Mortgage Fraud: Emerging Risks and Mitigation Strategies

-

May 27, 2026

Downloads Download Article

Download Article

-

Mortgage fraud risk is evolving and growing because of advanced fraud techniques including generative AI (“GenAI”) and large language models (“LLMs”). As noted in a recent FTI Consulting article,1 fraudulent documents and phishing emails can now be easily and quickly mass produced with results that are almost undetectable using traditional methods of scrutiny. Indeed, the rapid growth in mortgage fraud has been well documented in multiple recently published studies:

As fraud schemes become more sophisticated, financial institutions face rising losses, increased scrutiny from regulators and investors, and higher operational costs. The challenge is substantial, but best mitigated when financial institutions enhance their fraud programs to be agile and responsive to new threats. Here we discuss the most pressing fraud risks facing financial institutions and strategies they can implement to prevent, detect and respond to these threats.

How Advanced Technology Is Accelerating Fraud Schemes

Mortgage fraud isn’t new but advanced technology and GenAI has dramatically accelerated both its scale and sophistication. What once took weeks to create high-quality fraudulent documents can now be accomplished in a matter of minutes. Financial institutions must now defend against traditional fraud tactics reimagined by AI. The following are three examples of the highest risk emerging fraud schemes:

- Synthetic identity fraud: Synthetic identity fraud has historically been one of the most difficult to detect forms of mortgage fraud. Using a combination of illegally acquired but factual personally identifiable information and fictitious information to open bank accounts and credit cards, these synthetic identities are able to successfully bypass legacy verification systems and controls such as credit checks and asset verifications. New and more advanced AI bots have supercharged the ability to create effective synthetic identities at scale. The impact of synthetic identify theft stretches far beyond the initial loan origination. Indeed, extended losses across the loan cycle include:

— Defaults with no recoverable borrower;

— Inability to pursue collections or legal action; and

— Incurable title defects that break the chain of title. - Document fabrication fraud: While document fabrication is not a new type of fraud, GenAI has increased the level of sophistication and the ease by which fraudsters (internal bad actors, external third parties, and loan applicants) can create falsified income and asset documents. Loans originated based on falsified income, assets, credit and collateral documents often fall into early default, creating significant repurchase and indemnification exposure.

According to a Reggora 2024 study, the average mortgage loan repurchase rate over the last 18 months (April 2023 to October 2024) is 0.49%, with each repurchase costing lenders an average of $32,288.5Beyond the potential for significant financial losses, lenders face regulatory and investor scrutiny alongside reputational damage. Lenders with excessive early default ratios will be subject to costly agency reviews such as HUD/FHA Early Payment Default Review, or an FNMA Mortgage Origination Assessment (“MORA”).

