Global Aviation Themes 2026

Key Trends Shaping the Industry’s Next Phase

-

March 27, 2026

Downloads Download Article

Download Article

-

This article was prepared prior to the recent conflicts in the Middle East. The views and projections expressed herein do not incorporate scenarios arising from the resultant impact on the aviation industry and may be subject to revision as conditions evolve.

The industry is moving beyond the post-pandemic rebound and settling into a more demanding operating environment, where costs are higher and conditions are tighter than in previous years.

The defining characteristic of this cycle is that margin pressure is not primarily demand-driven. Load factors are healthy across many markets and premium leisure travel remains supportive. Yet cost inflation, labor dynamics and supply chain fragility are reshaping the economics of the sector in a more permanent way.

Maintenance costs have increased structurally as fleets age and engine shop capacity remains constrained. Labor agreements signed over the past several years have raised wage floors across key markets. Higher interest rates have lifted cash break-even thresholds and reduced financial flexibility. In many cases, pricing power has proven insufficient to fully offset these pressures, forcing operators to rethink network design, fleet strategy and operating models rather than rely on incremental cost controls.

Sustainability remains a strategic priority, but the tone is shifting. Regulatory mandates, SAF requirements and emissions frameworks continue to shape airline agendas, yet stable fuel costs, limited Sustainable Aviation Fuel (“SAF”) availability and shifting political winds are forcing a more pragmatic approach.

Running in parallel, the aviation industry must consider how best to integrate modern distribution technology and artificial intelligence (“AI”) advancements. Success will depend on companies adapting to a structurally higher cost base, ensuring operational resilience in tighter supply conditions and making thoughtful, disciplined investment decisions.

Cost Inflation Is Reshaping Profitability Across the Aviation Value Chain

Cost inflation is now a structural feature of the aviation industry and will shape its economics for the foreseeable future. Maintenance costs continue to rise as fleets age, engine reliability issues persist and shop capacity remains constrained. Labor expenses have increased sharply following multi-year wage negotiations, while higher interest rates have materially raised cash break-even levels. At the same time, pricing power remains uneven across markets, leaving many operators unable to pass higher costs through to customers fully.1

These pressures are particularly challenging for airlines with limited scale, older fleets or weak balance sheets. In this cycle, margin compression is primarily the result of a structurally higher cost base that is unlikely to normalize in the near term. As a result, traditional short-term cost cutting is increasingly insufficient to restore financial resilience.

FTI Consulting Perspective

We expect a sustained increase in demand for performance improvement, cost transformation and selective restructuring work. This will be most pronounced among smaller regional airlines, leisure and low-cost carriers and tier-2/3 OEM suppliers with limited pricing leverage. Importantly, balance-sheet stress is increasingly translating into deeper operational and strategic intervention — covering fleet strategy, network design, labor models and vertical integration decisions — rather than isolated efficiency initiatives. The current wave of restructuring reflects the need to realign operating models with a cost environment that has structurally changed.

