Power, Renewables & Energy Transition: 2025 M&A Year in Review and 2026 Outlook

-

March 23, 2026

Downloads Download Article

Download Article

-

Entering 2025, renewable energy mergers and acquisitions (“M&A”) activity encountered significant headwinds, including elevated capital costs, rigid supply chain audit requirements and policy friction stemming from the One Big Beautiful Bill Act (“OBBBA”).1

2025 Review

As a result, renewable energy deal volume plateaued in 2025, failing to surpass 2024 levels as capital fled subsidy-sensitive sectors like wind and alternative fuels. Despite these challenges, investor conviction strengthened during the second half of the year, driven by the “use-it-or-lose-it” urgency of OBBBA tax credit deadlines and the undeniable signal of surging power demand. The confirmation of ITC eligibility for standalone storage, combined with the maturation of the tax credit transferability market, offered a critical liquidity valve for investors willing to navigate the complex compliance landscape.

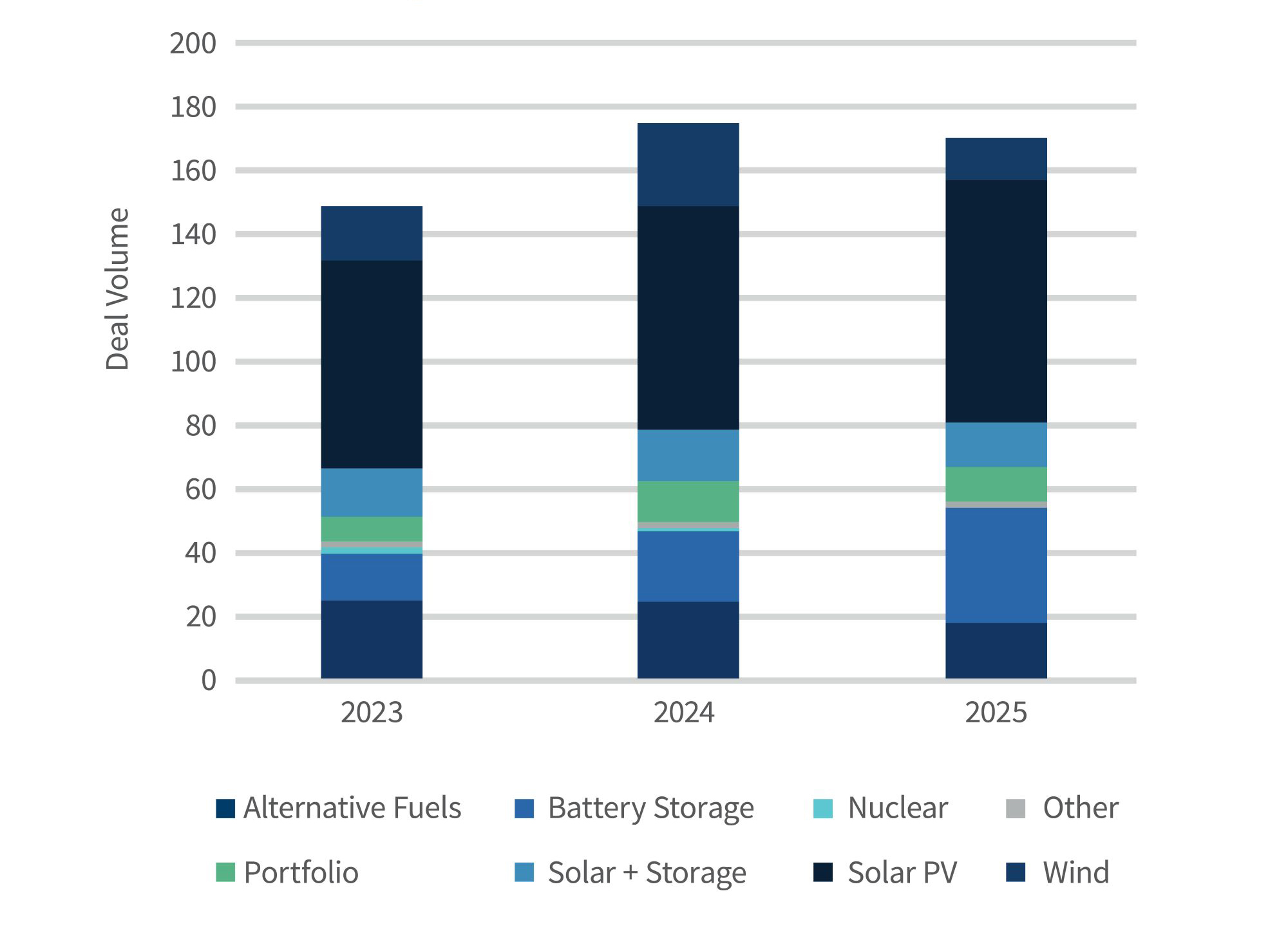

Figure 1: M&A Volume 2023-2025

Source: Infralogic Transaction Data

Solar PV technologies continued to dominate M&A volume, accounting for approximately 45% of all transactions.2 In a departure from previous years, there was a stark bifurcation in platform M&A activity; interest rates and interconnection delays drove a wedge between “deployment-ready” developers and those holding speculative queue positions. While selective platform transactions did occur, the broader trend favored asset-level sales as liquidity-constrained developers sought to recycle capital. Year over year, transaction activity for wind and alternative fuels declined, however, there was one notable exception. Battery Storage transactions surged by over 60%,3 proving the technology’s evolution into a mature and essential component of modern energy infrastructure.