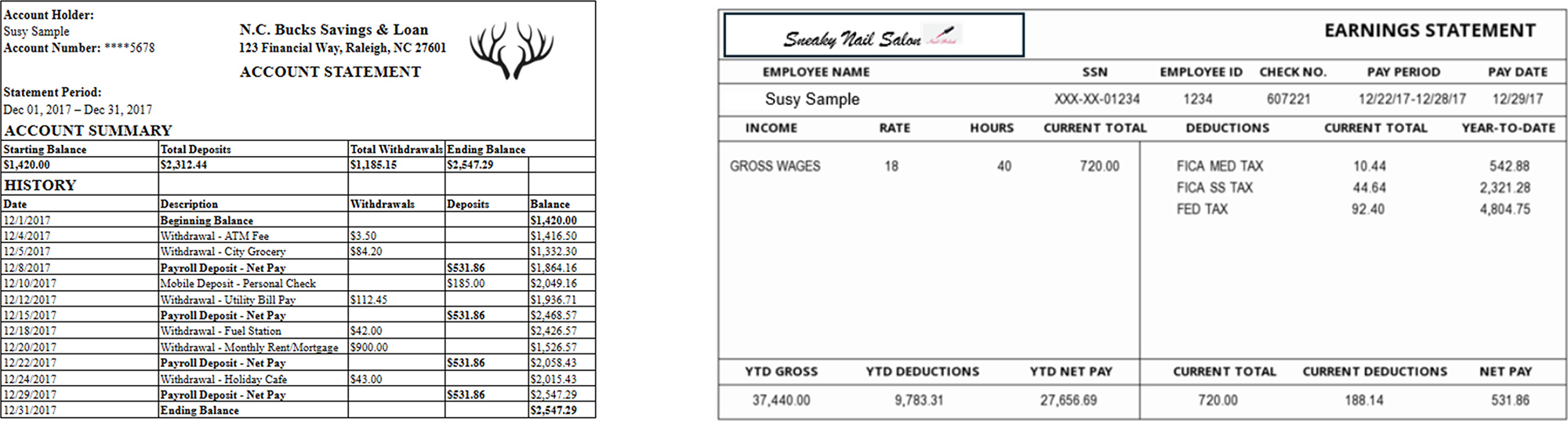

Case Example: Fakes a Child Could Make

Bad actors can now generate convincing paystubs and bank statements in minutes using widely available software that requires no specialized skills. These applications create documents from simple prompts and suggest enhancements to improve authenticity. What once demanded technical expertise and hours of effort now takes minutes and minimal know-how. Below are two examples of realistic-looking documents that were created using open-source tools.

- Wire transfer fraud: Wire Transfer Fraud can occur when the fraudster compromises legitimate business email accounts, often through social engineering or computer intrusion techniques,6 to intercept legitimate wiring instructions for a mortgage transaction between interested parties.

Nearly a quarter of property buyers are targeted with suspicious communications during the mortgage closing process. More than 10% become targets of fraud. More than 5% become victims.7A commonly seen tactic is a “last-minute” change in wiring instructions that redirects funds to the fraudster account. Increasingly, scammers are also using deepfake audio and video to impersonate agents and other parties involved in the home purchase,8 making these schemes harder to detect.

