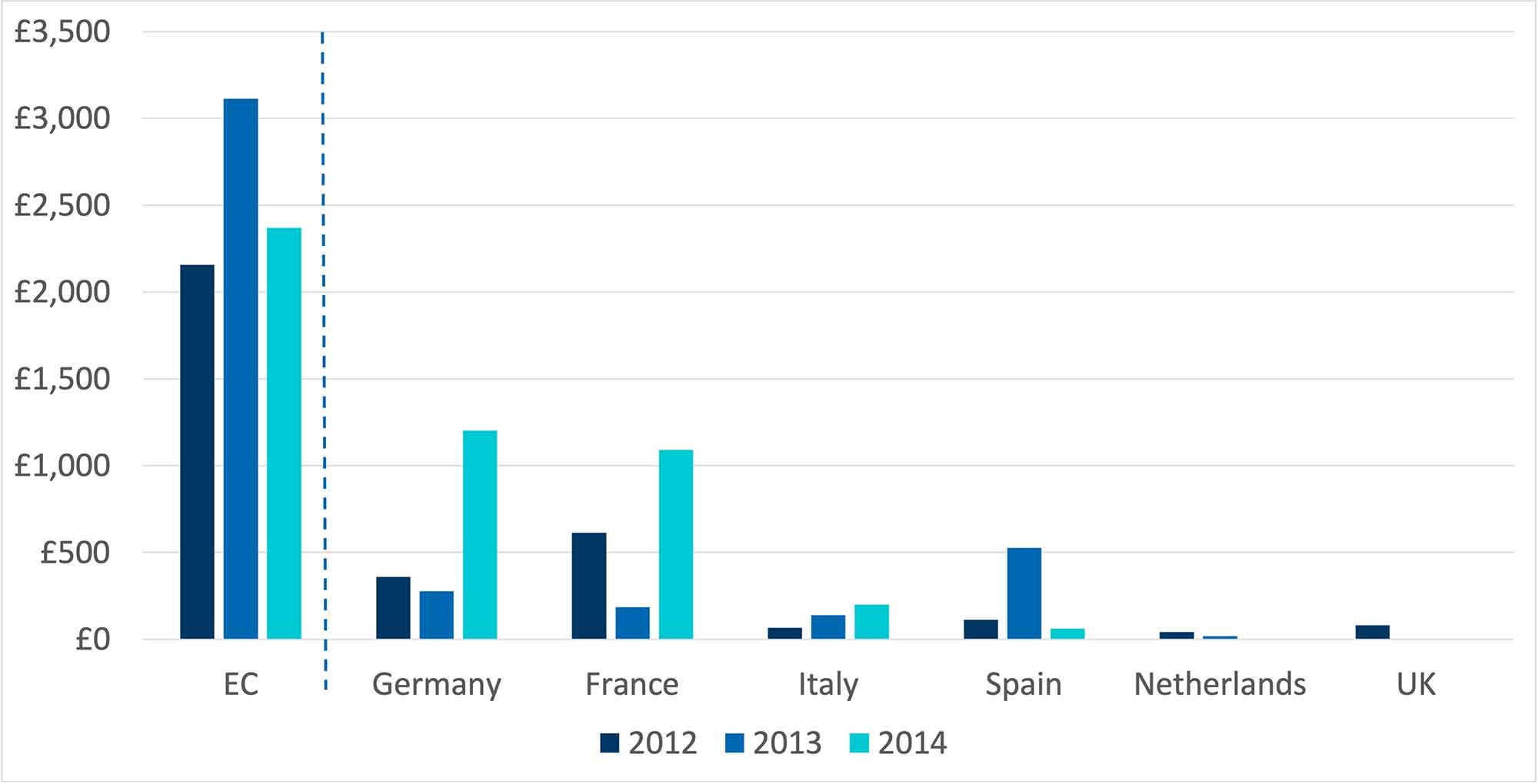

The quality of the UK’s work on collusion and abuse of dominance cases (CA98 Chapter I and Chapter II cases) is also generally well-regarded. However, the scale of this work has been well below that in comparator regimes. In its 2016 report, the NAO found that “[t]he flow rate of cases has not increased since our 2010 report, remaining at around four per year at the primary competition authority, with no infringement decisions by the regulators… In 2014, the German competition authorities concluded nearly six times as many cases than their UK counterparts, and the French competition authorities four times as many…, despite similar levels of resourcing for enforcement work and similar-size economies.”5 Fines were also much lower (Figure 1).