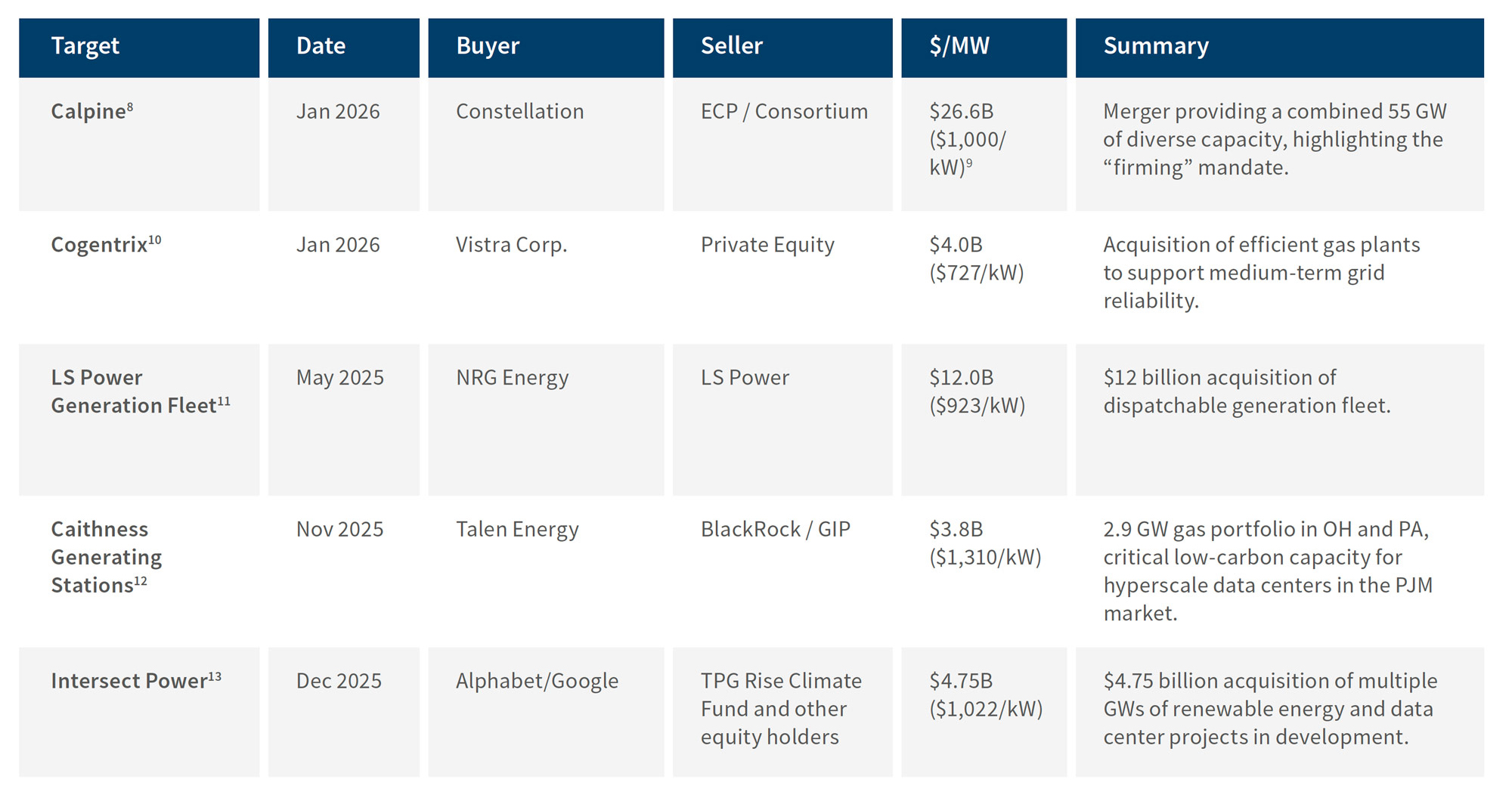

Meanwhile, 2025 also marked a resurgence of conventional thermal power M&A, headlined by Constellation’s merger with Calpine,4 Vistra’s acquisition of Cogentrix5 and Talen Energy’s acquisition of PJM baseload assets from Caithness Energy and Blackrock.6 Although some market participants have historically viewed natural gas and nuclear generation as distinct from the energy transition, there is increasing market conviction that these technologies will play an indispensable role in the evolving U.S. energy landscape, serving as a critical provider of 24/7 power to digital infrastructure.

Key 2025 Trends

Firm Power Resurgence Driving Deal Flow

The definition of “energy transition” assets expanded fundamentally in 2025. Previously viewed by ESG-focused capital as legacy infrastructure, natural gas and nuclear generation assets were underwritten in 2025 as critical reliability components. The exponential increase in energy demand from AI training clusters and data centers became a key catalyst, as investors recognized that meeting Hyperscalers’7 uptime requirements entails firm, dispatchable power alongside renewables. This awareness accelerated investment toward assets providing firming capacity, underscoring the essential role of hybrid and dispatchable resources in enabling data center growth within the broader energy transition.

This trend manifested in a resurgence of large-scale M&A involving traditional independent power producers (“IPPs”). Unlike the valuation multiples of 2021–2022 which favored growth pipelines, 2025 valuations rewarded existing steel-in-the-ground