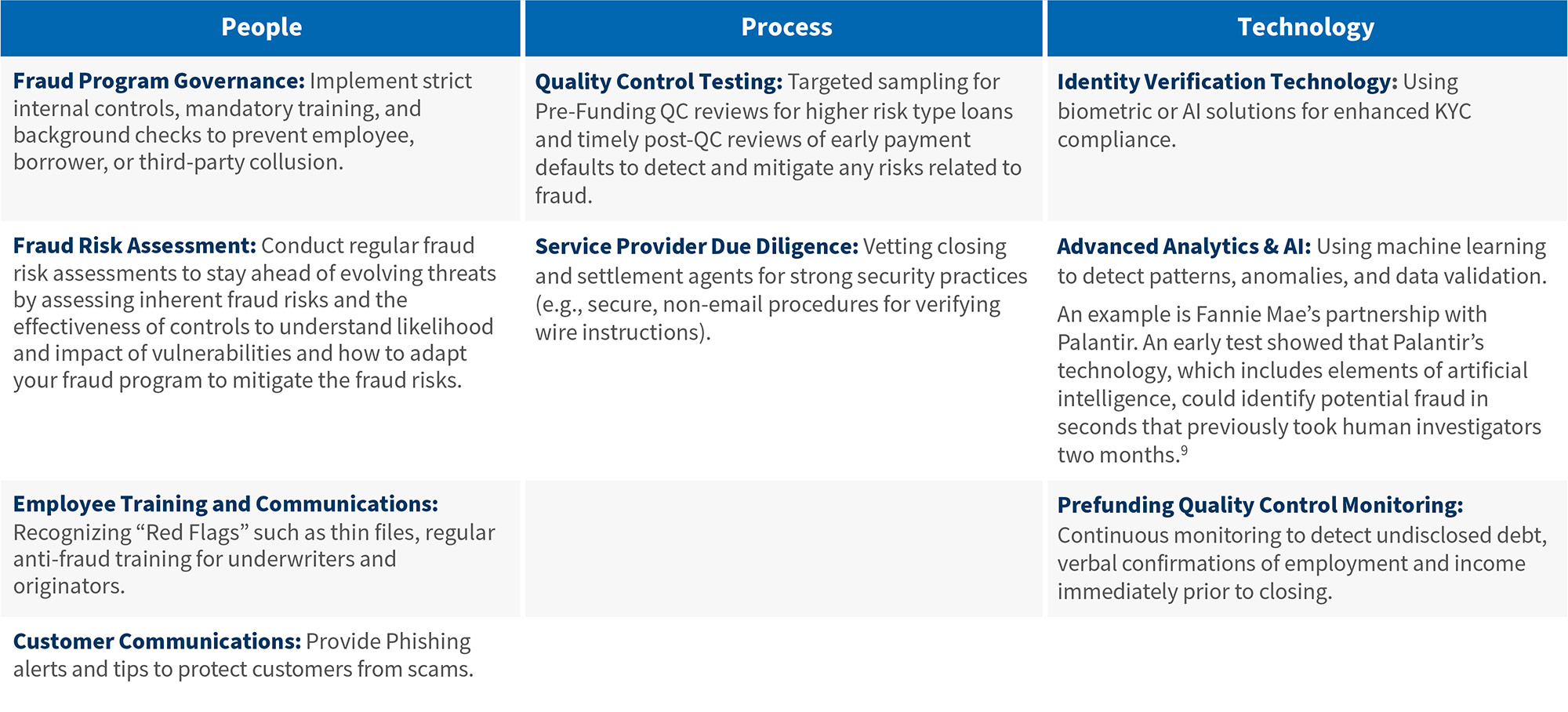

Strengthening Mortgage Fraud Defense

Unfortunately, there is no silver bullet to mitigate fraud risks involving advanced technology. The stakes are rising and as fraud schemes evolve with technology, so does their complexity. The best approach is to implement multi-layered controls that combine people, processes and technology. The following illustrates the core controls which lenders should use to help bolster their mortgage fraud prevention efforts:

Key Takeaways and Recommendations

Mortgage fraud is an increasingly sophisticated, evolving risk driven by AI and digital processes. Everyone operating in the space needs to recognize that what was once considered to be appropriate know-your-customer compliance and strong due diligence several years ago is now obsolete. Lenders must adopt a proactive, AI-powered due diligence framework that integrates cost-effective technology with robust controls. Continuous rather than singular verification needs to be in place both at origination and after loans are on the books. Institutions that fail to modernize their fraud prevention strategies risk increased losses, regulator and investor scrutiny, and long-term reputational damage.

The authors wish to thank Sandra Mozina and Serenity Guo for their contributions to this article.

Footnotes:

1: Tantleff, Alan, et al., “The Documentation Is the Risk,” FTI Consulting, (May 5, 2026).

2: Cotality, “Mortgage fraud risk continues its upward trend to end 2025” (Feb. 5, 2026).

3: Block, Eliana, “Online Real Estate Fraud Climbed to $275M in 2025, FBI Says,” NAR REALTOR News, (Apr. 13, 2026).

4: O’Connor, Ade, “Every Dollar Lost to Fraud Costs North America’s Financial Institutions $5, According to LexisNexus Risk Solutions,” LexisNexis Risk Solutions, (Sept. 10, 2025).

5: Reggora, “Research Finds Average Mortgage Loan Repurchase Rate is 0.49%, Average Cost $32,288 per Loan” (Dec. 5, 2024).

6: Fed. Bureau of Investigation, Internet Crime Complaint Center, “Internet Crime Report 2021” (Mar. 2022).

7: CertifID, “2024 State of Wire Fraud Report”(2024).

8: Tracey, Melissa Dittmann, “Scammers Use Agent Deepfakes to Fool Buyers, Sellers,” NAR REALTOR News, (Mar. 7, 2024).

9: 9 Pound, Jesse, “Palantir teams up with Fannie Mae in AI push to sniff out mortgage fraud,” CNBC, (May 28, 2025).

Related Insights

Related Information

Published

May 27, 2026

Key Contacts

Key Contacts

Senior Managing Director

Managing Director

Managing Director

Managing Director