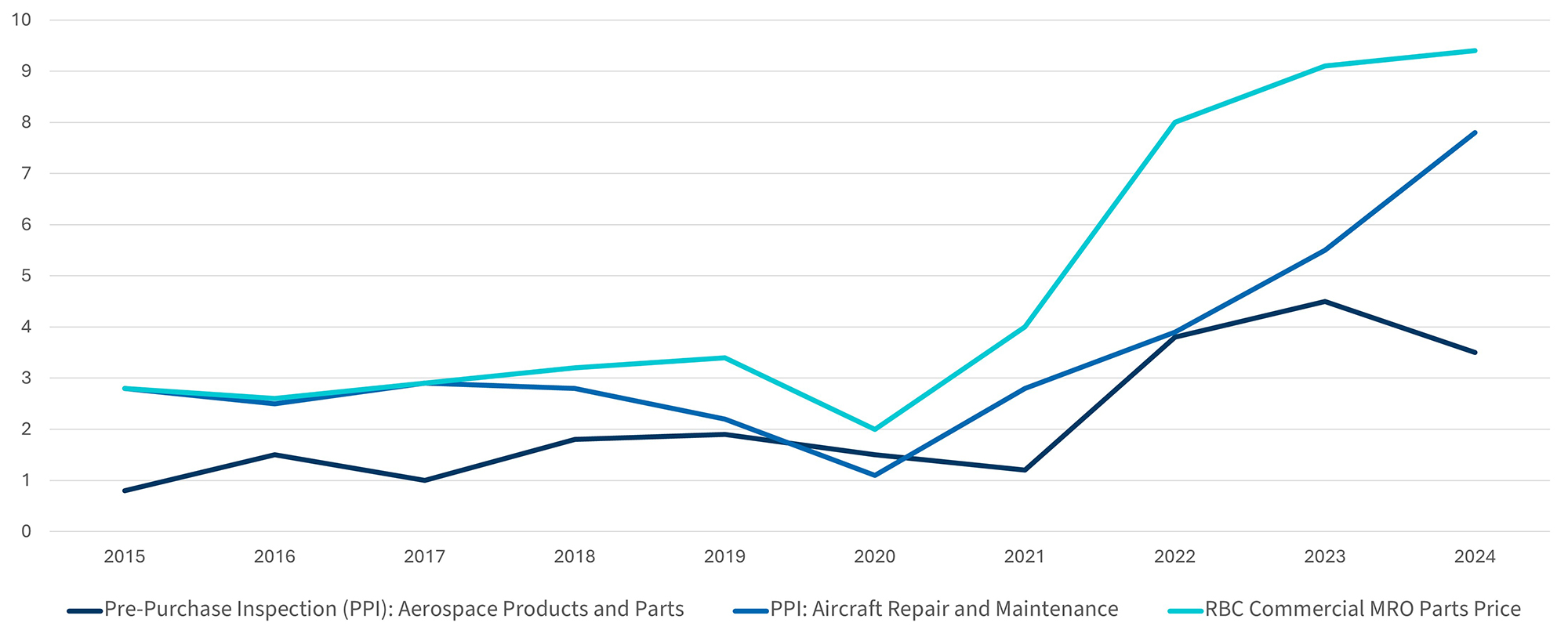

Figure 1 – Aerospace Parts Inflation Over Time, 2015–2024

Annual Percentage Change

Sources: St. Louis Federal Reserve, RBC Capital Markets MRO Survey Reviving the Commercial Aircraft Supply Chain, Iata Report, October 2025, Exhibit 27.

Aviation’s Workforce Challenge Is Becoming Structural

Even where airlines did not lay off or furlough staff during the pandemic, voluntary separations and attrition significantly reduced the pool of workers. When airlines rapidly rebuilt their schedules, the result was acute labor shortages, particularly for roles with long training horizons such as pilots and mechanics.

While pilot shortages dominated public discourse and contract negotiations resulted in substantial increases for labor, especially in the U.S. market, the urgency of the discussion has faded. Increased hiring and training volumes have caught up with slower growth. However, maintenance technicians remain in short supply.

FTI Consulting Perspective

- With the acute “pilot shortage” in the rear-view mirror, old but pressing arguments about the structural pilot deficit will re-emerge. Airlines, MROs and other aviation companies will refocus on supporting the long-term pipeline by investing in youth outreach, pilot training academies and partnerships with universities.

- The upcoming round of U.S. labor negotiations will be the hardest yet. Having received significant quality of life and wage rate improvements over the past five years, unions’ expectations are high, as are airline’s cost structures.

- Workforce strategy is now a core element of operational resilience and enterprise risk management. Those that fail to secure sustainable talent pipelines will face constraints on fleet utilization, network growth and service reliability, regardless of demand conditions. Effective workforce deployment will become increasingly important.