Figure 1: Fines Imposed by Selected National European Competition Authorities and the European Commission From 2012 to 2014 (Millions, Adjusted to 2024 Prices)6,7

Notes:

The reasons for these differences were widely-discussed, with no clear consensus – possible explanations we heard included the lack of statutory deadlines for enforcement cases, the lower profile of enforcement work relative to mergers and market investigations and a higher standard of proof in the UK than in comparator jurisdictions.8 Nonetheless, there was general agreement that the CMA should increase the flow of enforcement decisions, with help from its sponsor department to the extent that doing so was impeded by legislative or institutional barriers. Indeed, improving competition enforcement had been an important driver of the establishment of the CMA – the government stated that it aimed to encourage long-term growth by “streamlining and strengthening the competition tools to address anticompetitive behaviour.”9

Recent Developments in Public Enforcement

This section updated the analysis the NAO carried out on enforcement cases and fines using more recent data. Though this current approach differs from the NAO’s in several respects. First, given the more limited powers and resources, the analysis relies mainly on annual reports by national competition authorities. While different data sources are not entirely consistent, the broad trends appear similar across datasets.

Second, the analysis is based on authorities’ decisions does not account for whether a decision was ultimately overturned on appeal. To the extent that decisions were regularly overturned, the figures presented here would tend to overstate the deterrent effect of their enforcement activities. In relation to fines, different authorities appear to adopt different approaches as to whether to include fines for decisions which are under appeal – France and the UK, for instance, do not do so.

Finally when considering the UK, the analysis focuses on cases brought by the CMA, and do not include cases brought by those UK sector regulators that have concurrent competition enforcement powers. However, the number of infringement decisions they make is limited and including them would not significantly change the qualitative messages.

