Deals in Motion

How Investment Bankers View the 2026 M&A Market Shaping Up

-

June 15, 2026

Downloads Download Article

Download Article

-

As we move through the second quarter of 2026, investment bankers are signaling a meaningful shift in market sentiment. According to FTI Consulting’s latest survey of leading investment bankers across sectors, deal activity has accelerated from where it stood a year ago, and forward-looking confidence is even stronger. Whereas 2025 was defined by caution and selective engagement, 2026 is showing signs of broader re-engagement, with bankers reporting improved access to financing, a more constructive regulatory environment and growing pressure to deploy capital that has sat on the sidelines.

The shift is not uniform, as sector-specific dynamics, including tariff exposure, AI disruption and regulatory transition, continue to create divergent conditions. But the overall direction is clear: the market is moving, and most bankers expect that momentum to hold or build over the next three-to-six months. While completed deal volumes in early 2026 have remained selective, banker sentiment points in one direction, and most expect that to translate into accelerating activity through the remainder of the year.

Sector Views | A Broader Recovery, With Notable Exceptions

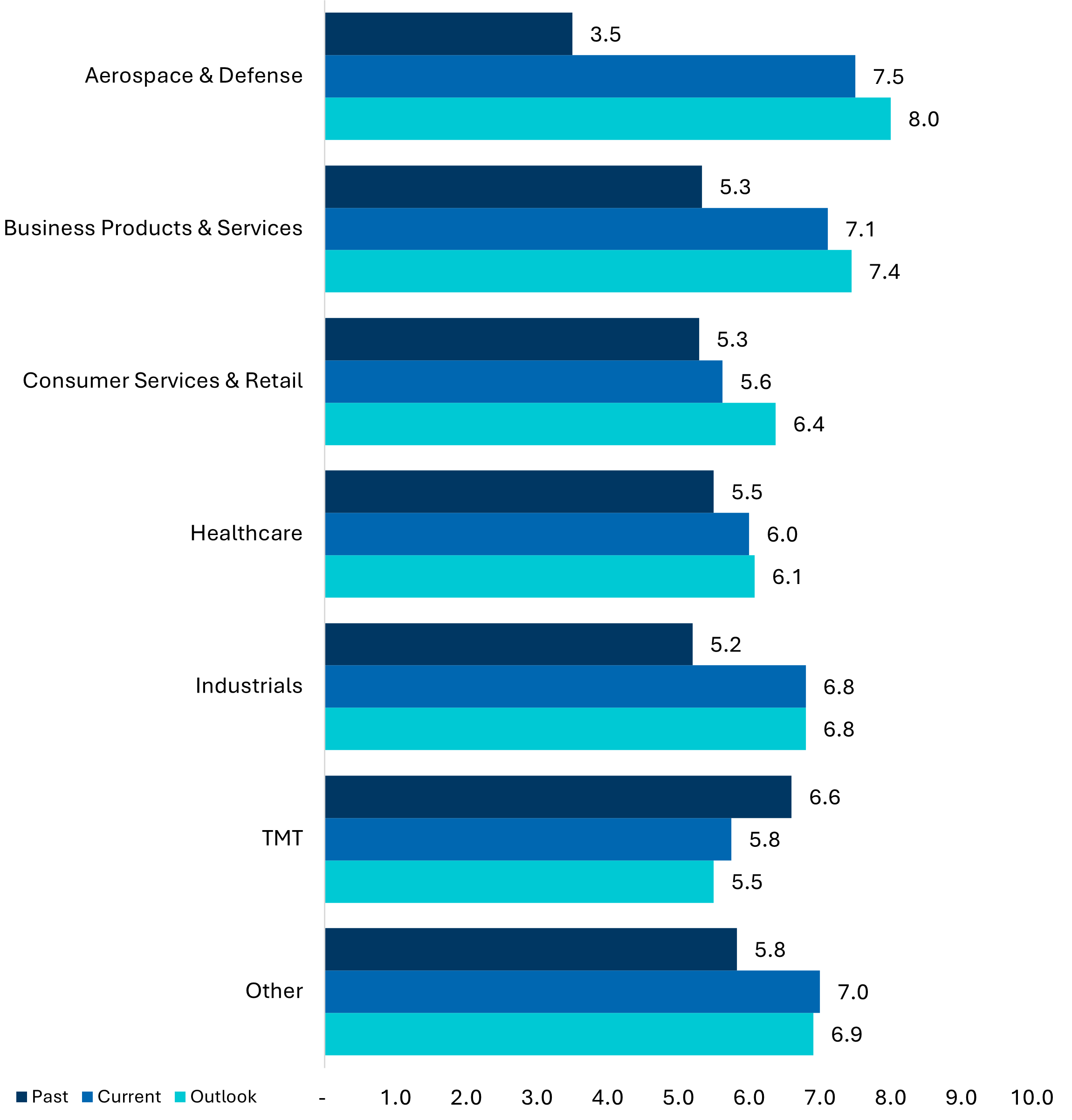

Investment bankers report improved conditions across most sectors, with Aerospace & Defense, Business Products & Services and Industrials showing the most significant upward movement, while Healthcare and Consumer Services & Retail are also trending in the right direction. Telecom, Media & Technology (“TMT”) is the notable exception, where sentiment has moderated from elevated levels. Across the board, bankers note that deal committees are becoming less reactive to macro noise and more focused on long-term strategic fit and asset quality.