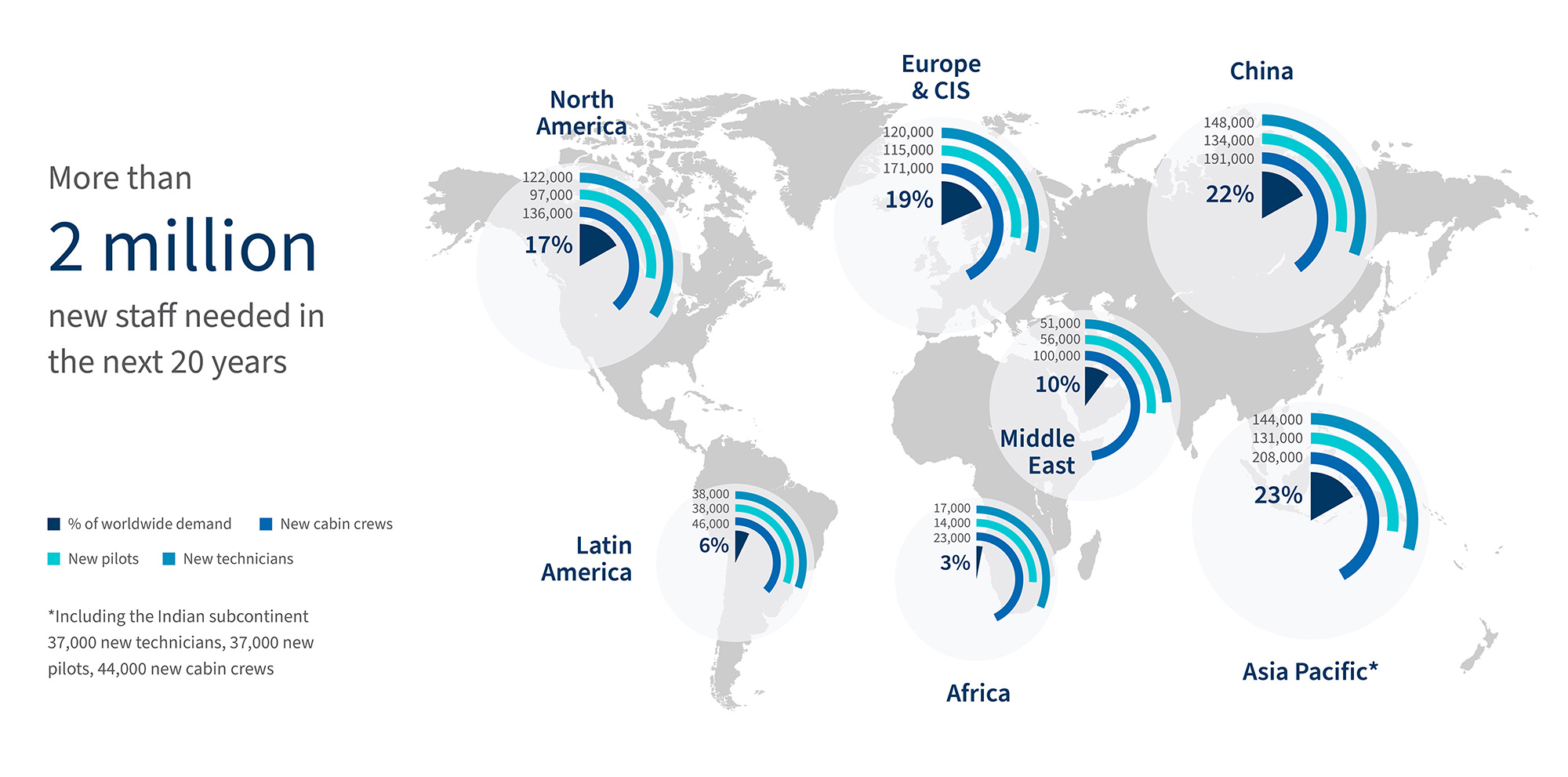

Figure 2 – Workforce Needs per Region

Sources: Airbus: Commercial aircraft services market to double in value by 2041, Pilot Careers News

Supply Chain Fragility Is No Longer Temporary

Supply chain disruption in aviation has evolved from a post-pandemic shock into a structural feature of the industry. Airframe and engine maintenance demand has surged due to pandemic-era deferrals, compounded by well-documented maturation challenges with next-generation GTF and LEAP engines. Raw material shortages and OEM bottlenecks are creating parts backlogs and leaving unfinished work occupying valuable shop floor space, while skilled labor gaps are expected to persist well into 2026 and beyond. These pressures combined are increasing maintenance event durations, driving higher costs and introducing greater uncertainty into fleet planning and operational forecasting.

The consequences are cascading across the ecosystem. Airlines face longer ground times and reduced schedule reliability, while lessors and investors are reassessing asset values and lease assumptions.2 What was once a tactical operational issue has become a strategic consideration shaping capital allocation and long-term planning.

FTI Consulting Perspective

Airlines must develop a more comprehensive understanding of fleet lifetime economics, incorporating fully loaded, scenario-based maintenance costs rather than relying on historical averages. MRO providers must reimagine their supply chain planning, building in more resilience to mitigate delays and customer expectations both.

This shift is reshaping decisions around fleet renewal, make-versus-buy MRO strategies, long-term contracting and alternative inventory models such as parts pooling and power-by-the-hour arrangements. As maintenance events, particularly engine overhauls, become more expensive and less predictable, traditional lifecycle assumptions are being fundamentally reconsidered, with implications for valuation, financing and restructuring decisions.