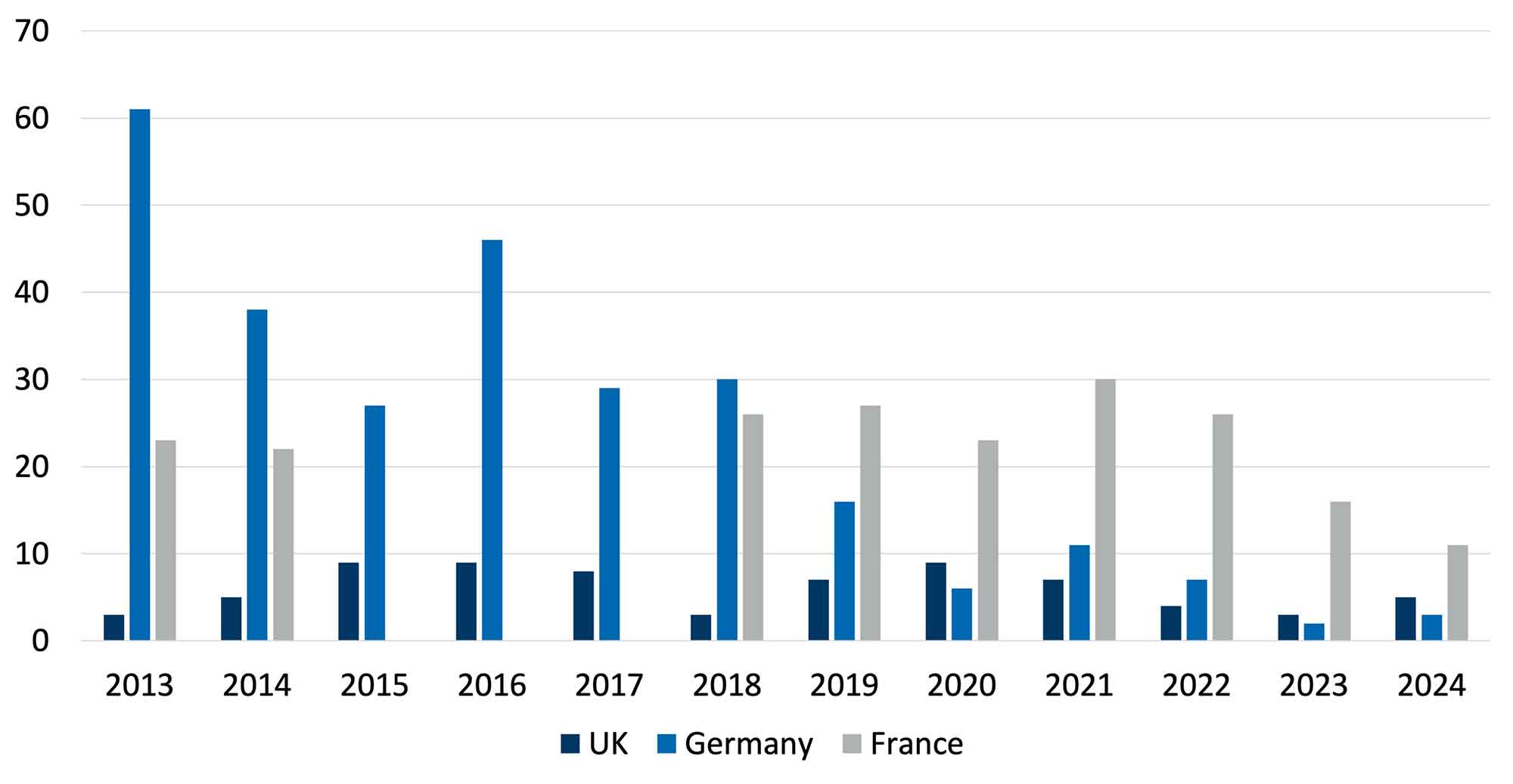

Figure 2 shows the enforcement case decisions by major western European competition authorities between 2013 and 2024. UK enforcement decisions have not increased markedly, but there has been some narrowing of the gap to Germany and France, particularly due to a significant decrease in the number of decisions issued by the German competition agency.

Figure 2: Enforcement Decisions by Selected National European Competition Authorities From 2013 to 202410,11