capability. This shift catalyzed vertical integration strategies, most notably seen in the Hyperscaler ecosystem, where tech giants moved beyond virtual Power Purchase Agreements (“vPPAs”) to support the acquisition and life-extension of nuclear, gas and renewable assets directly, creating a new class of “behind-the-meter” infrastructure deals.

Figure 2: Notable Firm Power and Infrastructure Transactions

Interconnection as a Catalyst for Renewable Platform Consolidation

Renewable platform M&A activity, which slowed in 2023 and 2024, rebounded in 2025 with a specific focus: the acquisition of interconnection queue positions. With wait times stretching to 4-5 years in PJM, MISO and CAISO, an approved interconnection position emerged as the primary currency in the sector. This dynamic forced a bifurcation in the market between “deployment-ready” platforms and those holding speculative, early-stage pipelines.

Well-capitalized entities utilized M&A to bypass the development bottleneck, paying premiums for mid-sized developers specifically to inherit their mature queue positions. This “buy vs. build” strategy became the dominant logic for new market entrants, including international energy majors and private equity infrastructure funds seeking to deploy capital on an expedited basis. Conversely, the larger at risk deposits and stricter financial readiness requirements imposed by FERC Order 2023 pressured smaller, capital constrained developers. Unable to float the balance sheet requirements for long-dated queues, several were forced into portfolio or outright platform sales, fueling a secondary market for interconnection rights.