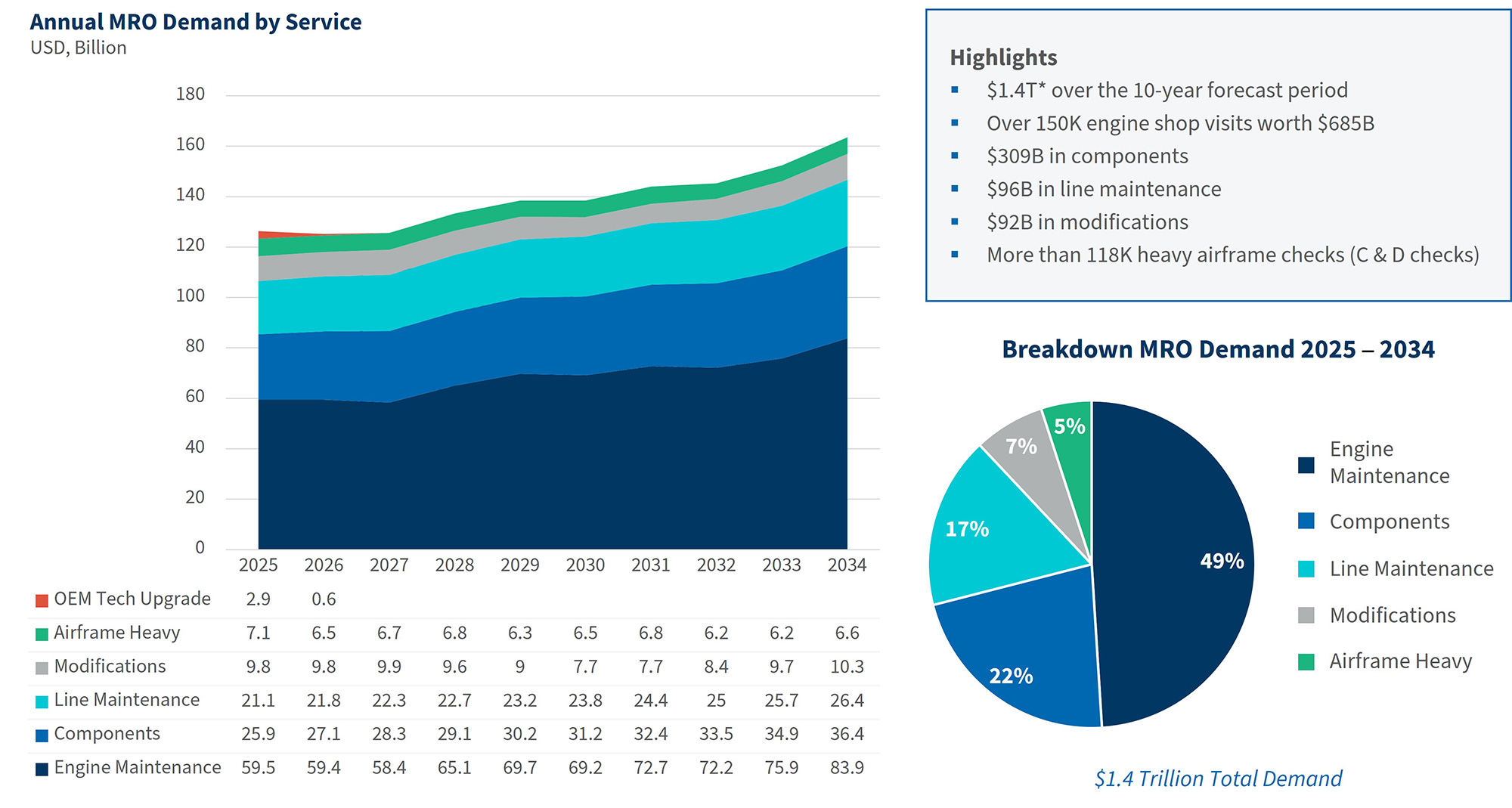

Figure 3 – Forecast MRO Demand Trends

Source: 2025 Commercial Aviation Fleet & MRO Forecast, Fleet Discovery, Aviation Week Network, Copyright 2024. Note: *2025/2026 engine technical upgrades/warranty repairs shown on chart only, not included in analysis nor CAGR figures. FTI Note: Though not shown here, we expect OEM Tech Upgrades to continue into the future.

Regional Airlines at a Turning Point

Regional airlines are under sustained pressure from multiple directions. Higher pilot costs, worsening supply chain issues, dependence on network carriers and shifting fleet economics are squeezing the traditional business model — particularly in the United States, the world’s largest regional market. At the same time, organic growth is limited by scope clauses and network carriers are reevaluating their regional strategies, favoring larger gauge aircraft and fewer partners.

The traditional regional airline model — built around high utilization of small aircraft and low labor costs — has become increasingly difficult to sustain. Scale, balance sheet strength and contractual positioning with major carriers are now critical differentiators.

FTI Consulting Perspective

Over the past 10 years the United States have seen the number of regional carriers shrink from ~15 to ~9. Further consolidation among regional airlines is likely, through mergers, asset combinations or market exits. Network redesigns and continued transitions away from 50-seat aircraft will continue, redefining the role of regionals within the broader airline ecosystem. For some operators, survival will depend on strategic repositioning; for others, consolidation may represent the most viable path to preserving value.