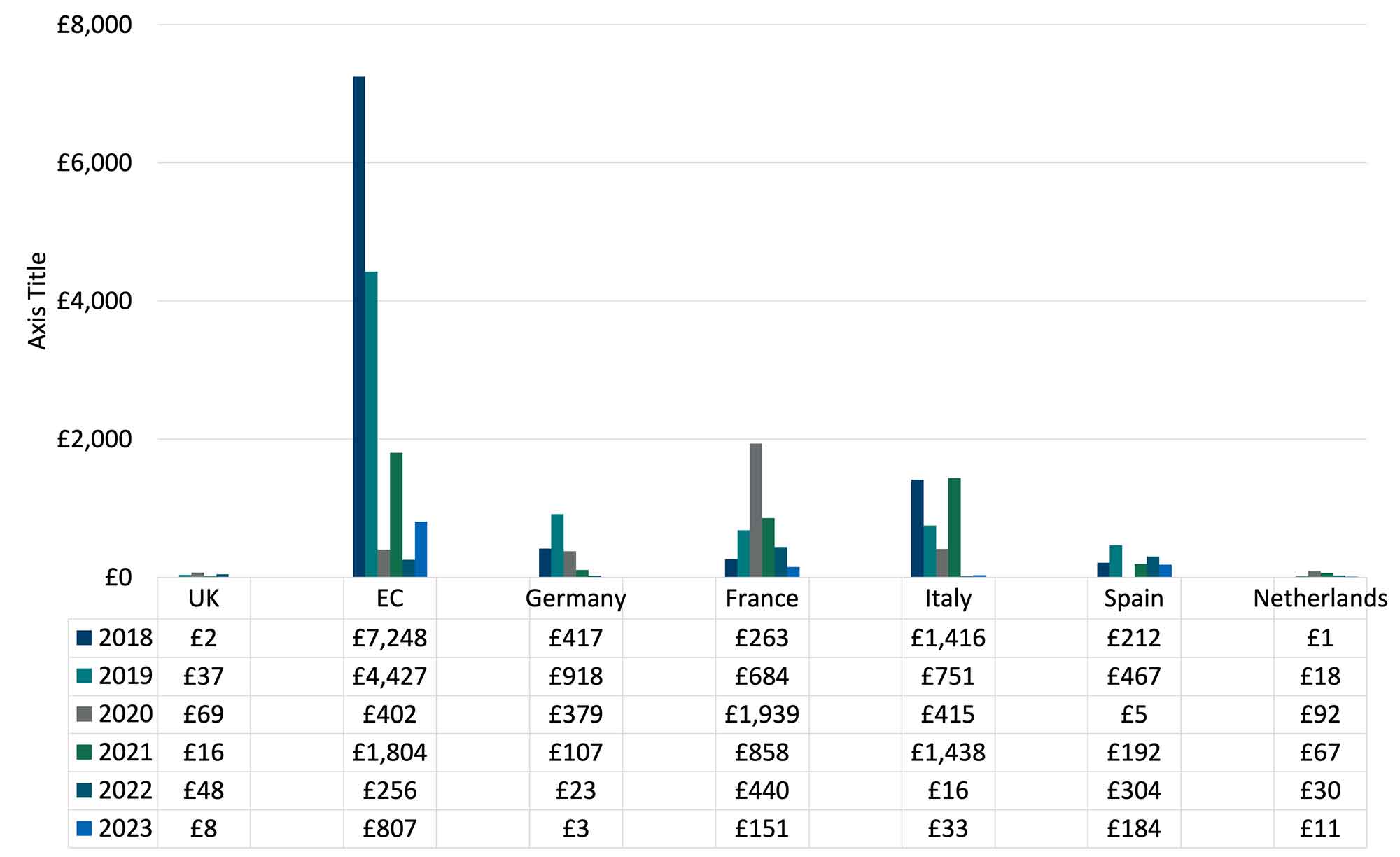

Figure 3 shows the fines levied by the UK, the EC and five leading European competition authorities between 2018 and 2023. Fines issued by the UK were significantly below those of comparators. For instance, the UK issued £180 million of fines over this period, compared to over £4 billion by the French and Italian competition authorities.

Figure 3: Fines and Penalties Issued by Selected National European Competition Authorities and the European Commission From 2018 to 2023 (Millions, Adjusted to 2024 Prices)12, 13

Overall, there are some positive developments in the UK compared to the picture in 2016. The number of enforcement decisions relative to comparator jurisdictions has increased. The level of fines is still well below that in most comparators, less than one twentieth of the fines levied in France, but the gap may close somewhat once cases currently under appeal are included. This growth in public enforcement is welcome, but it is perhaps too optimistic to assume that all problems have been solved. In particular, most of the period considered is after the UK’s exit from the European Union. Other things equal, we might expect the UK to bring a significant proportion of the cases that the EC runs, as well as the national cases as before, but this does not seem to have happened. EC fines alone are around 80 times those in the UK over this time period.

Without being close enough to the operation of public enforcement to have strong views on how the flow of decisions and fines could be increased further, though its likely that several of the same factors we identified in 2016 are still relevant. However, it is in any case important to consider the interaction between public and private enforcement in judging the successes or failures of the latter.

Private Enforcement

The UK government recently issued a call for evidence on the collective action regime for private competition enforcement.14 The direction of travel appears to be to try to reduce the number and scale of collective actions. This would be a mistake, particularly because of the interaction between public and private enforcement.

The limited historical scale and size of public enforcement in the UK, relative to comparators, has three key implications for private enforcement:

- First, standalone cases are inevitably more common than follow-on cases. There have been relatively few public enforcement cases from which to follow on. In particular, the CMA has not issued any cartel or abuse of dominance fines against the largest digital firms. This is in marked contrast both to the EC and to European competition authorities, where total competition-related fines since 2019 for these firms were over €11 billion.15 While it may be the case that the UK’s approach is right and the European authorities’ wrong (or that the factual background differs between the jurisdictions), it should not be surprising that private practitioners in the UK have looked across the Channel to bring cases that are similar in nature to those that public authorities have brought in the EU.

- Second, cases so far have been more expensive than was initially expected. Standalone cases, where claimants have to show both liability and damages, will typically be more expensive than follow-on cases. The level of disclosure and evidence-gathering will be greater, and a wider range of potential arguments and theories of harm will need to be considered. Moreover, the limited precedent means that there is more uncertainty about which economic or other expert methodologies are likely to be regarded favourably by courts, again encouraging experimentation and increasing costs.

- Third, uncertainty about the boundaries of the law means that claimants have brought forward some cases that might be considered speculative. On the flipside, defendant firms may be reluctant to settle in a context where they can reasonably believe that they have a good chance of success. Both of these factors are likely to increase the costs of the regime relative to a situation with more public enforcement decisions and thus more settled case law. Moreover, they suggest that there are likely to be substantial benefits, to defendants, claimants and public authorities, from building a body of case law through private enforcement cases.

After many years in which authorities, practitioners and politicians talked frequently about the need for more private competition enforcement in the UK, but with very little action, the last few years have seen a dramatic increase in the number of cases, particularly through collective actions.16 It seems that policymakers are now experiencing buyer’s remorse, with suggestions that the government will try to reduce claimants’ ability to bring collective actions in future.

This would be at best highly premature. Few of the recent private enforcement cases have yet been determined (or settled), meaning that the boundaries of the law and thus the likely success of different types of case remain uncertain. Given that public enforcement remains limited, there are serious risks that reducing the scope for private enforcement would entrench under-enforcement of competition law in the UK.

Footnotes:

1: “The UK Competition Regime,” National Audit Office (February 2016), (last accessed 22/09/2025), paragraph 21.

2: “Opt-Out Collective Actions Regime Review: Call for Evidence,” Department for Business and Trade (August 2025), (last accessed 22/09/2025).