Figure 3: Notable Platform and Portfolio Divestitures

Storage and Hybrid Deal Activity

2025 was a breakout year for battery storage M&A, cementing storage as a core infrastructure asset class within the power sector. Transaction volumes for standalone battery storage deals rose more than 60%17 from 2024 levels, driven by a fundamental shift in the underwriting thesis. Previously, storage assets were valued primarily on shallow, volatile ancillary service markets (like frequency regulation). In 2025, the investment case pivoted toward “firm capacity” and energy arbitrage, supported by the persistent lag in transmission build-out which has made non-wires alternatives essential for grid stability.

Policy certainty played a decisive role in this breakout. The OBBBA’s confirmation of long dated Investment Tax Credit (“ITC”) eligibility for standalone storage, without an accelerated sunset, effectively repriced project economics overnight and provided the bankable base returns required by infrastructure funds. This created a divergence in the solar market: while pure-play solar projects faced pricing pressure in congested hubs due to declining midday capture rates, solar-plus-storage projects commanded significant premiums. Investors aggressively targeted these hybrid assets to capture the “duck curve” arbitrage, driving portfolio turnover in markets like CAISO and ERCOT where solar penetration is highest.

Figure 4: Notable Storage and Hybrid Transactions

Transferability: The Liquidity Engine for M&A

While the OBBBA introduced policy headwinds, the maturing transferability market provided the necessary liquidity to keep deal velocity high. Transaction volume for tax credits surged to an estimated $60 billion in 2025 (up from $52 billion in 2024).22 This mechanism did not just facilitate financing; it fundamentally altered the buyer universe, allowing non-traditional players, such as big-box retailers, insurance giants and corporates to aggressively bid on credits, thereby de-risking the capital stack for developers.

By decoupling tax appetite from asset ownership, transferability allowed financial sponsors to execute acquisitions without needing the complex, slow-moving tax equity partnerships of previous cycles. This expanded liquidity pool was critical for clearing the market in 2025.

Figure 5: Notable Transferability Transactions

2026 Outlook

As we move into 2026, the renewable energy sector faces a defining horizon marked by rigid execution timelines. Although the cost of capital moderated in late 2025 following the Federal Reserve’s decisive rate cuts in the second half of the year, the industry enters 1Q26 confronting a complex regulatory environment that will dictate M&A strategy. The passage of the OBBBA has replaced the previous era of open-ended subsidies with strict sourcing mandates and time pressure, creating urgency across the capital stack that will force transaction activity.

Taken as a whole, the outlook for renewables M&A activity in 2026 can be summed up as “compliance-driven.” The implementation of the OBBBA has introduced sweeping mandates that will directly influence buy/sell decisions:

- Strict Supply Chain Audits: The shift to Foreign Entity of Concern (“FEOC”) audits will force developers with “tainted” supply chains to divest assets or seek recapitalization, driving distressed M&A volume. Conversely, platforms with “clean,” auditable platforms may see premium valuations and accelerated consolidation.

- The July 4th Deadline: The mandate to begin physical construction by July 4, 2026, to qualify for full credits will trigger a “use it or lose it” wave of transactions in H1 2026, as developers race to monetize safe-harbored positions before the window closes. .

- Corporate Tax Incentives: Reinstating 100% Bonus Depreciation effectively subsidizes capital-intensive infrastructure, incentivizing corporates to acquire operating assets in the renewables space for tax shield purposes.

- Leverage Cap Flexibility: The reversion of Section 163(j) limits to an EBITDA standard removes the depreciation penalty that previously constrained capital-intensive borrowers. By allowing sponsors to add back significant non-cash depreciation charges when calculating interest deductibility, this change materially expands tax-efficient debt capacity, a structural shift likely to reignite private equity LBO activity.

These provisions signal a significant shift in U.S. development strategy. Despite logistical hurdles, we expect these regulatory catalysts, combined with structural demand drivers, to bolster deal activity in 2026.

AI and Data Center Energy Demand

AI and data center energy demand have become central to M&A activity. The build out of AI and machine learning workloads is driving sustained growth in baseload power demand. Leading Hyperscalers are moving beyond financial hedges toward direct asset ownership to secure reliability and capture newly restored tax benefits. Currently, Hyperscalers are aggressively acquiring operating data center and power-generation assets to meet their power demand. Additionally, they are funding the next generation of firm power by providing development capital for behind-the-meter and dedicated off-site resources.