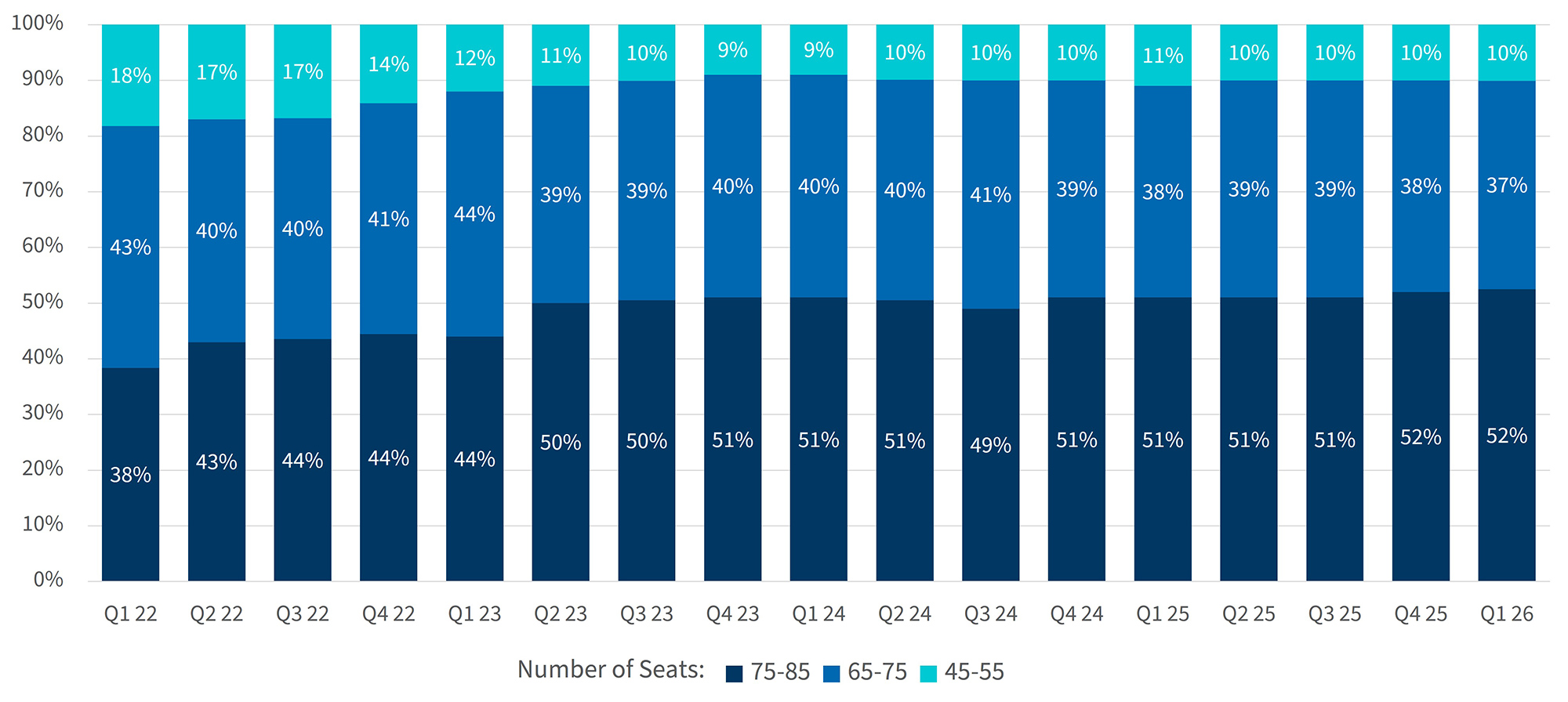

Figure 4 – Regional Fleet Mix Evolution (50-Seat vs. 70–76 Seat Aircraft)

Source: Cirium - Flight schedule data

AI Is Becoming an Operating Layer and Discipline Matters

AI is increasingly embedded across aviation operations, from predictive maintenance and fleet management to crew scheduling and air-traffic optimization. These applications offer tangible efficiency gains, but their economics differ materially from those of digital-native industries. Airlines operate on thin margins, with limited tolerance for long payback periods or experimental deployment.

At the same time, aviation’s safety-critical nature imposes higher governance and explainability standards. AI systems cannot operate as opaque “black boxes,” particularly where they intersect with flight operations, maintenance decisions or crew management.

FTI Consulting Perspective

AI investment must be disciplined, targeted and tightly linked to measurable operational or financial outcomes. Near-term value can already be unlocked in back office applications with lower risk and shorter implementation timelines. Larger value will be found in core applications such as revenue management, maintenance planning, crew optimization and inventory forecasting; however, these should be designed as “human in the loop” initially, focusing on speeding up decisions, testing new scenarios and highlighting opportunities before they are missed.