3: “United Kingdom's Competition and Markets Authority,” Global Competition Review (2024), (last accessed 22/09/2025).

4: “The UK Competition Landscape,” National Audit Office (March 2010), (last accessed 22/09/2025).

5: “The UK Competition Regime,” National Audit Office (February 2016), (last accessed 22/09/2025), paragraph 21.

6: Fines for Spain in 2013 cover the period from 1 September 2012 to 30 September 2013. In addition, the UK imposed £1.1 million of fines (after settlement) in 2015, meaning that total fines were £66 million between 2012 and 2015 in 2015 prices. All fines, other than for the UK, have been changed from euros to sterling using an average exchange rate for each year. Figures were converted from 2015 prices to 2024 prices using CPIH data.

7: “The UK competition regime” NAO (February 5, 2016): at Figure 14 (last accessed 22/09/2025).

8: “The UK Competition Regime,” National Audit Office (February 2016), (last accessed 22/09/2025), paragraph 2.15. Note One stakeholder made the striking statement that “the UK was the best jurisdiction in the world to defend a competition case”.

9: “Enterprise and Regulatory Reform Act 2013: Policy Paper,” Department for Business Innovation and Skills (June 2013), (last accessed 22/09/2025).

10: French concluded cases include “Litigation decisions (Anticompetitive practices)” issued by the French Competition Authority. German concluded cases include the "number of proceedings" which were concluded in Abuse control and cartel cases. UK figures for competition enforcement are based on the number of Competition Act investigations and do not incorporate investigations into consumer protection issues In some cases the total number of concluded cases was not reported and had to be estimated based on disaggregated data. Missing data for France in 2015-2017 indicates that the competition authorities' annual reports did not detail the number of concluded competition enforcement cases.

11: UK, 2022–2024: “CA98 and Civil Cartels” and “Criminal Cartels,” Competition and Markets Authority.

2015–2021: Competition and Markets Authority Annual Reports, Competition and Markets Authority.

France, 2017–2024: Annual Reports, Autorité de la Concurrence.

Germany, 2015–2024: Cartel cases: “German Competition Authority Cartel Cases,” Lexology.

Abuse of dominance cases: Annual Reports, Bundeskartellamt.

2013–2014: “The UK Competition Regime,” National Audit Office, Figure 13.

12: Fines by the UK and France Competition Authorities include total fines and penalties (including e.g., fines for obstructing an investigation); fines by the EC relate to competition fines; fines by the German Competition Authority include fines on cartels; the type of fines by the Italian Competition Authority depends on the available information; fines by the Spanish Competition Authority include competition-related fines; fines for the Netherlands Competition Authority include newly imposed fines across multiple sectors e.g., competition, healthcare, consumer protection and transport.

All fines, other than for the UK, have been converted from EUR to GBP using annual average ECB exchange rates. They are then converted to 2024 prices using CPIH based on ONS data.

UK: the CMA does not recognise fines for cases which are under appeal. Several significant fines have not yet been recognised, for instance in relation to abuse of dominance in the pharmaceutical sector.

European Commission: fines relate to fines on companies for breaches of EU competition rules and do not include fines on member states for infringements of EU law.

France: fine amounts include outcomes after appeal. The fines for 2023 and 2024 do not incorporate the outcome of appeals that have been filed against certain decisions in the French Supreme Court and the Court of Appeal (judgments unavailable at the closing date of the publication).

Italy: Fine amounts are based on estimates as the annual reports do not detail the total amount of fines but only include information on some of the fines imposed. Fines for 2018 include fines from January 2018 until June 2019.

13: UK: “Annual Accounts and Reports,” Competition and Markets Authority.

European Commission: “Consolidated Annual Accounts of the European Union,” European Commission.

Germany: “Annual Reports,” Bundeskartellamt.

France: “Annual Reports,” Autorité de la Concurrence.

Italy: “Annual Report,” Autorità Garante della Concorrenza e del Mercato.

Spain: “Annual Report CNMC 2023,” Comisión Nacional de los Mercados y la Competencia.

Netherlands: “Annual Reports,” Autoriteit Consument & Markt

14: “Opt-Out Collective Actions Regime Review: Call for Evidence,” Department for Business and Trade (August 2025),(last accessed 22/09/2025).

15: Calculated based on manual research of fines imposed since 2019. Figure may be understated due to potential omissions. This does not include successfully appealed fines or non-competition related fines.

16: Hourigan and Perkins, “Data and Damages in Digital Economy Class Actions,” LIDW (July 2025), (last accessed 14/10/2025).

Related Information

Published

April 10, 2026

Key Contacts

Key Contacts

Senior Managing Director