Aerospace & Defense — This represented the most dramatic recovery in this year’s survey. After rating current activity at just 3.5 in 2025, bankers now rate the sector at 7.5, with a three-to-six-month outlook of 8.0. Improved regulatory clarity, stronger defense budgets and renewed access to financing have all contributed to a more active deal environment. Respondents indicate that deal processes that were paused or delayed are now moving forward.

Business Products & Services — Sentiment continues to build on the momentum observed as we entered 2025. Current activity is rated at 7.1, up from 5.3 last year, with a forward-looking score of 7.4. Automation, cloud infrastructure and technology-enabled services remain focal points for both strategic and financial sponsors, with AI integration increasingly influencing how acquirers assess value and scalability.

Consumer Services & Retail — Conditions have improved modestly, with current activity rated at 5.6, up from 5.3 in 2025. The three-to-six-month outlook of 6.4 reflects cautious optimism as tariff-driven uncertainty eases in select categories. High-quality assets continue to command premium valuations, and financial sponsors with meaningful dry powder are increasingly active in identifying entry points.

Healthcare — The sector remains measured, with current activity rated at 6.0 and a forward outlook of 6.1. Respondents note that regulatory transition concerns that weighed on 2025 activity have begun to ease, though investor hesitancy around reimbursement risk and policy visibility persists. Consumer health platforms continue to attract the most consistent deal interest.

Industrials — Current activity is rated at 6.8, up from 5.2 in 2025, while the forward outlook remains at 6.8. Bankers report that while tariff-driven uncertainty has not fully resolved, buyers and sellers have become more adept at pricing risk into transaction structures. Carve-outs, PE-driven processes and businesses with strong domestic manufacturing positioning are leading deal flow.

TMT — The only sector where sentiment has pulled back, with current activity rated at 5.8 versus 6.6 in 2025, and a forward outlook of 5.5. Bankers attribute the moderation to sustained valuation pressure in software, ongoing interest-rate sensitivity and a recalibration of AI-driven growth expectations. That said, infrastructure-scale transactions, particularly in data centers and connectivity, continue to attract strong interest from both strategic and financial buyers.

Rating Scores | Confidence Is Building

Overall sentiment among investment bankers has improved substantially heading into mid-2026. Excluding TMT, every sector posted higher current activity scores relative to 2025, and forward-looking outlook scores exceed current activity in five of seven sectors, a meaningful signal that bankers expect conditions to continue improving.

Aerospace & Defense shows the largest year-over-year gain, rising more than four points on current activity. Business Products & Services and Industrials also reflect strong upward movement, while Healthcare and Consumer Services & Retail, while still measured, are trending in the right direction.

Aerospace & Defence

Source: Expert interviews

(0 = No activity, 10 = Extremely active | Past refers to ratings as of May 2025. Current refers to ratings as of May 2026. The rating scores are averaged from all respondents, and the sample size for each sector varies.)

Integrated Advisory | Bankers Signal Clear Preference for Coordination

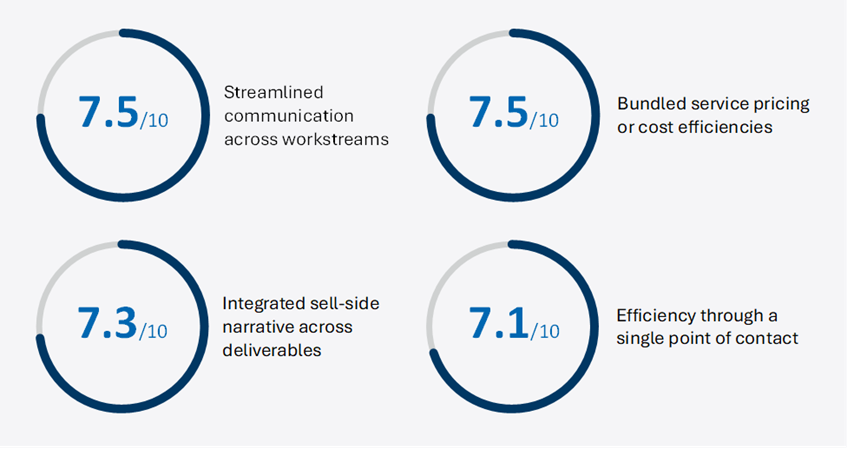

This year’s survey also asked bankers to weigh in on the value of an integrated “one-stop shop” advisory model in sell-side processes; one that brings together financial, commercial, operational, tax, HR/benefits and IT diligence under a single advisory relationship.

The results are consistent and clear: across all four dimensions, bankers rated the value of integration at 7.1 or higher on a 10-point scale.

Source: Expert interviews

Streamlined communication and bundled pricing tied for the highest scores, reflecting that bankers see integration as delivering value on two equally important fronts: process quality and cost. The communication finding reflects the practical reality that sell-side processes are often derailed by coordination failures across workstreams rather than by the quality of any individual work product. Bankers noted that a fragmented advisor model creates friction for management teams and can introduce inconsistencies that sophisticated buyers will uncover in diligence.

That bundled pricing ranked equally high signals something important: in a market where sellers are increasingly focused on maximizing proceeds and managing transaction costs, cost consolidation is not a secondary consideration. The ability to consolidate advisory fees without sacrificing quality is a tangible differentiator.

The strength of these scores across all four dimensions reinforces a consistent theme: bankers see real value in advisory relationships that can hold a coherent sell-side story together from preparation through close, rather than stitching a narrative across multiple, disconnected providers. For a deeper look at how integrated diligence models are reshaping transaction outcomes for buyers and sellers, see our recent article, The Strategic Advantage of Integrated Due Diligence in M&A.

Related Information

Published

June 15, 2026