Figure 5 – Applications of AI in Aviation

Source: FTI Consulting Analysis

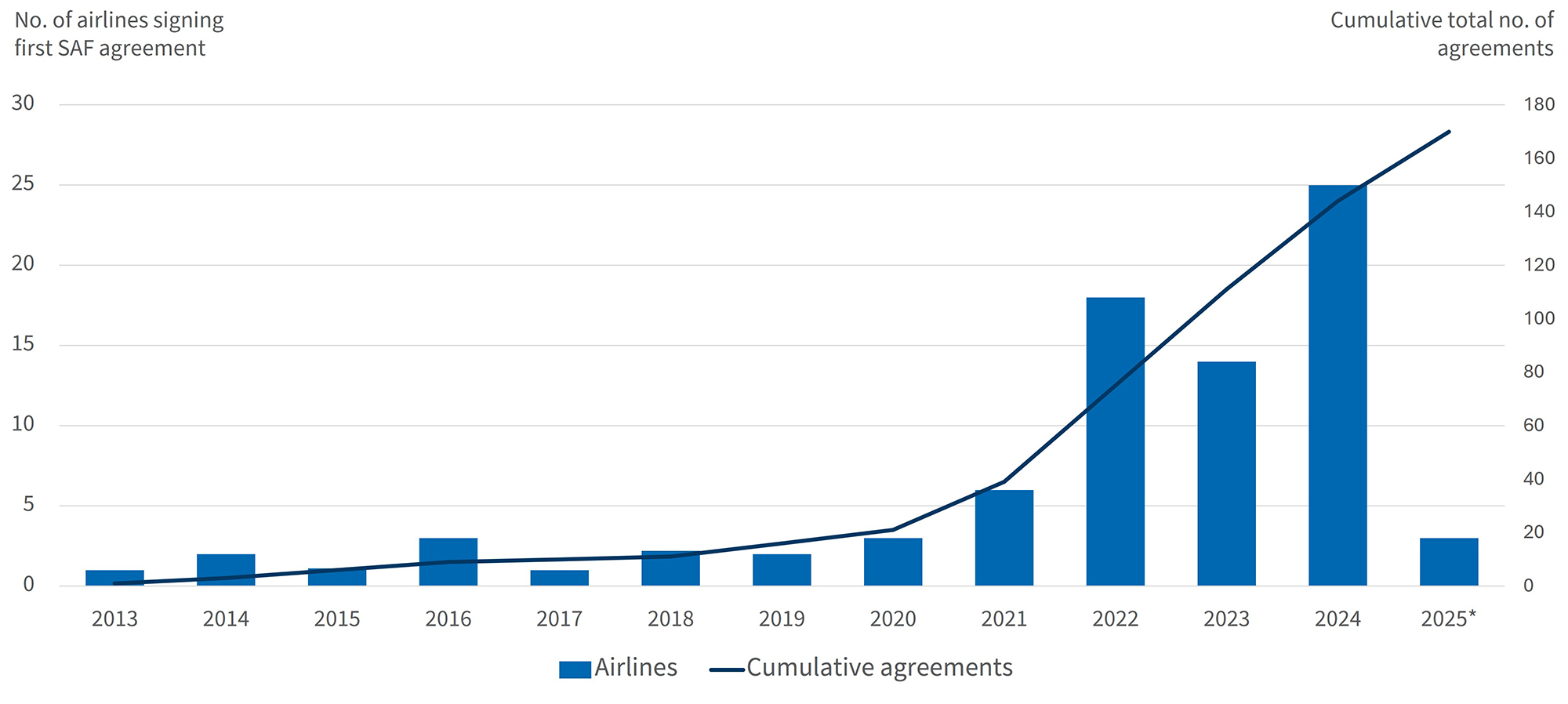

Sustainability Is Shifting from Public Commitments to Quiet Execution

Sustainability remains a strategic imperative for aviation, driven by SAF mandates, emissions disclosure requirements, EU Emission Trading Systema (“ETS”) expansion and investor scrutiny. However, political polarization, cost pressures and limited SAF availability are reshaping how airlines communicate their ambitions. High-profile public commitments are increasingly giving way to more cautious, execution-focused approaches.

The gap between aspiration and delivery has become more visible, particularly as SAF pricing remains elevated and supply constrained. Airlines must balance regulatory compliance, investor expectations and financial discipline in an increasingly complex environment.

FTI Consulting Perspective

As public pressure ebbs or becomes more polarized, airlines are likely to moderate external sustainability messaging, particularly around aggressive SAF targets, while continuing to invest quietly in new technologies, fuels and operational efficiencies.

Competitive advantage will increasingly come from execution rather than slogans, with value created through cost-effective compliance, fleet optimization and pragmatic decarbonization pathways that align with financial realities.