In the near term, we anticipate a surge of investment from Hyperscalers into solar-plus-storage and thermal facilities to meet immediate power needs, as well as in small modular reactors as they look further out to the 2030s.

Small Module Reactors (“SMRs”): Early Momentum and Market Positioning

SMRs are beginning to show early signs of commercial traction, and we expect 2026 to set the competitive landscape for which technologies and partnerships pull ahead.

- Commercial Progress Accelerates: Several leading SMR designs have advanced through major U.S. Nuclear Regulatory Commission (“NRC”) review stages and secured initial site approvals with utilities, giving investors clearer visibility on cost, schedule and near term deployment paths.

- Partnerships Begin To Solidify: We anticipate Hyperscalers, EPCs, and utilities to form early anchor partnerships this year as they look to secure long dated, zero carbon baseload and influence emerging supply chains.

- Winners Emerge Early: Developers with manufacturable designs and credible delivery partners are likely to secure capital and attract offtakers for vPPAs, while more speculative platforms may struggle, kickstarting a shakeout phase in 2026.

Battery Storage: The Firming Premium

Battery storage has become a core M&A theme. As solar penetration peaks in markets like CAISO and ERCOT, storage value is shifting from ancillary services toward firm capacity and load shifting, and standalone batteries are now treated as a primary infrastructure asset rather than a mere add on. We expect M&A activity to continue at a rapid clip in the year ahead and note the following observations and trends.

- Superior Returns (ITC Eligibility): Crucially, standalone storage maintains full eligibility for the Investment Tax Credit. This upfront 30%+ capital subsidy, when paired with high-value revenue streams, enables such projects to generate amongst the highest returns in the renewable and adjacent space.

- The Tolling Trend: Volatility in merchant revenue (particularly in ERCOT) has driven buyers toward the safety of Tolling Agreements. M&A premiums are now accruing to developers who can wrap their storage assets in 10–20 year capacity contracts with utilities or Hyperscalers, rather than those relying on merchant arbitrage algorithms.

- The Augmentation Trade: We are seeing a distinct M&A strategy where IPPs acquire vintage solar assets specifically to retrofit them with battery storage. This brownfield expansion bypasses the frozen interconnection queues, allowing developers to deploy capital into high-return storage projects using existing Points of Interconnection.

Supply Chain Constraints and Valuation Drivers: Foreign Entity of Concern (“FEOC”) Anxiety

While technological progress continues, a key driver of value in 2026 M&A transactions will be compliance. Market anxiety has shifted markedly from concerns about losing Safe Harbor to failing FEOC audits.

- FEOC & PFE (Prohibited Foreign Entity) vs. Safe Harbor: Sophisticated developers have largely mitigated the construction cliff by utilizing off-site physical work (e.g., taking delivery of transformers or inverters) to lock in Safe Harbor status through 2029. The far more pressing risk in M&A diligence is FEOC/PFE exposure. A project may be validly Safe Harbored, but if project equipment is traced to a Prohibited Foreign Entity, tax credits evaporate.

- Non-Compliant Inventory Risk: We anticipate M&A discounts for platforms holding large inventories of Safe Harbored equipment that lack granular supply chain traceability. Conversely, “clean” inventory, backed by non-FEOC supply chains that are auditable, will trade at a scarcity premium.

Capital Market Considerations for Deal Activity

The U.S. capital markets demonstrated resilience in 2025, but 2026 will likely see a divergence in capital availability. The restoration of EBITDA-based interest deductibility (Section 163(j)) is a critical development; it significantly increases how much debt operating platforms can support. This change could spur more private equity-led, take-private transactions and platform consolidations, as sponsors can now apply more efficient leverage to stable cash flows.

On a more somber note, we acknowledge that while the Safe Harbor deadline is manageable for incumbents, the barriers to entry regarding PFE compliance are higher than ever. We expect significant consolidation as smaller players, unable to fund the requisite compliance infrastructure or secure non-FEOC supply, seek exits. The role of Private Credit will be paramount here, providing the capital solutions necessary to bridge the liquidity gap for these capital-intensive compliance mandates.