Figure 6 – Growing Airline Engagement in SAF Agreements

Airlines’ First SAF Agreement by Year and Cumulative Number of All Announcements

Source: IATA Sustainability and Economics

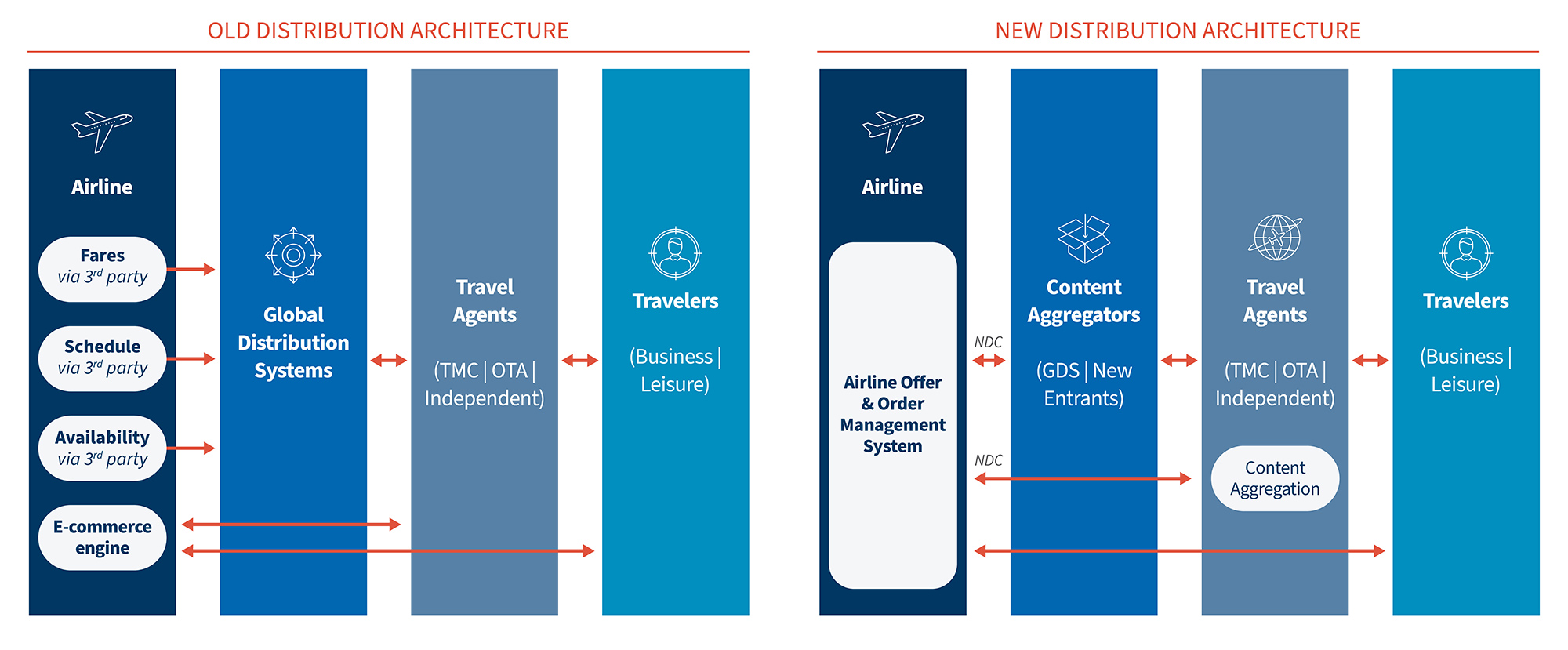

Digital Revenue Models Are Expanding

Airlines are accelerating efforts to monetize data, ancillaries, subscriptions and personalized digital journeys. Dynamic retailing is becoming a key differentiator, enabling airlines to better segment customers, optimize pricing and increase share of wallet. However, these opportunities are unevenly distributed across the industry.

Legacy technology architectures continue to constrain many airlines’ ability to retail effectively. Substantial investment is required to overcome the fragmented systems, limited data integration and outdated distribution standards which undermine both revenue potential and service quality.

FTI Consulting Perspective

Unlocking digital revenue streams requires a fundamental shift away from legacy EDIFACT systems toward modern distribution standards such as NDC and IATA ONE Order. This transformation must be accompanied by redesigned service and operating models to ensure that post-booking support remains robust and consistently matches or exceeds the experience delivered under legacy systems. Airlines that execute well can create structurally higher revenue per passenger; those that lag risk falling permanently behind.

Figure 7 – Old Versus New Distribution Architecture

Airline Gains Clearer Understanding of Customer and Therefore Has Better Opportunity To Personalize Offers

Source: IATA Report, “Getting Started with Airline Retailing”, February 2022.