Conclusion

Ultimately, 2025 will be remembered as the year when the push for a clean energy transition was forced to reconcile with the hard realities of maintaining grid reliability, satisfying an unprecedented surge in power demand and navigating a stringent new policy environment. This convergence forced a maturation in how assets are valued and traded. While high capital costs and supply chain friction dampened overall volumes, the market successfully pivoted toward high-quality, high-reliability assets, resulting in a series of notable, strategic transactions despite the broader headwinds.

Looking into 2026, we remain optimistic that the industry will navigate the logistical bottlenecks created by the OBBBA. However, in the near term, fortune will favor the compliant: Vertically integrated firms with clean, non-FEOC supply chains and validated Safe Harbor strategies will be well-positioned to consolidate market share. In 2026, speculative pipelines will yield to operational realities, making rigorous compliance and reliable execution the definitive drivers of M&A value creation.

Footnotes:

1: One Big Beautiful Bill Act, Pub. L. No. 119 21, 139 Stat. 72 (2025).

2: Infralogic Transaction Data (accessed Feb. 2026).

3: Infralogic Transaction Data.

4: Press Release, Constellation Energy Corporation, “Constellation Completes Calpine Transaction, Powering America’s Clean Energy Future” (Jan. 7, 2026).

5: DiGangi, Diana, “Vistra to buy Cogentrix Energy’5.5 GW of gas plants in $4B deal,” Utility Dive (Jan. 6, 2025).

6: Press Release, Talen Energy Corporation, “Talen Energy Completes Freedom and Guernsey Acquisitions” (Nov. 25, 2025).

7: Hyperscalers include Amazon (AWS), Microsoft (Azure), Google (Google Cloud), and other big tech players, and are defined as the large cloud providers that run data centers and offer computing and storage services.

8: See supra note 4.

9: Good, Allison, “Constellation shares soar on $26.6B Calpine acquisition,” S&P Global (Jan. 10, 2025).

10: See supra note 5.

11: Ciampoli, Paul, “NRG Energy to Buy LS Power Generation Portfolio for $12 Billion,” American Public Power Association (ay 12, 2025).

12: See supra note 6.

13: Press Release, Alphabet Inc., “Alphabet Announces Agreement to Acquire Intersect to Advance U.S. Energy Innovation” (Dec. 22, 2025).

14: Press Release, Sempra, “Sempra Announces Strategic Transactions Advancing Goal of Building Leading U.S. Utility Growth Business” (Sept. 23, 2025).

15: Kennedy, Ryan, “Dispatch Energy Acquires Green Lantern Solar, expanding distributed generation across nine states,” PV Magazine (Nov. 13, 2025), .

16: Press Release, UGE International Ltd., “UGE Acquires 122 Development‑Stage Solar Projects Across 14 States” (June 3, 2025), .

17: Infralogic Transaction Data.

18: Press Release, Repsol, “Repsol allies with Stonepeak on solar and storage portfolio for its first US renewals partnership” (Apr. 29, 2025).

19: Press Release, Engie North America Inc., “ENGIE enters partnership with CBRE Investment Management for 2.4 GW portfolio of Battery Storage Assets in the U.S.” (May 15, 2025).

20: Press Release, GridStor, “GridStor Announces Acquisition of Texas Battery Energy Storage Project from Balanced Rock Power” (Feb. 3, 2025).

21: Press Release, Altus Power, “Altus Power Acquires 234 MW Portfolio Across 18 States from Greenbacker” (Dec. 18, 2025).

22: Crux Climate, “Highlights from Crux’s 2025 mid-year market intelligence report” (Sept. 8, 2025).

23: Press Release, Intersolar Energy Storage North America, “Walmart partners with Nexamp to Build 31 Community Solar Projects Across Five States” (April 22,2025).

24: Press Release, Latham & Watkins LLP, “Latham & Watkins Advises Cordelio Power in the Financing of the Winfield Solar Project” (September 11, 2025),

25: Press Release, CRC IB, “CRC-IB Advises Innergex on $54.4M Tax Credit Transfer Agreement for 30MW Solar / 120MWh Battery Storage Project” (September 24, 2025).

Related Insights

Published

March 23, 2026

Key Contacts

Key Contacts

Global Practice Leader Power, Renewables & Energy Transition (PRET)

Senior Managing Director

Managing Director

Director