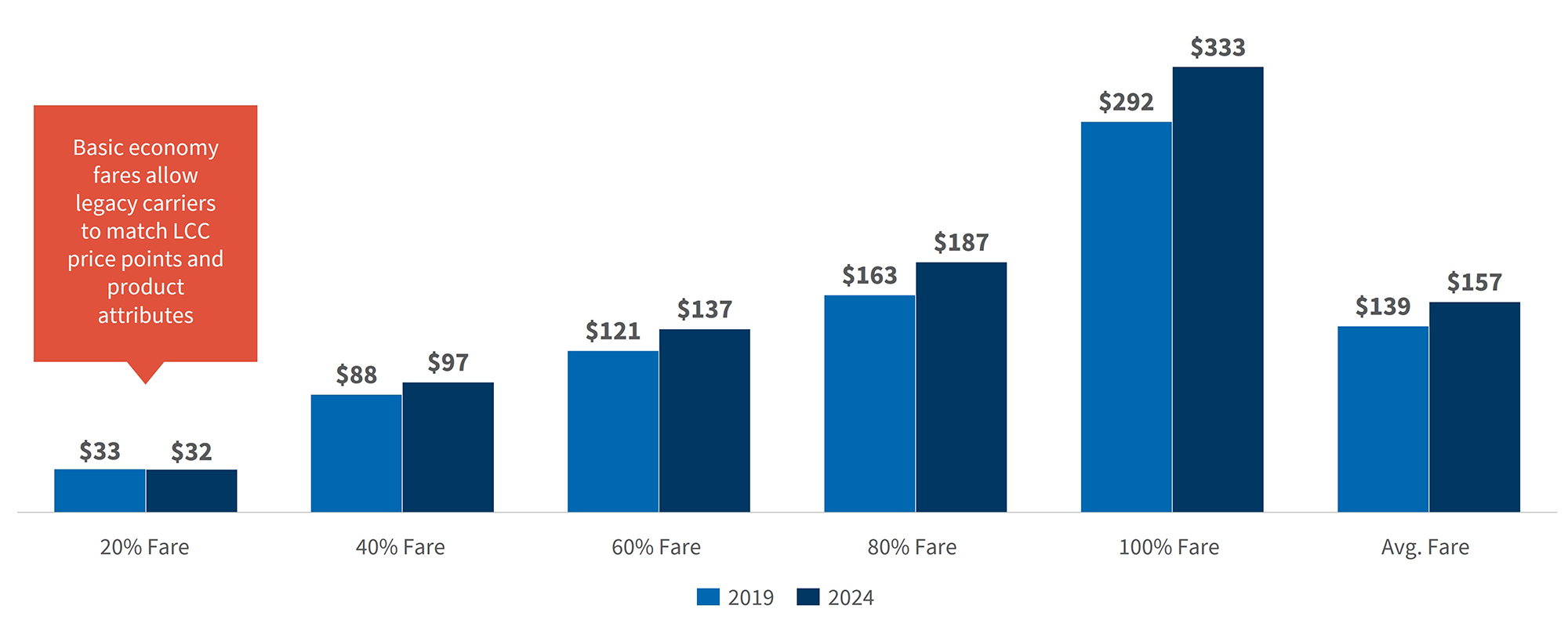

Passenger Demand Is More Fragmented and More Fragile Than It Appears

Passenger demand has recovered unevenly. Premium-leisure, long-haul leisure and “bleisure” travel remain strong, while corporate demand has stabilized at structurally lower levels. At the same time, passengers are more price sensitive and less tolerant of service disruption, increasing pressure on operational performance.

Beneath the surface, demand resilience varies significantly by segment and geography. Premium travel, while currently a growth driver, is increasingly correlated with broader financial market performance and consumer confidence.

FTI Consulting Perspective

Airlines that failed to adapt to the post-COVID demand profile and cost environment will continue to face increasing pressure to transform or exit over the coming years. While premium travel remains a growth story, it carries growing risk. Emerging evidence suggests that premium demand may be particularly vulnerable to macroeconomic shocks or market corrections, reinforcing the need for flexible capacity, diversified revenue streams and resilient cost structures.

Figure 8 – Legacy U.S. Carriers Have Placed Pressure on Low-Cost Carriers With Their Lowest Fare Buckets While Still Benefiting From the Growth of Premium and “Bleisure” Fare Increases

Source: Cirium – U.S. DOT Fare Band Data.

FTI Consulting Analysis of fare buckets on overlap routes between legacy carriers and low-cost carriers

Footnotes:

1: “2025 Market Summary Report,” Aviation Week Network (November, 2024).

2: Cowman Karl, “What today’s aircraft leasing market really means for investors, lessors and airlines,” (Mar 2026).

Related Insights

Related Information

Published

March 27, 2026

Key Contacts

Key Contacts

Global Leader of Aviation Turnaround & Restructuring, Co-Leader of Turnaround & Restructuring U.S. West Region

Global Leader of Aviation Business Transformation, Co-Leader of Human Capital

Director

Director